Real Revenue Has Become the Crypto Trend of the Year

|

| By Marija Matic |

Just like most markets, crypto has its trends.

2021 was the year of airdrops. 2022 saw the non-fungible token (NFT) craze. 2024 was the year of low-float, sky-high, fully diluted value (FDV) launches that bled out the moment their unlocks hit.

We’re only halfway through this year. But the dominant trend of 2026 has already made itself known: revenue.

The market has been loud about its revenue obsession. So much so it’s created a very real, structural shift. After two cycles of tokens whose only "fundamental" was the promise of future adoption, crypto has swung hard toward projects that earn actual money.

That means real fees earned from real usage. And crucially for investors, some of these real revenue projects even return some of that money to token holders.

That’s why phrases like …

- Real yield

- Cash-flow crypto

- Buyback-and-burn

Have become the ones that move capital. And why today, we’ll take a look at which cryptos are actually at the top of the earnings table.

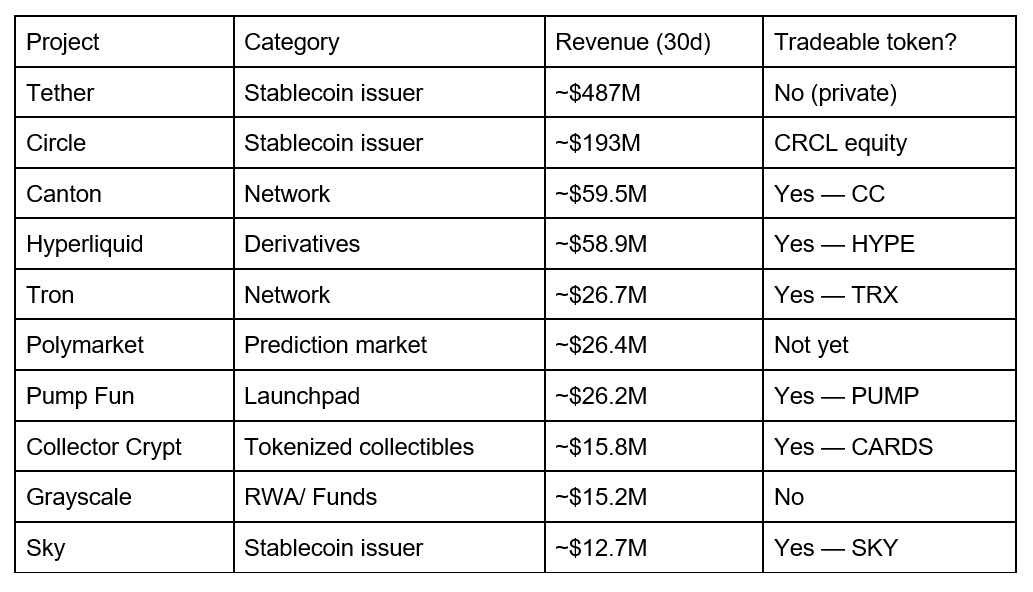

The cleanest scoreboard is DefiLlama's revenue ranking,1 which measures the slice of fees a protocol retains as opposed to the total fees flowing through it.

As of late June 2026, the 30-day leaderboard looks like this:

A note on reading this list before we get into the names …

"Revenue" here is not the same as profit, and the top of the table is dominated by businesses that aren't really "protocols" in the crypto-native sense.

The two giants — Tether and Circle (CRCL) — earn their money the boring way: interest on the Treasury bills backing their stablecoins.

That's an enormous, durable cash machine … but it tells you nothing about on-chain demand.

More importantly, neither gives a retail buyer a clean, volatile token to express a view on. So, they’re the honorable mentions, not the story.

The story, for anyone who wants a tradeable, volatile coin tied to the revenue narrative, sits just below them. Today, we’ll look at how the top three names under them actually stack up.

While you read, I want you to keep a vital question in mind: Does the revenue reach the token, and is that revenue organic or subsidized?

Canton: Institutional Plumbing with a Burn

Canton (CC, “D-”) is the highest-earning project on the list that comes with a real, tradeable token. It pulls in roughly $59.5 million over the trailing 30 days.

That makes it third overall, right behind the two stablecoin issuers.

It is not a retail playground. Canton is a privacy-first settlement network built for institutions, offering tokenized Treasurys, repo — repurchase transactions and buy/sell-backs — and synchronized settlement.

And it’s already been noticed by big players, with names like Depository Trust & Clearing Corporation (DTCC) and JPMorgan's (JPM) Kinexys building on it.

The fees it earns come from genuine institutional workflows, which is about as durable a revenue base as crypto offers.

It all runs on what Canton calls a burn-mint equilibrium. To make it work, two things happen in parallel:

-

Burn: Every fee paid on the network — which include transactions & holding fees (scaling fees that keep contracts alive for keeping contracts active) — is paid in CC. Those tokens are then destroyed.

More network usage means more CC burned, which shrinks supply.

- Mint: New CC is created and handed out as rewards to the people who keep the network running — validators, infrastructure operators and especially app builders. It’s this last group that currently receives the lion's share of rewards.

The balance between the two is the whole game.

When usage is high, burning can outpace minting and the supply gently shrinks. When the network needs to attract more participation, minting runs ahead and supply expands.

What this means for an investor is subtle but important: CC's circulating supply already equals its total supply. So by the crude "market cap equals fully-diluted value" screen, there's no lockup cliff hanging over it.

That’s a genuine benefit. But it’s not the same as "no dilution." Because the supply is effectively uncapped and new coins are continuously minted, the dilution simply takes the form of ongoing issuance rather than a scheduled unlock.

Here’s my honest take: CC's value holds up only if real fee-burn keeps pace with that emission. And the burn-to-mint ratio has been climbing.

Price action has been constructive. CC sits around 25% below its all-time high and has held firm since bottoming in early April.

For a believer in institutional adoption, it's the most "fundamentals-first" name on the board.

The catch, however, is one every Canton skeptic raises: Because the network incentivizes app builders to generate the very activity that produces fees, some unknown slice of that $59.5 million is effectively subsidized by freshly minted tokens.

The revenue is real; how much of it sticks remains to be seen.

Hyperliquid: The Cleanest Revenue-to-Token Link

If you want the textbook example of the 2026 revenue narrative, it's Hyperliquid (HYPE, “D”).

The on-chain perpetuals exchange earned roughly $58.9 million in the last 30 days. And it has built the most direct revenue-to-token mechanism in the space: 97%–99% of all trading fees are funneled into an Assistance Fund.

This fund is, functionally, an automated stock buyback system. Itcontinuously buys HYPE on the open market and removes it from circulation. The only difference is that the Assistance Fund is transparent and on-chain.

The platform has poured well over a billion dollars of cumulative fees into these repurchases since launch.

That mechanism is also why HYPE's price behaves the way it does. Abd why it's worth being precise about what the price actually depends on: trading volume on Hyperliquid exchange.

More volume → more fees → more buyback pressure → upward push on the token. Everything flows from perps volume on a single exchange.

Hyperliquid currently processes around 70% of all on-chain perpetual-futures volume. As of last year, perp volume accounted for 78% of ALL crypto trading volume.

So, it’s not surprising that Hyperliquid at one point surpassed Coinbase in notional trading volume, Needless to say, the engine has been running hot.

HYPE printed an all-time high near $77 in mid-June and has since pulled back to the mid-$60s. That’s less than 17% off the top, which is shallow by crypto standards and reflects how much buying the buyback provides.

Not to mention, it’s a strong sign of strength as the broad market is looking to confirm its bottom.

But before you buy, you need to know this bull case has two potential issues.

First, the HYPE token has a multi-year unlock schedule. Only a fraction of total supply circulates today, so the future buybacks must continue to absorb the newly unlocked coins to hold the line.

Second, quarterly buyback spending has been declining even as the price rose. That suggests if perps volume softens, the support may weaken during bearish conditions.

As one widely shared framing put it, buying HYPE is essentially a leveraged bet on one variable: Whether trading volume on a single venue keeps climbing.

Tron: Not Really a Chain Bet, a USDT Bet

Tron (TRX, “C+”) earned about $26.7 million over 30 days, all of it from network fees that are burned (TRX has its own deflationary fee-burn).

The most accurate framing of TRX is this: It is a leveraged play on Tether.

Tron is the dominant rail for settlement of Tether’s USDT stablecoin. It now carries roughly $90 billion in stablecoins, with 389 million-plus accounts and over 14.5 billion lifetime transactions.

Every dollar of USDT that moves on Tron burns a little TRX. If you believe stablecoin settlement will continue to grow — especially in emerging markets — TRX is a way to own the toll booth.

What's new and genuinely notable is the institutional and treasury layer forming around it.

A Nasdaq-listed digital-asset-treasury vehicle, Tron Inc. (TRON), has been buying TRX almost daily. At the time of writing, it has accumulated a treasury north of 700 million TRX.

Keep in mind, this is a public company bid that didn't exist a year ago.

On the adoption side, Hamilton Lane tokenized its Senior Credit Opportunities private-credit fund (HLSCOPE) on Tron via Securitize, dropping the minimum buy-in from $2 million to $10,000.

Reportedly, this is the first asset Securitize has ever issued on the network.

And Bitnomial listed a CFTC-approved TRXUSD futures contract, opening regulated U.S. derivatives trading on the token.

Think of these updates as doors into the same building for institutions: A regulated fund tokenized on Tron, and a regulated market for Tron's own coin.

Price action is solid: TRX trades around 25% below its all-time high and has been one of the steadier large caps. That fits its "infrastructure, not casino" profile.

The risk is that its fortunes are tightly bound to USDT's continued dominance. If stablecoin flows ever migrate to another chain, the toll booth will clear out.

The Bottom Line

The revenue narrative is the right one for 2026. But that means more work for investors like us.

As I mentioned last week, headline numbers are no longer enough to understand the full story. Earning fees is necessary; it is not sufficient.

We now need a sharper test to determine if revenue is real and if it’s reflected in the token’s price.

Because the names that have rewarded holders are the ones where the underlying activity is organic and revenue flows transparently and aggressively into the token.

Best,

Marija Matić

P.S. To see which real revenue coins also got Juan Villaverde’s Crypto Timing Model’s “buy” signal, click here.