Wisely Assess Your Retirement Funds Amid Market Mayhem

|

“Slow down,” I said to my panicked friend on the phone. “What’s the problem?” I asked.

“I was all set to retire in May, but my 401k has lost more than $1 million dollars,” he cried, “and now I can’t afford to retire!”

I’m sure there are lots of Americans in the same boat as my friend, who saw his 401k fall from almost $3 million to $2 million in just two months.

Maybe you don’t feel sorry for my friend because he still has $2 million, but he has been diligently socking away 15% of his salary for more than three decades. And instead of enjoying his dream retirement, he will likely need to work another five years to re-build his retirement nest egg.

Talk about a serious kick in the retirement nuts!

The good news for my friend is that, according to a Charles Schwab survey, the typical American will spend around $1.7 million in retirement. Which means that even his corona-whacked portfolio is still enough for him to retire on.

Maybe he won’t be flying business class or staying in five-star hotels. But his savings combined with Social Security is more than enough to live comfortably on.

|

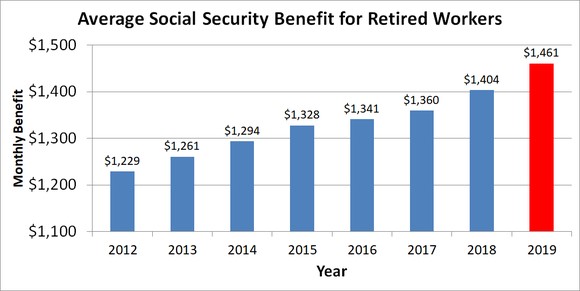

The average Social Security benefit today is $1,503 a month. That number will go up or down depending upon your earnings history. My friend, a successful corporate executive, will receive the maximum, which is currently $3,011 a month.

That’s right; $3,011 a month.

After I figuratively talked my friend down from the bear market roof, we discussed what he should do today with his portfolio. So today, I’m going to share with you what I told him.

Managing Your 401(k) for Those Nearing Retirement

For my friend (and maybe you too), the damage is already done. So, what I recommended to my friend was to raise enough cash that he would be able sleep at night without worrying about the stock market.

That amount will be different for everybody, but my friend is going to cash out 5% of his portfolio each week, for the next seven weeks, which will get him 65/35 portfolio of stocks and cash.

And then he is going to invest 100% of his new 401k contributions into a S&P 500 index fund until he does retire, sometime in the next three to five years.

If you have fewer than three years until retirement, I think you should set aside at least one-third of your portfolio in safer investments, such as a money market fund or short-term bond fund.

Managing Your 401(k) for the Young

Stick with stocks. If you’re more than five years away from retirement, you have enough time to recover your losses ... and then some. You should continue to buy stocks with your future contributions because you’d be buying at a 30%-plus discount compared to just two months ago.

Bear markets are painful, but this isn’t the first and it won’t be the last. And the two most important things you can do are:

- Remove as much emotion from your investing decision-making process, and ...

- Have a clear asset allocation strategy that is appropriate for your time frame and personal tolerance for risk.

These two steps are key to helping you weather any market storm.

Best wishes,

Tony Sagami