|

As a child, Labor Day was my favorite holiday of the year.

I was raised on a small vegetable farm near Tacoma, Wash. For those who don’t know, growing up on a farm is a lot of work. So, Labor Day was a BIG holiday for my family.

Not because it meant barbecued hot dogs, swimming at a lake, baseball games or a family vacation, but because it meant that school was about to start.

You see, when you’re raised on a farm, summertime means getting up early and working until the sun goes down. School, however, was a welcomed change from the three months of hard, physical work on the family farm.

|

Sitting in class and hanging out with my friends was infinitely more fun than breaking my back in the farm fields under the hot sun.

We still had to work on Labor Day, though. There was always lots of work to do done. Heck, I think my father worked us extra hard because he knew that his quasi-free labor was about to vanish.

President Grover Cleveland made Labor Day a federal holiday in 1894 as a tribute to American workers who were routinely working 12-hour days and seven-day weeks.

My father never got that memo. He worked grueling 12-hour (or longer) days, seven-days a week until his health failed him in his late 80s.

You see, my father truly considered hard work and long hours to be a godly virtue and he thought his sons should do the same, which is why my brother and I cheered the start of every new school year.

Another reason my father worked until his late 80’s was that he never made much money. He didn’t have a choice. He had to work long and hard because he didn’t have any retirement savings to speak of.

But in today’s world, retirement has become far more commonplace. We’re very fortunate.

So, what about you? How much money have you saved? How much do you think you need to save to fund a comfortable retirement?

According to a new survey by The Charles Schwab Corp. (NYSE: SCGW), Americans between the ages of 25 and 70 feel they will need $1.9 million to comfortably retire.

The dollar amount changes by generation. Millennials and Gen Xers believe they need to save $2 million, while older baby boomers think they can get by with $1.6 million.

Here’s the problem: Only 37% of those surveyed think it’s likely they will be able to save that much money.

|

| Source: Business Insider |

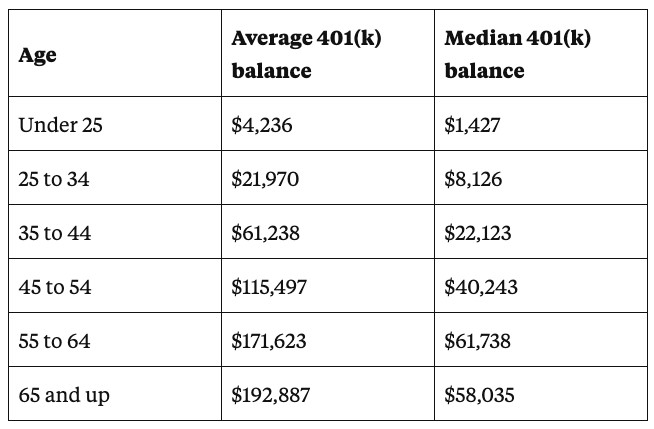

According to The Vanguard Group, the average 401k balance today is $92,148; a far cry from the $1.9 million savings goal. The median account balance is far lower; a paltry $22,217.

I found it difficult to save money when I was raising my four children. Kids cost a lot of money!

But I started saving like a madman in my personal pension plan after I put them through college.

And you can too. In 2020, the maximum contribution limit for a 401(k) plan is $19,500. If you’re age 50 or older, you can add another $6,500 to your account using the catch-up contribution provision. That’s $26,000 a year.

Here’s the bottom line: Get serious about saving money. Otherwise, you won’t have any savings, like my father. Heck, he may even put you to work on his farm.

Best wishes,

Tony Sagami