|

| By Nilus Mattive |

We’re starting to see more and more headlines about so-called private credit market funds — bundles of loans tied to things like AI data centers and software companies now being disrupted by those AI data centers.

These investments are very much like the CDOs that brought our entire financial system to the brink as the housing bubble popped.

They promised relatively high returns with relatively low risk.

But they have very little transparency. And they are difficult — or even impossible — to buy and sell freely.

So, it’s no surprise that they are now showing signs of cracking.

“While sponsors insist most of the loans are sound, some estimates project a sharp rise in defaults. UBS recently forecast a 15% default rate, nearly triple recent experience.”

Most estimates say we’re talking about anywhere from $1 trillion to $2 trillion dollars in investments that could blow up and ripple into other parts of the Wall Street banking complex, setting off a chain reaction of losses and deleveraging.

In short, they’re one of the major pieces of the AI Apocalypse I warn about in this urgent new video.

But these private credit funds are really just the first layer in what is now the greatest pile of debt in mankind’s history.

The second layer? Record amounts of consumer debt, too … precisely the type of loans that will suffer under the weight of higher inflation and a slower economy.

How much debt are we talking about?

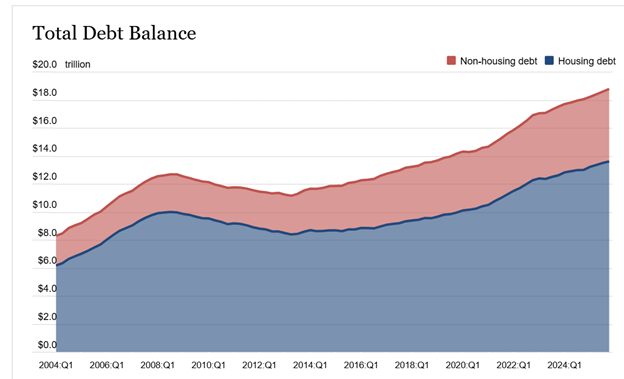

According to the Federal Reserve’s latest Quarterly Report on Household Debt and Credit, total household debt increased by $191 billion to hit $18.8 trillion in Q4 2025.

- Mortgage balances grew by $98 billion to total $13.17 trillion …

- Credit card balances rose by $44 billion to $1.28 trillion …

- Auto loan balances increased by $12 billion to $1.67 trillion …

- HELOC balances increased by $11.6 billion to $434 billion …

- And student loan balances rose by $11 billion to $1.66 trillion.

These are wild numbers, especially when you consider the fact that several trillion dollars of the loans aren’t backed by any assets at all!

Yet it pales in comparison to the mother of all debt loads … and arguably the biggest problem of all … record U.S. government debt.

While it didn’t get much media attention, the U.S. Treasury recently released its consolidated financial statement for fiscal 2025 (ended September 2025).

It showed the U.S. government piling on another $2 trillion in additional debt and interest owed over the course of the year …

Along with another $438.8 billion in federal employee and veteran benefits payable …

Leaving Washington with $6.06 trillion in total assets against $47.78 trillion in total liabilities.

Let that sink in …

Uncle Sam now owes about eight times more money than he has!

Actually, that’s not true … he owes a lot more.

Because this figure doesn’t include unfunded obligations of social insurance programs like Social Security and Medicare, which are outlined in a separate off-balance-sheet statement.

If we add in the current liabilities there — which jumped $10.1 trillion to a 75-year liability of $88.4 trillion — things get downright ridiculous:

Our federal government has IOUs of $136 trillion … five times the annual gross domestic product (GDP)!

In an excellent piece for Fortune, economists Steve H. Hanke and David M. Walker take the numbers and divide them proportionally to create the following illustration …

“[This is the equivalent of a] household that earns $52,446 and spends $73,378 — running a $20,932 annual deficit. Its total liabilities and unfunded promises amount to $1,361,788 against just $60,554 in assets, leaving it $1.3 million in the hole.”

Their conclusion?

“Uncle Sam, by any accounting standard, is insolvent.”

Yet the country spent another $30 billion to $40 billion just in the first month of the Iran War … on top of all the regular spending … with no end in sight.

I will admit people like me have been worrying about this problem for decades now.

Yet it has also been growing bigger and bigger that whole time.

The only way it can continue indefinitely is through a further devaluation of every single dollar we earn and spend.

And that’s actually the BEST-CASE scenario.

The other two choices — an outright U.S. debt default or a world where AI and robots increase productivity so sharply that regular workers become irrelevant — sound far worse.

Best wishes,

Nilus Mattive

P.S. What specific steps do I recommend taking to protect your money in the face of these threats? I lay it out very clearly at the end of this video.