Hyperliquid Unseats Solana in Fully Diluted Valuation

|

| By Marija Matic |

Just two days after Mark Gough gave you the scoop on Hyperliquid (HYPE, “D”) last week, it hit a major milestone: It overtook Solana (SOL, “B-”) in fully diluted valuation (FDV).

But for most casual crypto investors, this news likely flew under the radar.

Here’s why it should be on yours …

FDV is the measure of the total value of a crypto project, assuming all its tokens are in circulation. In short, it’s a snapshot of the “big picture” that can help investors compare projects with different tokenomics.

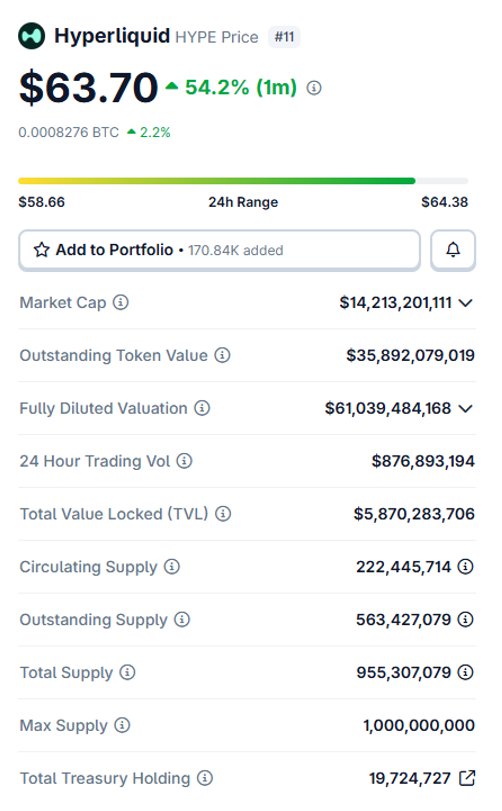

And in the time since, that gap that has only widened. At the time of writing, HYPE’s FDV sits at $53.65 billion, while SOL’s is at $51.37 billion at the time of writing.

I’ll be blunt: This is one of the more interesting developments in crypto this cycle.

First because the timing aligns with strong institutional momentum. Spot HYPE ETFs from Bitwise and 21Shares launched in the U.S. this month and pulled in over $30 million in their first week. Digital Asset Treasuries now hold roughly 10% of total HYPE supply.

That’s a level of institutional concentration that, combined with ETF inflows, is adding structural buy-side pressure on an already tight supply. Out of a total possible supply of 1 billion tokens, only 2.2 million are currently in circulation.

And Hyperliquid’s buyback and burn program is aggressive enough that new emissions won’t devalue what’s already on the market. In fact, the supply headwind that kills most altcoin rallies is running in reverse here.

Burns are funded by protocol fees, which creates a self-reinforcing loop: More trading volume → more fees → more burns → less supply → price support.

The FDV flip reflects the market pricing in exactly that.

And here’s the second reason this flip caught my eye: It shows the “fat app thesis” I explained late last year is playing out.

If you haven’t read up on it yet, I encourage you to do so. Because it explains a shift in where value will settle in the crypto markets. Which means investors like us should adjust our portfolios accordingly.

Put simply, though, the fat app thesis suggests that value will accrue on the application layer — i.e., the decentralized applications themselves — not the settlement layer, or the underlying network the app is built on.

On a 30-day basis, Hyperliquid generated $57 million in fees. That complete blows Solana’s $14 million and Ethereum’s (ETH, “B+”) $24 million over the same time, according to DefiLlama data.

A single-application chain out-earning two of the top Layer-1 networks is worth pausing on, though the comparison needs context.

Solana and Ethereum are general purpose chains, so most value gets captured by apps on top, not the base layer. For example, Pump.fun (PUMP, Not Yet Rated) alone did $77 million in 30-day fees, Lido (LDO, “D+”) did $45 million, Sky (SKY, “D”) did $32 million. And all three sit on those L1 networks.

In Hyperliquid’s case, it’s app and chain are the same thing. So, it captured ALL the value. But that also means if a competitor app ever out-trades their perp DEX, there’s no broader ecosystem underneath to fall back on.

So, if Hyperliquid can hold trading volume through the rest of this broader bear phase, the tokenomics alone make it structurally different from almost anything else in the altcoin space right now.

That’s why FDV flip is worth noting. And why savvy investors are already looking for their entry opportunity.

Best,

Marija Matić