|

"If you use a credit card, you don't want to be rich."— Mark Cuban

"If you can't pay cash ... don't buy it," I said to my son as he rolled his eyes.

That's an old-fashioned attitude, but I have always avoided debt like the plague. I am proud to say I don't owe a dime to anybody on this planet (including my ex-wife). And I've pounded this philosophy into my children's heads for years and years.

My kids have largely listened to this advice. However, I can't say the same about most Americans, who are hopelessly addicted to plastic.

Americans collectively owe more than $1 trillion in credit card debt. The average American, age 65 to 69, carries a credit card balance of $6,786. That figure gets a lot higher in lower age brackets.

The typical American has three credit cards in their wallet and pays an average interest rate of 16.4% on their credit card debt.

Americans collectively paid $110 billion in interest and fees to credit card companies in 2018, a 13% increase from the $98 billion of interest paid in 2017.

Dumb, dumb, dumb.

I don't tell you that as a lecture about how you should use your credit cards, but to get you to think about getting on the receiving end of that $110 billion.

Yup, the credit card business is incredibly lucrative and a great place to invest some of your money.

Just ask the largest credit card issuers in the U.S., which collect interest and/or fees from tens or even hundreds of millions of customers:

- Visa (V), with 323 million cardholders

- Mastercard (MA), with 191 million cardholders

- JPMorgan Chase (JPM), with 93 million cardholders

- American Express (AXP), with 58 million cardholders

- Discover (DFS), with 57 million cardholders

- Citibank (C), with 48 million cardholders

- Capital One (COF), with 45 million cardholders

Disclosure: My Weiss Crypto Investor subscribers own Mastercard and are sitting on a fat open gain. The stock is already up more than 10% since we added it to our buy list just six weeks ago. And we have plenty of reasons to believe that gain is going to get a lot fatter this year.

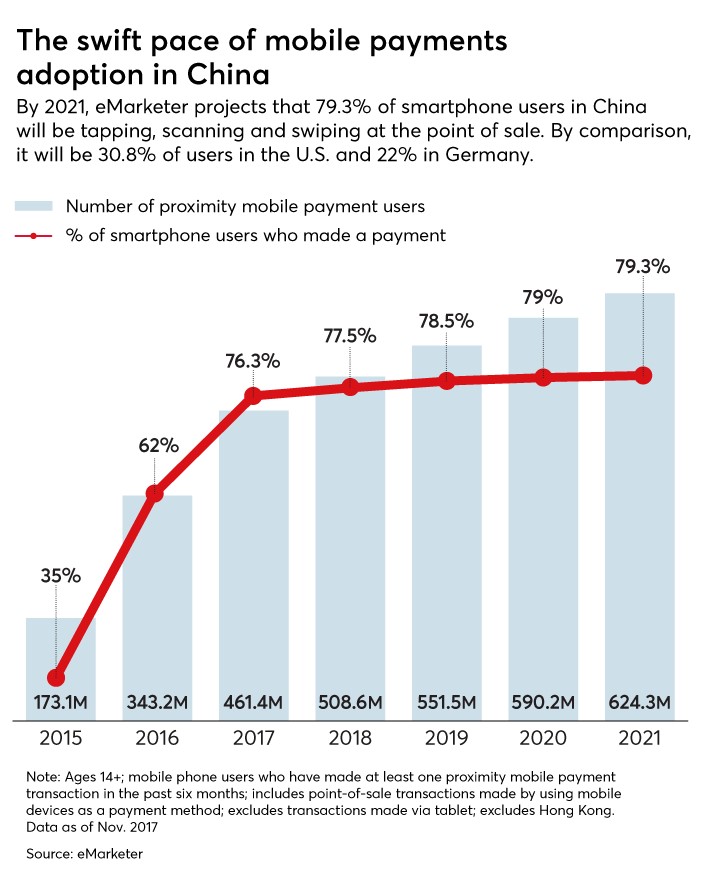

Even better investments than the above credit card giants are the payment processing companies in China.

China is the largest e-commerce market in the world. It accounts for 40% of the world's e-commerce, which is way up from less than 1% about a decade ago.

Note that I said "payment processors" and not credit cards.

You see, credit cards are not very popular in China. In fact, most Chinese don't have a credit card but instead rely on mobile payment platforms.

China has grown so fast that its credit cards have moved directly to smartphone-based payment platforms. Similar to how it skipped calculators and went straight from the abacus to the personal computer.

The Chinese pay for just about everything with their mobile phones. They even make donations to homeless people with a smartphone!

|

The two most popular payment processing apps in China are Alipay from Alibaba (BABA) and WeChat Pay from Tencent (TCEHY). More than 90% of Chinese mobile payments take place on these platforms. Even though those are both Chinese companies, both are traded right here in the U.S.

The credit card business is controlled by a small number of players, receives a piece of much of the world's commerce, and controls the growing online economy.

There is a lot of money to be made by investing in them. Just ask my subscribers. Better yet, click here to join them.

Best wishes,

Tony