Large Auto Insurers in New York Closed Nearly Half of Liability Claims in 2025 Without Payment to Policyholders

PALM BEACH GARDENS, Fla., April 21, 2026 — Weiss Ratings, the nation’s only independent rating agency covering the insurance industry, has released a special report revealing an increasingly hostile insurance market facing automobile drivers in New York State.

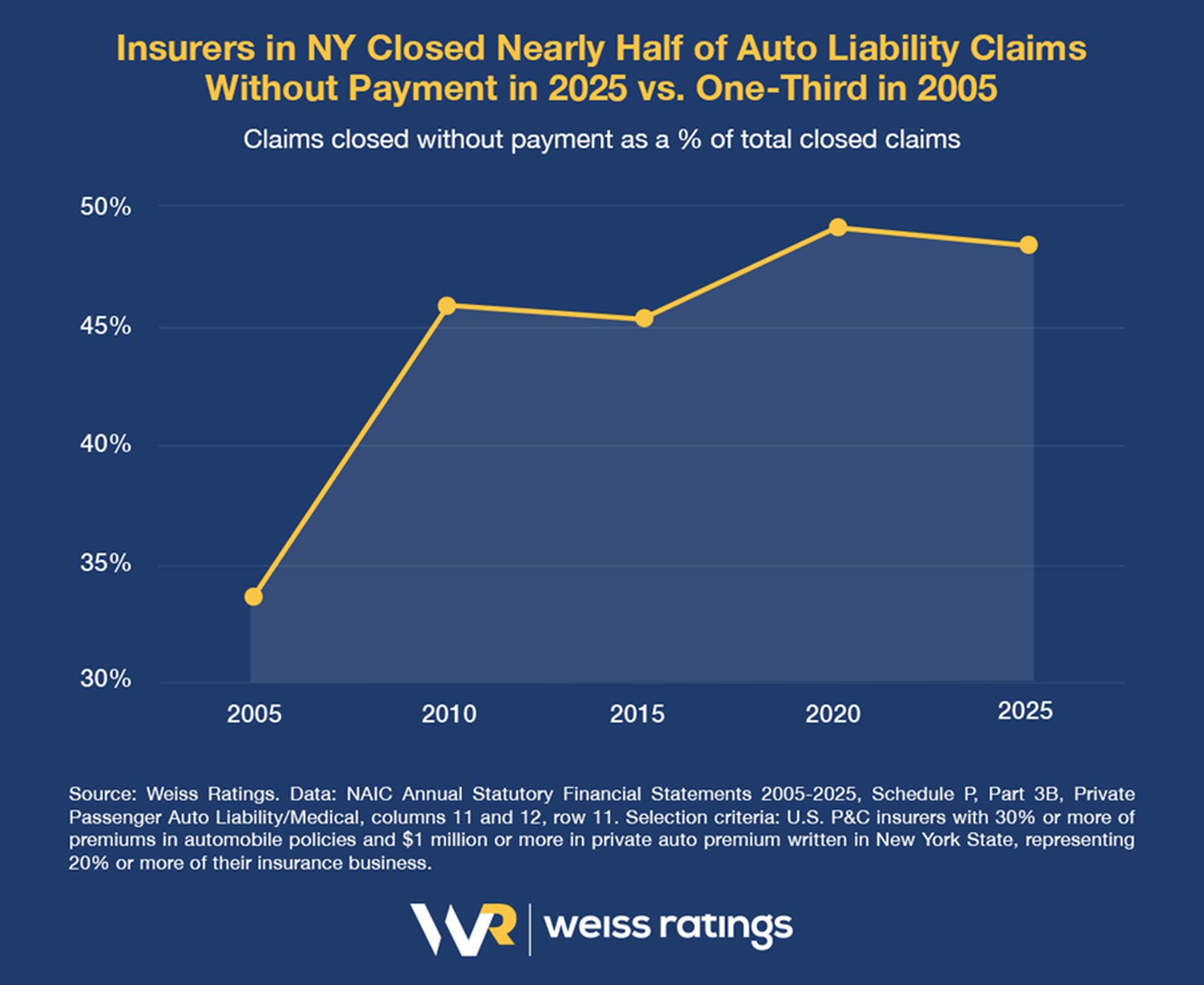

The report, requested by Citizens Action of New York, shows that auto insurers operating in the state closed 48.6% of liability claims in 2025 without payment to policyholders, up substantially from 33.6% in 2005.

Allstate Insurance (domiciled in Illinois) was among the worst offenders. It opened and closed 1,243,516 private auto liability claims in New York State in 2025. And among these, it closed 689,832, or 55.5% without payment.

Progressive Max Insurance and its sister company, Progressive Advanced (OH), each closed 47.4% without payment.

Progressive Casualty (OH) closed 43.7% without payment.

And several others closed more than 42% — all without any payout whatsoever to policyholders.

10 Large Auto Insurers Operating in New York State That

Closed Over 40% of Liability Claims Without Payment in 2025

|

Company |

State of Domicile |

Total Claims Opened & Closed in 2025 |

Claims Closed Without Payment |

% Closed Without Payment |

|

Allstate Insurance |

IL |

1,243,516 |

689,832 |

55.5% |

|

Progressive Max Insurance |

OH |

91,929 |

43,551 |

47.4% |

|

Progressive Advanced Ins |

OH |

61,286 |

29,034 |

47.4% |

|

New South Insurance |

NC |

11,514 |

5,316 |

46.2% |

|

Plymouth Rock Assr Corp |

NY |

2,752 |

1,233 |

44.8% |

|

Plymouth Rock Assr of NY |

NY |

2,407 |

1,078 |

44.8% |

|

Progressive Casualty Ins |

OH |

669,333 |

292,273 |

43.7% |

|

Farmers Grp Ppty & Cas Ins |

RI |

15,652 |

6,773 |

43.3% |

|

Esurance Insurance |

IL |

4,714 |

2,008 |

42.6% |

|

21st Century Centennial Ins |

PA |

4,937 |

2,092 |

42.4% |

Source: Weiss Ratings. Data: NAIC Annual Statutory Financial Statement 2025, Schedule P, Part 3B, Private Passenger Auto Liability/Medical, columns 11 and 12, row 11. Selection criteria: U.S. P&C insurers with 30% or more of premiums in automobile policies and $1 million or more in private auto premium written in New York State, representing 20% or more of their insurance business, and 2,000 or more auto private liability claims closed in 2025.

In contrast, some companies — such as NY Central Mutual Fire and A. Central Insurance — were able to make payments on nearly three-quarters of claims in 2025.

“Insurance companies point to consumer fraud as one of the primary culprits,” commented Weiss Ratings founder Dr. Martin Weiss. “However, they fail to explain why unpaid claims have grown from one-third of total claims closed in 2005 to nearly one-half in 2025. Nor do they disclose how other insurers operating in the same state in the same year have been able to do a better job for their customers.”

“One of the biggest problems for New York consumers,” Weiss continued, “has been a lack of transparency by insurance companies and regulators. So, we’re glad to see that, after many years of opting out, the New York Department of Financial Services is finally joining the national Market Conduct Annual Statement (MCAS) system.”

Regulators use MCAS to keep track of how often consumers suffer payment delays, denials, policy non-renewals, and other adverse outcomes. But they do not disclose which companies are the worst and best performers, making it difficult for consumers to decide which to avoid and which to favor.

Using this lookup table, Weiss recommends that consumers review each insurer’s history of claims closure without payment before purchasing or renewing coverage — a step that has become essential in today’s market.

In its just-released report, Private Auto Owners in New York State Face an Increasingly Hostile Insurance Marketplace, Weiss Ratings provides recommendations for legislators, regulators, policyholders, and consumer advocates.

*******

About Weiss Ratings: Weiss is the only independent research organization in America that has been tracking and releasing data to the public regarding the worsening trend of claims denials by insurers. Weiss rates 60,000 institutions and investments, including safety ratings on insurers, banks, and credit unions, as well as investment ratings on stocks, ETFs, mutual funds and digital assets. Since its founding in 1971, Weiss Ratings has never accepted any form of payment from rated entities for its ratings. All Weiss insurance company ratings are available at https://weissratings.com/en/insurance.

The U.S. Government Accountability Office (GAO) reported that the Weiss ratings of U.S. life and health insurers outperformed those of A.M. Best by 3-to-1 in warning of future financial difficulties, while also greatly outperforming those of Moody's and Standard & Poor's. The New York Times reported that Weiss “was the first to warn of the dangers and say so unambiguously.” Barron's called Weiss Ratings “the leader in identifying vulnerable companies.”