|

Since this horrific pandemic started, no industry has been hammered more than oil & gas (though restaurants and retail are up there, too). But this is part of a longer-term big bear for oil & gas, which has seen about seven years of pain.

I mean, in 2014, oil prices were over $100 a barrel. Prices collapsed to $20 a barrel this year. This was due to ...

- Oversupply

- The brief price war between OPEC and Russia and

- The collapse of demand due to the global pandemic.

Numerous oil companies filed for bankruptcy. It was a bad time.

But times change.

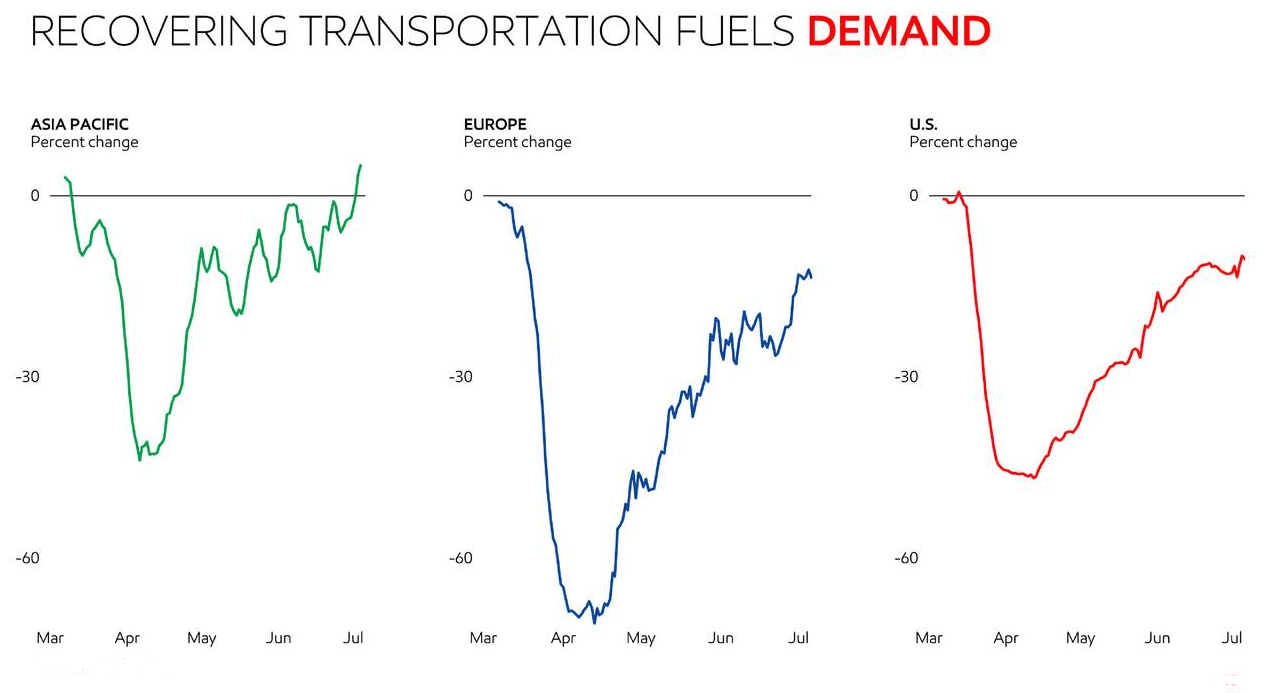

The oil & gas industry is very cyclical. We’ve coming out of one of the worst quarters ever. It’s likely that it was a bottom. Economies around the world are beginning to recover and demand for oil and oil products is returning. Here’s a chart from a recent Exxon-Mobil (NYSE: XOM, Rated “D+”) presentation, showing transportation fuel demand.

|

What’s still missing is demand from airlines and cruise ships. The general expectation is that they won’t resume regular operations until 2023.

But what if global oil demand returns to “normal” before that?

After all, China’s oil demand has recovered to more than 90% of the levels seen before the coronavirus pandemic struck early this year.

In the first half of the year, China’s imports of crude oil jumped by 9.9% compared to the first half of last year. The growth in imports between January and June was 4.9% faster than between January and March.

Obviously, China’s demand is accelerating. And analysts at Wood Mackenzie expect China’s oil consumption in the second half to grow 2.3% to 13.6 million barrels per day (bpd) from the same period last year.

In fact, demand in many emerging markets is ramping up. Not everywhere, sure. Imports of crude oil into India dropped to a five-year low in June. But generally, people around the world are learning to live with COVID-19.

Now here’s a funny thing: Last Monday, Aug. 10, OPEC began to scale back its historic production cuts, which were enacted in response to the COVID-triggered drop in demand. Traders braced for oil prices to go down on the news. Instead, prices went up.

When prices go up on what should be bad news, that’s usually bullish.

The next day, the American Petroleum Institute (API) reported a draw-down in crude oil inventories of 8.587 million barrels for the week ending July 31. Analysts had predicted a modest inventory draw of 3.267-million barrels. This was the second week in a row that saw a bullish surprise.

The API also reported a draw of 1.748 million barrels of gasoline for the week, compared to last week’s 1.083-million-barrel build. Last week’s draw also beat expectations.

Now let’s add in that oil production in the United States has fallen from 13.1 million bpd on March 13 to 11.1 million bpd for July 24. It has been at that low level for two weeks, according to the Energy Information Administration (EIA).

These are all early indicators that the oil market is bottoming.

Sure, things can go the other way. China might stop buying oil for some reason. But it’s worth taking a nibble oil.

All the best,

Sean