Video Game Industry on the Verge of Massive Disruption in the Cloud

The global video game market in 2021 is expected to reach $178 billion. Now, one of the major players in that ecosystem wants to disrupt everything.

The E3 (Electronic Entertainment Expo) — the largest gaming expo of the year — ended last week with a flourish. Managers at Microsoft Corp. (Nasdaq: MSFT), an E3 mainstay, announced plans to embed the Xbox experience directly into smart televisions.

Investors need to understand what this means: One of the largest makers of gaming hardware is disrupting its multibillion-dollar console business by moving to cloud streaming.

This is like Netflix, Inc. (Nasdaq: NFLX) managers deciding in 2009 to go all-in on streaming at the expense of its extremely profitable mail-order DVD businesses, only bigger.

Game streaming is less fragmented than recorded media, with better profit margins.

Related Post: NVIDIA Wows Gamers With Next-Gen Line of Monster Chips

It helps that Microsoft owns the second-largest cloud computing business. Azure, its cloud subsidiary, is tracking a $66.8 billion annual run rate in 2021, up 50% in the second quarter year over year.

Presumably, Azure would handle the backend processing for an Xbox app that would natively run on future smart TVs.

And that’s the key. Product managers at Microsoft believe they have figured out the algorithms required to make cloud gaming comparable with standalone consoles.

According to a blog update earlier in June, gamers with a smart TV will only need a Bluetooth controller and good internet connection for the complete Xbox experience.

It’s also the ramp-up of a new subscription business model that could be worth billions.

But Microsoft will not be alone. Other big players have established beachheads. Alphabet Inc. (Nasdaq: GOOGL) launched Stadia in 2019, a gaming platform that runs solely in the cloud. NVIDIA Corp. (Nasdaq: NVDA), the leading developer of high-end video rendering silicon, has been operating GeForce since 2015. And Amazon.com, Inc. (Nasdaq: AMZN) set a priority on gaming in 2014 with the $970 million purchase of Twitch, an extremely popular game streaming platform.

Amazon Games — a division dedicated to building game franchises — has become an important part of the larger business.

Gaming is following the road map Netflix leaders successfully navigated to become a streaming media giant. Business managers at Amazon.com, NVIDIA, Google and Microsoft understand the importance of content.

As with Netflix and streaming, big tech leaders need to secure streaming rights to the games subscribers want to play.

And that’s where the true opportunity of this development lies for investors.

Enter Tencent Holdings Ltd. (OTCPK: TCEHY), a Chinese conglomerate with major investments in the world’s largest game studios, including Activision Blizzard, Inc. (Nasdaq: ATVI), Epic Games, Riot Games, Ubisoft, Bluehole, Sea Limited (NYSE: SE) and Roblox Corp. (NYSE: RBLX).

These companies produce such online favorites as “Call of Duty,” “Fortnite,” “League of Legends,” “Assassin’s Creed,” “PubG,” “Free Fire” and “Adopt Me!”.

Additionally, in 2019, Tencent secured the China streaming rights to NBA 2K League, the NBA’s eSports league.

Through its extensive portfolio, Tencent is the No. 1 global game business by revenue, according to a March investor presentation. That is an enviable position.

Statista analysts estimate that the worldwide game market is expected to grow to $268.8 billion through 2025, up from the current 2021 pace of $178 billion.

Related Post: Video Games Play With Digital Transformation

It’s true that investing in Chinese businesses carries exogenous risks. The country is ruled by a single political party. Regulatory changes occur swiftly and often without prior warning.

Tencent also operates WeChat, a Chinese super app that encompasses messaging, search, bill payments, shopping, banking, maps, mobile games and customer service communications for most Chinese businesses. The app is used daily by 88% of Chinese citizens.

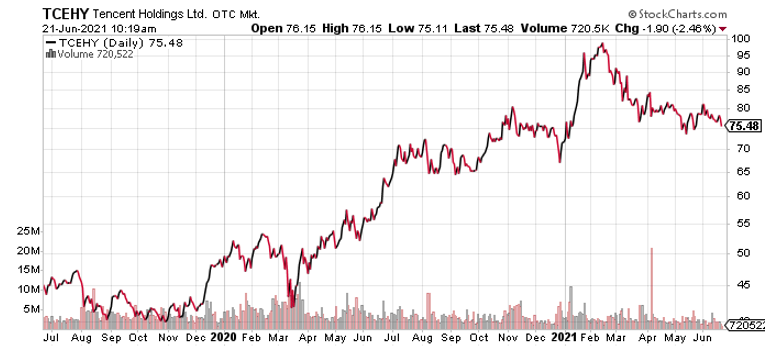

Fear of regulation is the driving factor in the current valuation: Tencent shares trade at only 33 times forward earnings and 9.9 times sales after skidding from $98 in February to around $75.40 today. That haircut makes the stock inexpensive, given that sales have grown by double-digits every year since 2010, soaring 26% in 2020.

Whatever happens, one thing is clear: The game sector is about to be disrupted.

Big players are looking to secure quality content for their new subscription businesses, and the undisputed king of content is selling on the cheap.

Longer-term investors should consider buying Tencent into any near-term weakness.

Best wishes,

Jon D. Markman