The Chipmaker That’s Set to Rule Contactless Payments

The iconic magnetic stripe on the back of credit cards is going away. And it is a big deal for more than most investors understand.

Executives at Mastercard (NYSE: MA) just announced that, beginning in 2024, newly issued credit cards in most markets will no longer require a magnetic stripe. The cards will depend fully on chip technology.

But this is the beginning of a trend, not the end. And it’s one that investors should consider getting on board with.

The so-called magstripe on the back of most credit cards harkens back to older technology. Swiping a card for purchases seemed like an evolution when the technology was developed in the 1960s by International Business Machines (NYSE: IBM). At the time, magnetic strips were needed to verify customer cards against fraudulent ones that were popping up at shopping malls and gas stations.

But modern credit cards have both a magstripe and EMV chip technology on board.

A study by EMVCo, an industry group founded by Europay, Mastercard and Visa, found that 86.1% of global payments are now made using chip technology. Customers prefer the chip because it allows them to simply tap the card on a compliant terminal. No swiping. No entering a pin.

Related Post: How Shopify built an E-Commerce Powerhouse

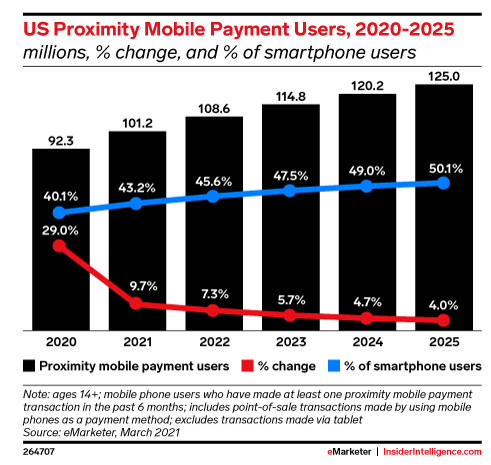

Contactless payments grew in popularity over the past year, aided in part by COVID-19. And there’s no indication of that slowing down, even if the pandemic eventually does. According to TechCrunch, by 2025, half of all smartphone users will be using contactless payment.

And the trend mirrors others associated with generational demographics. Over the past year, adoption of contactless payment was most popular among millennials and Gen Z. The latter, according to TechCrunch, “is expected to account for more than 4 million of the total 6.5 million new mobile wallet users per year from 2021 to 2025. Millennials, meanwhile, will continue to account for around four in 10 mobile wallet users.”

The financial services industry sees even bigger benefits.

In addition to reduced fraud, payment cards that use chip technology also hold the key to better biometrics and coordination with connected devices. In March, Mastercard and Samsung announced the joint development of a card with a built-in fingerprint scanner. And in the past, Mastercard executives have talked about coordinating personal payment information with vehicles to pay road tolls, refueling charges and even maintenance.

To get there, merchants and banks need to move away from the magstripe.

That process started in 2015 with something called the EMV liability shift, an incentive for American retailers and banks to start supporting EMV technology. Following the shift, merchants who did not support EMV tech became liable for fraud.

The Chipmaker Poised to Dominate

NXP Semiconductors (Nasdaq: NXP) is the world’s largest producer of EMV chips used in credit and debit cards.

The Dutch company is the co-inventor of near field communication (NFC), the chip technology used to make contactless payments secure. The intellectual property is used by every smartphone maker in the world. Yet this is only half of the story.

Point of sale manufacturers also need to license NXP technology. When magstripe finally goes away completely, every new POS will have this tech.

The total addressable market for NFC has grown from only $9.5 billion in 2017 to a projected $25.5 billion this year. Statista notes the 2024 projected market is $47.3 billion.

Related Post: Why Billionaires Are Winners

NXP will dominate the NFC market.

At the same time, executives have been careful to build other products around this important IP.

Lars Reger, chief technology officer, highlighted in January the company is working closely with Amazon.com Inc. (Nasdaq: AMZN), Alphabet Inc. (Nasdaq: GOOGL) and all of the major auto manufacturers to incorporate payment IP with smart home digital assistants and vehicles.

NXP is developing an ultrawideband platform that works seamlessly with smart home software. Reger explained how an ecosystem of NXP-enabled protocols might begin making his favorite coffee as he enters his home kitchen each morning. When he’s ready to leave, other systems automatically lock the doors, turn off the lights and unlock his car as he approaches. Chips inside his vehicle recognize the encrypted smartphone is his pocket.

These products are not way off in the future: Many are in the pipeline right now. NXP is going to get a nice piece of all of it as the technology goes mainstream.

Getting rid of the magstripe might not seem like a big deal, but it’s an enormous one. It’s how the next part of the contactless payment revolution begins.

Investors should consider buying NXP into weakness.

Best wishes,

Jon D. Markman