Don’t Time the Market — Spend Time in the Market

|

| By Kenny Polcari |

I hate it when someone preaches to me. So, I will do my best not to do the same to you.

But as a baby boomer, I need to get something off my chest, especially to those in the younger generations.

With age comes wrinkles and gray hair, but most important, it breeds wisdom. The more experiences you live through, the better equipped you are to handle similar situations that come your way.

That is especially true for navigating hardships — when I think it is better to be street-smart than book-smart.

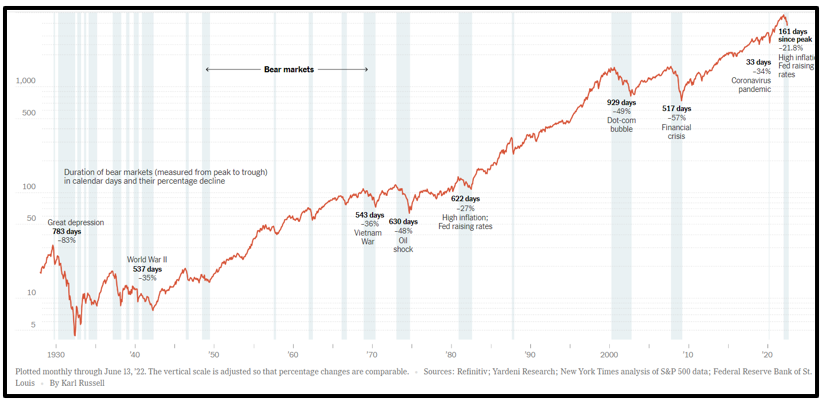

Think about it. You can read a zillion pages about lessons learned during the Dot-Com Bubble that inflated from 1995 to early 2000, then ushered in the longest bear market in history. But reading about it is not the same as experiencing it.

Click here to view full-sized image.

In fact, until you live through a bear market, you will have no idea how destructive it can be, how you will react or how your investment strategy would fare. You can only go by third-person accounts.

I have invested successfully during bears, and I have also failed and walked away all the wiser.

I have also lived through inflationary times that make today’s 6.2% rate laughable. I have watched the Federal Reserve hike and lower rates with apparent reckless abandon and felt the personal financial pain because of them.

And just because you have not lived through the toughest of economic times does not mean you are immune from the pain. In fact, those unprepared — and a little naive — may suffer worst of all.

I am here to make sure that does not happen to you.

While the stock market is a forward-looking mechanism, meaning that investors often ignore the past and what’s happening now while focusing on the future, economists go straight to history for glimpses of what to expect in the future.

But before we do that, let us first look at …

The Market’s Present

After stronger inflation data released last week — both the Consumer Price Index and the Producer Price Index — I said to myself that the narrative on Wall Street has to change.

What I mean is that stocks need to reprice based on this latest data and continue to do so as the conversation matures.

The squawking began on Friday and has carried over big-time into this week.

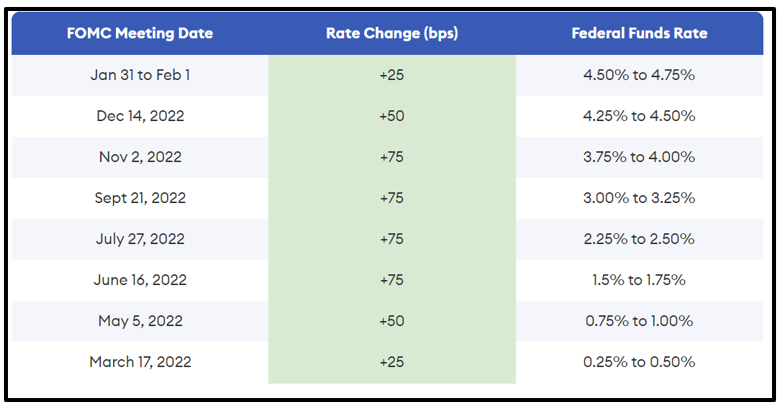

I have been saying for quite some time that while inflation was trending lower, I was afraid that it was going to rear its ugly head again if the Fed eased up, and they did just that by going from 75 to 25 basis points in a less-aggressive move on Feb. 1.

Click here to view full-sized image.

While I would rather not see rates rise, the fact is they are going up because inflation has become sticky in places that will not necessarily respond until rates are high enough to break it, and 4.25%–4.5% is not doing it; 4.75%–5% is not doing it; and 5%–5.25% probably will not, either.

Just how high will the Fed be willing to go and at what expense? As high as it needs to go.

Now, it is time to look at …

The Market’s Past

History shows that we have been in this position before. It is exactly what happened from 1979 to 1981, and I can remember it like it was yesterday.

To be specific, the U.S. had really sticky inflation. We had rising wages that forced prices higher in what would become a wage-price inflation. We saw inflation trend lower, until it didn’t. When it turned up again, it did so with a vengeance.

Unemployment rose to 10% while inflation surged to 13%, forcing then-Fed Chair Paul Volcker to do the unthinkable: Push rates to 21% to “break it” — and break it he did.

The U.S. fell into a deep, two-year recession. The market got crushed, housing got crushed and money-market funds became the investment of choice.

That is because all you had to do was put your money in a certificate of deposit, and you earned a guaranteed 21%. You slept great and had nothing to worry about as $100,000 turned into $121,000 in 12 months, and $500,000 soared to $605,000. It was magic.

The question of the year became, “Why would anyone put money into stocks in that environment?” The answer? They didn’t.

In 1980, 10-year Treasurys were yielding 13%, 2-year Treasurys paid 15.3% and 1-year CDs offered 20%+. The economy was ugly with a capital UGH. Just ask any boomer or anyone from the silent generation, comprising people born between 1930 through 1945.

You see, Gen Xers, millennials and Gen Zers cannot understand it — and it is not their fault because they didn’t live it. All the more reason to pay close attention to someone who did live and experience it.

The Market’s Future

Now, I am not suggesting that the Fed is going there, but I am suggesting that no one should be surprised if rates continue to go up, because historically, even 6% would be considered normal.

That may be quite a shock for those who only know 0% savings rates and 3% mortgages.

And last Friday, when the narrative finally changed like I said it needed to, Treasury prices declined and sent the 3-month yields to 4.8%, the 6-month to 5%, the 1-year to 5%, the 2-year to 4.7% and the 10-year to 3.9%.

The current S&P 500 dividend yield is just 2%, maybe a bit less, with lots of short-term risk. Are you still asking why stocks went down?

Look, the idea that the Fed is going to pause and then pivot has to stop. Pivoting would suggest that the economy needs stimulation. Do you really think the economy is so weak that it needs stimulation? Too much of that sort of thinking is what got us where we are in the first place.

I don’t mean to be a downer, but there is no reason to sugarcoat things.

Fortunately, there is light at the end of the tunnel, but you have to be in it to win it. That means being prepared to experience more weakness in the weeks and months ahead as short-duration cash goes into high-yielding Treasurys before it flows into stocks.

It also means not chasing profits or trying to time the market. I have learned through all my years of experience that timing the market is a losing game.

Instead, I suggest spending time in the market with names that can weather storms and turn shareholders into winners when the tide turns.

And when the Fed — or a wise boomer — tells you time and time again that rates will continue to rise until we see inflation at the 2% target, take it to heart and be smart. Now is not the time to take chances. Take a trip to Las Vegas and put a few coins in a slot machine for that.

Remember, even if it feels like you have all the time in the world to grow your wealth, there is no reason to lose money unnecessarily.

Just don’t make me say, “I told you so.”

To your wealth & wisdom,

Kenny Polcari

P.S. The Fed’s actions should have investors concerned for their financial well-being.

Starting as soon as May 2023, its insidious “Fed Control” powers could go live, which means that any accounts linked with the U.S. banking system could soon be at risk for surveillance of all transactions … or worse.

Investors who want to take action to protect their money should click here for four steps to take now to stay safe and grow their wealth.