Alphabet Shareholders Should Not Fear an Antitrust Case

Federal prosecutors are rushing to bring an antitrust case against Alphabet Inc. (Nasdaq: GOOGL, Rated “B-”), the parent company of Google. Oddly, the haste may be good news for the search giant.

According to a Wall Street Journal report Tuesday, some Justice Department staffers worry political expediency is endangering the chance of winning a once-in-a-generation lawsuit.

Regardless of what happens, it’s a win for shareholders.

This is not the first rodeo for Google. The Mountainview, Calif.-based company has been in the crosshairs of politicians and regulators for nearly a decade. It’s part of the territory when a company dominates a category with best-in-class products.

The Federal Trade Commission, starting in 2011, spent two years building a case against Google for favoring its own products in search results. The company argued its innovations benefited users with lower prices and better products. In the end, Google made some minor concessions, allowing online advertisers to use rival websites to manage ad campaigns. This led five FTC commissioners to vote unanimously to drop the case.

The current case against Google is mostly about the same issues. Rivals say Google is abusing its dominant search position to stifle competition, and that the company has its fingers in too many parts of the internet advertising ecosystem.

Related post: Why the Next Google … Is Google

Justice Department lawyers have been working through millions of pages of documents, the Journal notes, but they’re still not sure they have a winnable case, especially given the timeline.

Attorney General Bill Barr is hoping to make a decision by the end of the summer.

That’s going to be a problem. Google has a strong case to make it is not stifling the competition. Other internet search engines exit. End users simply choose not to use them.

Google is one of those rare products that so defines the category, its name is synonymous. Some 24 years after the search engine was introduced, the product maintains 92% of the global search market, according to a July report from Statcounter, an online analytics firm.

But the clear dominance in this area doesn’t translate to others where the company faces fierce competition.

Take, for example, the complicated situation in digital advertising. While Google grabs 73% of search ad revenues, Amazon.com, Inc. (Nasdaq: AMZN, Rated “B”) is currently at 12.9% and growing fast. And, as eMarketer notes, Google’s market share is falling quite rapidly.

The bottom line is, should the case go to court, Google’s lawyers have a winnable case that will only benefit the company. If the government case is rushed because of politics, the odds of success increase exponentially.

That’s one potential outcome. The other is the ultimate break up of Alphabet. That would actually be even better news for shareholders. Why? Because …

The sum of the parts is worth way more than the current whole.

Keep in mind, it’s not like managers at Alphabet haven’t been planning for dissolution. When the company reorganized in 2015 as a conglomerate, Ruth Porat was hired as chief financial officer. In her previous role at Morgan Stanley (NYSE: MS, Rated “C+”), she was a powerful voice in investment banking.

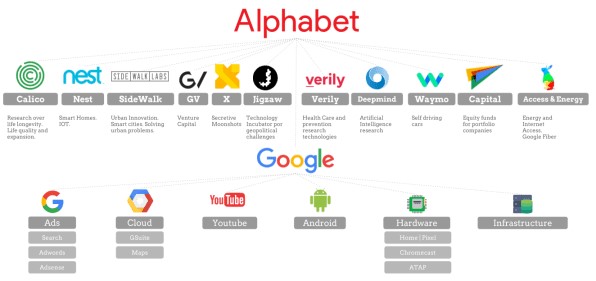

And although Sundar Pichai is chief executive officer at both Alphabet and Google, most of the company’s other businesses are run as independent companies. They have chief executives, boards of directors and even the ability to raise outside investment.

Some of these, like Google and YouTube, are extremely well known and valuable. They could be standalone public companies today. Others, such as Waymo (self-driving cars), Google Cloud (cloud computing infrastructure), GV (venture capital), Verily (life sciences), Calico (biotech research and development) and Loon LLC (rural broadband) are works in progress.

Related post: Proposed Privacy Rules Threaten Tech Giants

Still, in 2018, Morgan Stanley did value Waymo at $175 billion. And Google Cloud is on a $10 billion annual run rate and growing quickly after bringing on Thomas Kurian as chief executive officer, a talented ex-Oracle Corp. (NYSE: ORCL, Rated “B”) executive. So, even these less prominent businesses have tons of potential.

Alphabet shares trade at 27.5 times forward sales. An investment in the shares today is like getting all of these parts for free. In my opinion, any hint of a breakup would send the stock soaring.

Investors should not worry about antitrust investigations. Use any weakness to buy.

Best wishes,

Jon D. Markman