Here's the Difference Between MY Picks (and the Wild Names Wall Street Speculators are Flocking to!)

The June issue of my newly re-named Weiss Ratings’ Safe Money Report is about to go to press. I have loads to say about the state of the markets in the issue, including details on several behind-the-scenes warning signs that all too many investors are ignoring.

But just because I’m cautious doesn’t mean I have nothing to recommend. Far from it. It’s just that what I’m comfortable putting out there — and the wild investments Wall Street is pushing — couldn’t be more different.

Consider my lead recommendation this month. It’s a “Steady Eddie” company in the food and beverage space. It’s currently rated “B” by our time-tested Weiss Ratings system, and hasn’t earned anything less than a BUY grade since mid-2014.

|

The stock trades at a reasonable 13X earnings and 2.4X sales, and sports an S&P 500-topping dividend yield of around 2%. What’s more, that payout has risen at an annualized rate of 11% over the past three years.

The firm’s list of brands is so attractive that a well-known activist hedge fund recently bought a sizable chunk of its shares. That firm is now agitating for change, and it’s possible that will lead to a merger — just the latest in a long series of them in the industry.

The shares have already risen at a respectable single-digit rate in 2018. But I have every reason to believe they’ll continue delivering solid gains for investors in the months and quarters ahead, without exposing them to undue risk.

Now let’s contrast that to some of the “moonshot” companies that the wild-eyed speculators on Wall Street are going gaga about. I just ran a Weiss Ratings Screener for all stocks traded on the Nasdaq or NYSE with a closing price of at least $5, a market cap of at least $1 billion, and average daily trading volume of at least 50,000 shares.

I screened out those rated “D+” (SELL) or lower. Then I sorted the list in descending order by year-to-date performance. The general idea? To see what the stocks leading this market look like when it comes to actual fundamentals, not just price performance and momentum.

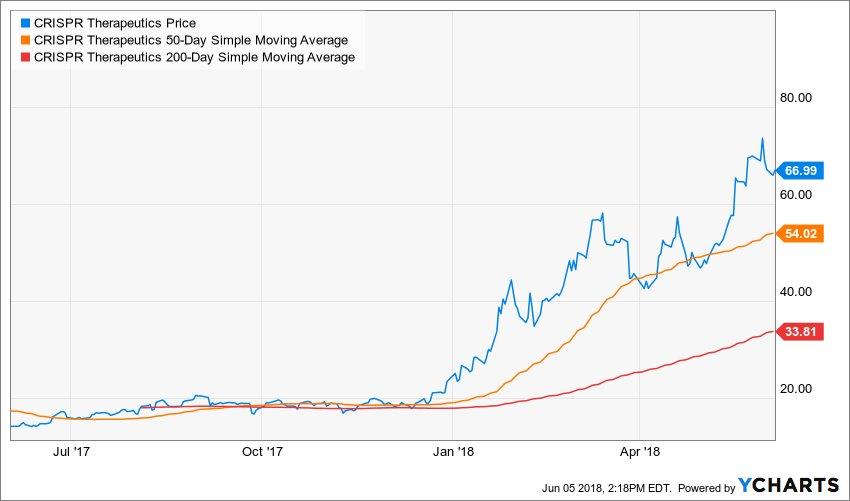

Topping the list is a firm called Crispr Therapeutics AG (CRSP, Rated “C-”). This Swiss biotechnology and gene-based medicine company trades here on the Nasdaq, and it’s up a whopping 192% year-to-date — despite the fact the year isn’t even half over.

Now, let’s dig a little deeper.

- First, CRSP is just barely rated a HOLD by our Ratings model. That’s yellow flag No. 1.

- Next, I’d tell you about its high price-to-earnings ratio ... if it had any earnings. But it doesn’t. The company racked up net losses of $75 million, or $1.79 per share, over the trailing 12 months. That’s yellow flag No. 2.

- Fortunately, you CAN evaluate the stock based on its price-to-sales ratio. Unfortunately, it trades at 85X sales — more than 38 times the S&P 500! Yellow flag No. 3.

- And good luck finding a dividend. Of course, it doesn’t pay one. Yellow flag No. 4 for me.

None of that has stopped it from trading into the stratosphere, as you can see in the chart below. But isn’t this the kind of action that should worry a prudent, careful investor just a little bit?

|

Now I know some will argue that you can’t look at development-stage biotechs through a traditional lens. I mean, who uses fuddy-duddy metrics like dividend yields or P/E ratios when you have a stock that’s going to trade to infinity and beyond?

So, for the sake of argument, let’s assume that’s right and move on to stock No. 2 on my “leader board”: Axon Enterprises (AAXN, Rated “C”). If the name doesn’t ring a bell, that’s because the company changed it from “Taser International” last April.

Axon says it made that move to highlight its shift to more of a software/service model, one reliant on getting police departments to sign up for its “Evidence.com” data storage and processing subscription offerings.

But to me, it looks suspiciously like other corporate rebrandings we’ve seen in the past — those designed solely to capitalize on whatever the market fad of the moment was.

Just think back to how many companies added a dot-com to their name, or changed it to something else that sounded “tech-ish,” to profit from Tech Bubble 1 in the late 1990s.

Anyway, back to the stock. It has literally gone vertical, pushing the gain to +140% YTD ...

|

But AAXN gets only a middling “C” (HOLD) grade from our Weiss Ratings system. What’s more, the stock trades at a mind-boggling 257X trailing 12-month earnings. That’s more than ten times the S&P 500.

In other words, it would take until around the year 2,275 for AAXN to earn back its share price at the current rate of EPS.

Yes, that’s using reported GAAP figures not “adjusted” ones. But even if you give AAXN the benefit of the doubt, the P/E drops to “only” 151 — just like the proof of the rum some of today’s speculators must be drinking! And on a price-to-sales basis, it trades at 9.5X, slightly more than four times the S&P.

Of course, the last thing momentum-chasing investors care about is valuations. Case in point: Twitter (TWTR, Rated “C-”) is getting added to the S&P 500 tomorrow. This news sparked a furious new round of buying in anticipation of all the purchases that index mutual fund and ETF managers will have to do in this name.

Never mind the fact the company earned only one penny per share in the last 12 months on a GAAP basis. That gives the stock a P/E of ... oh ... around 4,000! Even if you use adjusted EPS, you’re still talking about a P/E of 68-ish.

What’s the bottom line here? I can’t stop investors from living dangerously with their money. I can’t stop everyone from chasing these kinds of stocks if all they crave is fast trading action and momentum, with little regard to potential downside risk or the need for a margin of safety.

But I can say that the wild rallies in these kinds of very high-risk names ... not to mention the crazy hype and blanket coverage in the financial media about tech, tech, and more tech ... is concerning.

It’s the same kind of thing you saw with the last generation of tech darlings in the late 1990s, and again with real estate in the mid-2000s.

Rest assured in my Weiss Ratings’ Safe Money Report, I’ll focus instead on stocks that have the kind of time-tested, rock-solid fundamentals, and high Ratings that you can rely on for lasting gains, not the flash-in-the-pan, faddish kind. Click here or call my team at 1-877-934-7778 to get your hands on the June pick I mentioned earlier, as well as all my other guidance. I’m confident they’ll help you navigate this increasingly volatile and dangerous environment in the rest of 2018 and beyond.

Until next time,

Mike Larson