You have the unique opportunity to earn 19.49% yield that’s available right now on cash-equivalent deposits.

Hard to believe?

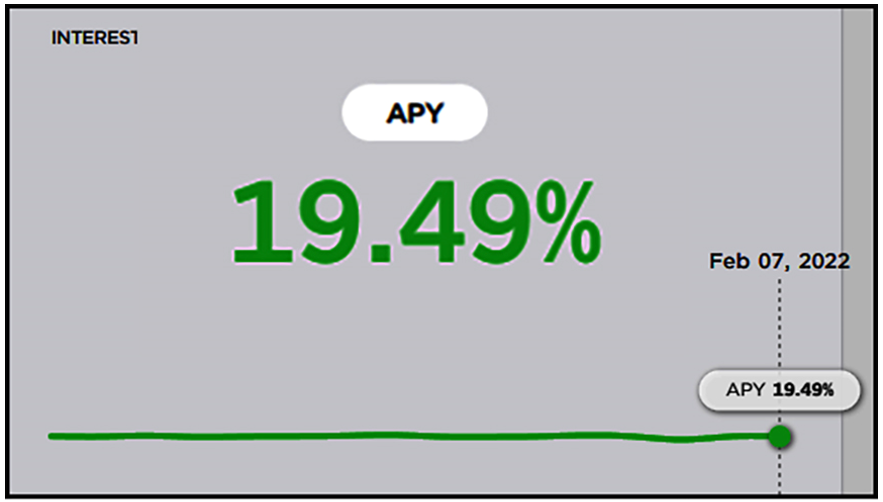

Well, below is a screenshot I took of my account earlier today:

As you can see, the yield is currently 19.49%.

Plus, in the lower right, you can see the chart shows that the yield has been pretty steady since its inception of about 10 months ago.

I feel this situation is appropriate for my savings.

Plus, for investment funds that I can afford to risk, I’ve earned even higher yields, such as 41%, 65% and even 107%.

If you’re interested in learning more about this opportunity that’s earning more than nine times the yield of a 30-year Treasury bond, click here now.

But before you decide what to do with your money, let me tell you more about what I’m doing with mine.

As a prudent investor, I don’t like to take unnecessary risks.

So …

First, I keep a big portion of my money in cash-equivalent assets.

For these funds, I want strictly savings vehicles that give me a decent yield without putting my principal at risk.

Unfortunately, though, with inflation at 7% and most savings vehicles yielding a mere fraction of a percent, that’s almost impossible right now for most people.

Let’s face it: In the traditional financial markets, either you have to take big risks ... or settle for near-zero yields.

That’s another reason why my presentation is so timely and urgent.

I provide what I consider to be one of the only viable solutions in the world today.

As I showed you with my screenshot, it’s available right now and currently paying me 19.5% annual yield on my cash-equivalent deposit, while still protecting my principal from downside risk.

With that alone, I’m already making far more on my savings than virtually anyone else I know.

Second, I allocate a smaller portion of my funds to a special kind of deposit that ...

A) Protects half my principal from price risk, while …

B) Allowing the other half to fluctuate up or down with the market.

In years past, you could make pretty good yields with high-rated dividend-paying stocks and corporate bonds.

But nowadays, both are questionable. Their average yields are far below the inflation rate — 1.3% on S&P 500 stocks and 3% on high-grade corporate bonds.

Even junk bonds yield only 4.4%.

And with the Federal Reserve planning several rate hikes this year, there’s growing downside market risk in both stocks and bonds.

My solution are deposits that have offered 41%, 65%, even 107% annual yields plus capital gains potential.

But needless to say, with the chance for capital gains also comes the risk of loss. That’s why I keep my allocation to this category relatively small.

The rates I cited above (19.5% with principal protection and 41% or more with principal risk) are not locked in.

They can go up or down.

But I consider that an advantage, because it also means I don’t have to lock up my funds. I can withdraw the money at any time without penalty.

Our Step-by-Step Guidance

Now, claiming these high yields isn’t quite as simple as opening a bank or brokerage account. There are quite a few extra steps involved.

So, to help investors get started, we’ve created a series of video tutorials. If you’re comfortable making bank transfers or investing online, I think it’s very doable.

And for my own money, even if I can earn just half the yields that are currently available, I feel it’s definitely worth the extra trouble.

So far, I’ve deposited close to $100,000 — enough to earn nearly $20,000 in yields in the first year alone!

And I soon plan to add another $900,000 into opportunities like these.

I provide more info in this video, and I suggest you watch it carefully from beginning to end.

And I suggest you do so soon. This important video will be taken offline at midnight Eastern tonight.

Good luck and God bless!

Martin