|

| By Sean Brodrick |

The market is severely underpricing just how tight the physical math is on critical minerals.

There’s an opportunity there for investors, and I’ll tell you how to play it.

The fact is, critical minerals are at a critical juncture, facing supply constraints and soaring demand.

Total global consumption is expected to double or even triple between now and 2030!

Production can’t keep up, and the Chinese are using critical mineral supply as a weapon.

I’ll boil down my bullish case to five reasons.

1. Chinese Export Bans & ‘Extraterritorial’ Controls

The most immediate catalyst is China’s aggressive weaponization of its upstream dominance.

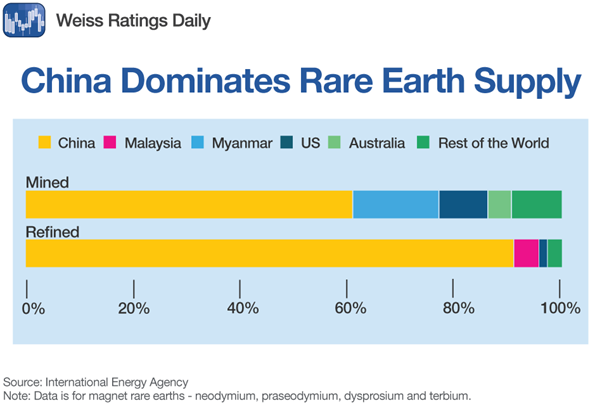

China dominates production and refining of elements essential for permanent NdFeB magnets (neodymium, praseodymium, dysprosium and terbium).

These are vital for electric vehicle motors, turbines, modern weapons and other uses.

China controls around 60% of global supply. And it makes 90% to 94% of finished permanent magnets, as this chart shows.

China also controls about 60% of antimony, 79% of tungsten, up to 80% of refined germanium and up to 99% of the world’s gallium!

Now, Beijing has shifted from minor regulatory oversight to outright economic warfare.

- The U.S. Embargo: China has placed an outright export ban on gallium, germanium and antimony, specifically targeting the United States.

- The Structural Shock: The impact of these restrictions has been devastating to Western supply chains. For example, since China restricted antimony exports, shipments dropped by roughly 97%, while global prices skyrocketed by over 200%. European gallium prices have seen spikes of over 350%.

- The Extraterritorial Trap: China implemented an extraterritorial foreign direct product rule. This means foreign manufacturers cannot sell components containing even trace amounts (0.1%) of Chinese-sourced rare earths or processed materials anywhere else without Beijing's approval.

2. Radical Supply-Demand Asymmetry in Western Defense

The U.S. and its allies face a massive structural deficit in the materials needed just to maintain basic deterrence.

Military hardware requires an astonishing volume of critical minerals, and the West has virtually no domestic production for many of them.

- Antimony: Essential for ammunition primers, armor-piercing rounds, infrared sensors and precision optics. Domestic antimony mining in the U.S. just restarted, most projects are still in the development stage, and America relies nearly entirely on imports and stockpiles.

- Gallium & Germanium: These are replacing traditional silicon in next-generation, high-performance semiconductor chips used in military radar, electronic warfare and satellite communications.

3. The Unforgiving Timeline to Production

The market consistently fails to price in the massive time lag required to bring new mining operations online.

You cannot simply flip a switch or build a digital patch to solve a physical mining deficit.

Developing a new critical mineral asset in a tier-one Western jurisdiction (like the U.S. or Australia) takes an average of 10 to 15 years from initial discovery to commercial production.

This delay is driven by permitting, regulations and more.

This guarantees that asset owners holding high-grade deposits with clear, accelerated paths to production possess immense, unpriced scarcity value.

Western governments see that value.

Uncle Sam and others are aggressively bankrolling domestic capacity and setting price floors, acting as a backstop for strategic producers.

4. High Technical Complexity & the Midstream Bottleneck

The true bottleneck for critical minerals isn't just digging the rock out of the ground — it is the chemistry required to refine it.

Extracting and separating elements like dysprosium, terbium or neodymium requires highly complex, capital-intensive chemical processing plants.

China spent decades subsidizing its midstream refining sector, intentionally running it at a loss to bankroll a near-total monopoly on processing capacity.

Consequently, even when Western mines successfully extract ore, they have historically had to ship the concentrate back to China for separation.

Building out independent, allied midstream refining is an incredibly slow and technically difficult journey.

Companies that actually own proprietary processing technology or have secured fully integrated supply chains command an extraordinary competitive moat.

5. Inelastic Demand from the Energy & Aerospace Supercycles

Outside of the defense sector, the sheer volume of material required for high-efficiency infrastructure guarantees demand.

- Grid & Data Centers: High-efficiency transformers, backup battery energy storage systems (BESS) and data center cooling frameworks rely on massive inputs of high-grade copper, aluminum and specialty alloys.

- Aerospace & Space: The accelerating space supercycle is experiencing severe rationing of materials like yttrium (vital for coating jet engine turbines) due to Chinese export drops.

Bottom Line: Wall Street consistently prices critical minerals companies using short-term commodity frameworks.

They fail to value them as the high-barrier, national security infrastructure that they actually are.

That means you can get ahead of Wall Street. And I’ve got just the fund to do it.

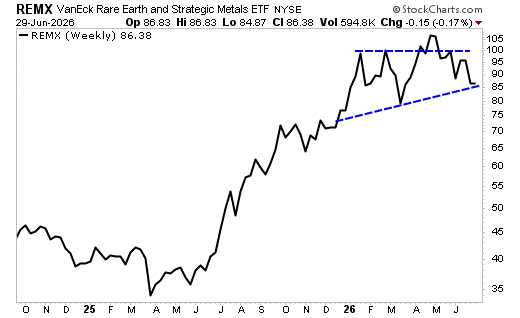

The VanEck Rare Earth/Strategic Metals ETF (REMX) holds a basket of 31 companies across the critical minerals space.

It has an expense ratio of 0.53% and a recent dividend yield of 1.3%.

You can see that REMX soared last year and then spent the first half of this year consolidating.

It’s near support, and I believe it’s going to break out and go much higher.

The math points to much higher prices in critical minerals.

Geopolitics is fueling a flood of government investment.

Get your piece of this bull before it really starts to run.

All the best,

Sean Brodrick

P.S. A 1.3% dividend yield is on the low side. But the potential for capital gains here makes it worth considering.

This combo of growing dividends and potential for quick capital gains is at the core of what Dr. Martin Weiss outlined yesterday during a special event.