|

Tomorrow, as tens of millions of citizens queue up at the polls, three forces are converging on America.

The first force is social — extreme levels of inequality unlike anything we’ve ever seen before in this country.

I’m not talking just about the rich vs. the poor or even millionaires vs. the middle class.

This story is also about billionaires (the top 0.01%) squeezing out millionaires (the top 0.1%).

|

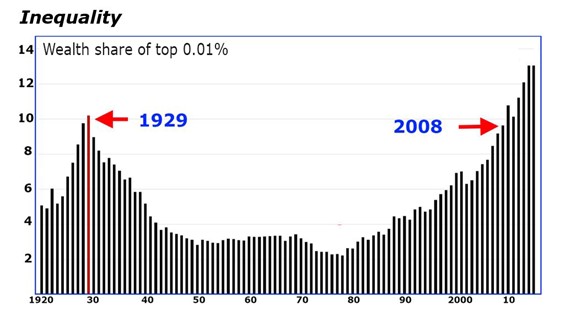

The wealth share of the top 0.01% — one out of every ten thousand households — reached the extreme nosebleed level of 10% only twice before:

- In 1929, on the brink of the Great Depression and

- in 2008, in the early days of the Great Recession.

But today, their wealth share is even greater, the worst in recorded history.

The cultural divide in America is unprecedented.

The American middle class is squeezed.

But this did not begin with President Trump or even with President Obama. It reared its ugly head many years before, especially at the turn of the new millennium.

The second force is political — the most extreme political division and dysfunction since the Civil War.

How extreme?

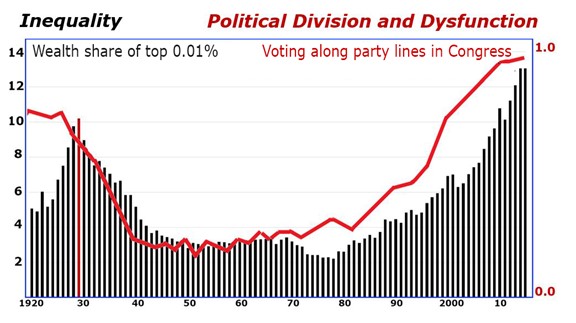

We know the answer thanks to an exhaustive historical study of the voting record in Congress (red line in chart below).

|

For about half a century, between the 1930s and 1980s, members of Congress crossed party lines and voted on the issues at least two-thirds of the time.

Today, it’s precisely the opposite. They vote strictly along party lines nearly all of the time.

That’s also far more extreme than it was in 1929 on the brink of Great Depression … or in 2008 in the early days of the Great Recession.

And it should come as no surprise that the extreme political divide in America coincides with the extreme social divide.

One feeds on the other.

Meanwhile …

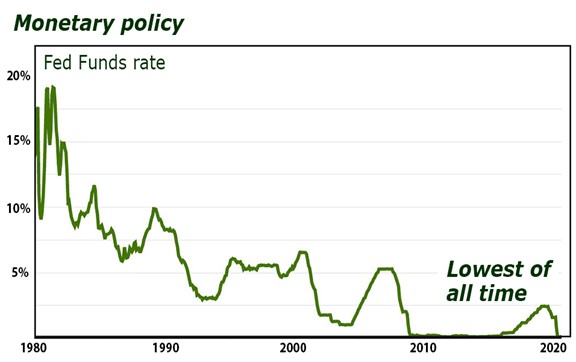

The third force is monetary — the Fed’s unprecedented money printing and the lowest interest rates of all time.

|

Most observers think the Fed’s crazy actions are simply a reaction to the Covid-19 crisis or the damage it has done to the economy.

But this phenomenon also began long before Trump or Obama; the Fed has been artificially crushing interest rates since the early 2000s.

Why?

One reason was massive debts. The other was precisely the forces I’ve just told you about — the social and political divide in America.

The Fed knew they made our society — and the entire nation — far more vulnerable than ever before.

So with each new threat of decline, the Fed printed more and more money and drove interest rates to lower lows.

Each Fed Chairman — from Greenspan to Powell — knew full well what he was doing. And each justified his extreme actions with the same basic rationale.

“Had we not intervened so aggressively,” they say, “the economy would have surely fallen into a great depression, and God knows what that would have done to our society, our politics or our standing in the world!”

Even former Fed Chairman Paul Volcker admitted as much when I talked to him in 2008 at the height of the Debt Crisis.

“In all my lifetime,” he confessed, “I would never have dreamed the Fed might do something like this. But it’s pretty obvious that the alternative is far worse.”

Or is it?

Did the Fed really prevent the decline of America? Or did it inadvertently deepen that decline?

Did the Fed’s ever-larger money-printing binges resolve the inequality and political division? Or did it merely make them worse?

As you watch the results of the election tomorrow night and in the days ahead, keep these questions in mind.

Then seek to map out your finances with a broader understanding of how these powerful forces impact your future.

The extreme inequality.

The extreme political division and dysfunction.

The extreme monetary policy.

Regardless of who wins the election, the nation will remain sharply divided between rich and poor.

With a weakened middle class.

Regardless of who wins the election, the nation will remain sharply divided between left and right.

Often ungovernable and vulnerable to turmoil.

Regardless of who wins the election, you need to build a shield of safety around your assets.

With cash, with money alternatives like gold or Bitcoin and with special strategies that can build your wealth even in the worst of times.

That’s the unique kind of guidance we’ve always provided no matter who occupies the White House. And it’s the guidance we’re committed to providing no matter who’s inaugurated on Jan. 20.

Good luck and God bless!

Martin