Tempted to collect your Social Security sooner? Here's why it pays to put it off

|

Break out the rocking chair, because I’m going to retire and sign up for Social Security tomorrow.

Not really. But one of my closest friends from high school just retired after working 35 years at Boeing. He is loving life so much that he has to pinch himself to make sure he’s not dreaming. Really!

He spends his days pursuing his three big passions: golfing, tinkering with his 1970s muscle car and spending time with his young grandchildren. No wonder he can’t stop smiling.

My friend got me thinking. I have accumulated a nice nest egg of savings. I am completely debt-free. And I am eligible to start collecting a monthly Social Security check.

My problem is that I love my work so much that I have zero desire to retire. You’re stuck with me until I’m too blind or too senile to follow the markets.

Still, my friend’s retirement prompted me to check my personal Social Security account and see how much I could collect if I did call it quits.

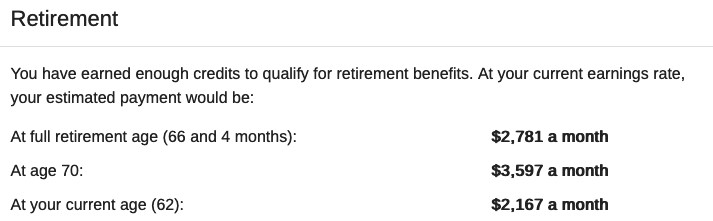

Here’s a screenshot of my Social Security account. I am 62 years old (I turn 63 next month), so I would receive $2,167 a month if I started collecting retirement benefits today.

|

But, if I wait until my “full retirement age,” which is 66 years and 4 months, I would receive $2,781, a $614 or 28% larger monthly check.

NOTE: Your Social Security benefit is based on your work history. The check is based on the wage income for your 35 highest, inflation-adjusted years (up to the ever-changing payroll tax cap).

The age that you hit full retirement age depends on what year you were born. Baby boomers hit full retirement age between 66 and 67 years old. Anyone born in or after 1960 has to wait until age 68 to receive a 100% Social Security benefit.

However, if you start collecting before your full retirement age, you will see a permanent reduction to your monthly payout. Conversely, waiting later than your full retirement age can lift your payout above 100%.

Your monthly check will increase by roughly 8% for every year that you delay receiving Social Security, beginning at age 62 and ending at age 70, in my case.

Claiming at age 62 will result in a 25% to 30% lower payout depending on your birth year. But if you wait until age 70 to start collecting, you would increase your payout by 24% to 32% above what you would have received at full retirement age.

Look at my numbers: I would receive $3,597 a month if I wait until age 70 to retire. That’s $1,430, or 65% more per month for the rest of my life vs. if I began collecting right now.

Bottom line: If you wait until you’re 70 years old, you will receive 60%-plus more than if you started collecting Social Security at age 62.

If you want to see what your Social Security payment will be, go to ssa.gov. Its free, despite the several hoops you’ll need to jump through to verify your identity. But don’t let that stop you finding out how much you’ll get paid!

I’m still happily working, so there’s no reason for me to start collecting Social Security. But everybody’s situation is unique, so take the time to figure out exactly what you stand to receive.

Best wishes,

Tony Sagami