|

| By Sean Brodrick |

Everyone is watching the Strait of Hormuz, waiting for it to reopen and unlock about 20% of the world’s oil supply.

But even if the Strait of Hormuz reopened tomorrow, the global supply shock has already occurred.

Inventories have been drained.

The world's emergency buffers are already shrinking.

And that means an oil shock could hit hard — even in the U.S.

Uncle Sam’s Oil Kingdom

The good news is America is the world's largest oil producer, at about 14 million barrels per day (bpd).

Saudi Arabia and Russia each produce about 10 to 11 million bpd.

America also shares borders with Canada and Mexico, two major oil-producing nations connected to us by extensive pipeline infrastructure.

On the surface, that sounds like a recipe for energy security. But oil is a global commodity.

A barrel produced in Texas can and will be sold into the same global market as a barrel produced in Saudi Arabia.

When inventories collapse worldwide, American exports ramp up. And Joe Sixpack feels the pinch at the pump.

Storage Wars

The real story is what is happening inside storage tanks.

For months, governments around the world have been drawing down inventories to compensate for the loss of Persian Gulf supplies.

The world has effectively been spending down its oil savings account.

Think about it this way: Imagine your paycheck suddenly falls by 20%.

Instead of cutting spending, you dip into your savings account.

At first, everything seems fine.

Your lifestyle doesn't change.

Your bills still get paid.

But each week, your savings account gets smaller.

That's essentially what the global oil market has been doing since the blockade of the Strait of Hormuz began, as inventories bridge the gap between supply and demand.

Most investors see reports showing billions of barrels of oil in storage and assume there is plenty of cushion left.

But much of that oil isn't truly available.

It serves as what the industry calls “system fill” — the oil required to keep pipelines operating, refineries functioning, tankers moving and distribution networks flowing.

You cannot completely empty a pipeline, operate a refinery without feedstock or run a tanker fleet without cargo in transit.

In other words, not every barrel sitting in storage is actually available for consumption.

This is where two phrases investors will soon hear more frequently come into play: "operational minimum" and "tank bottoms."

These terms describe the point at which inventories become so depleted that the system begins to experience stress.

Refiners begin competing aggressively for available barrels.

Small disruptions suddenly produce outsized consequences.

Importantly, danger arrives long before inventories actually reach zero.

And that brings us to America's Strategic Petroleum Reserve.

The SPR was created after the oil shocks of the 1970s as an emergency stockpile designed to protect the United States from major supply disruptions.

Draining the SPR

Washington has repeatedly tapped the SPR to cushion consumers from rising fuel costs and offset disruptions in global markets.

Every barrel released into the market keeps a lid on U.S. gasoline prices.

But every barrel released is also one less barrel available during a future emergency.

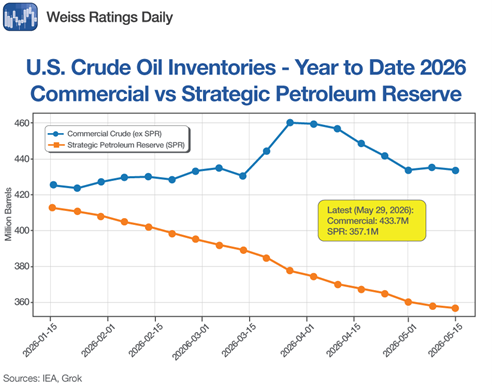

The Strategic Petroleum Reserve once held more than 700 million barrels. Now, inventories are falling dramatically.

Recent estimates place SPR holdings at around 350 to 360 million barrels, roughly half of the historic peak.

You can see the U.S. is draining the SPR to keep commercial inventories stable.

More concerning is the pace of recent withdrawals.

In several recent weeks, 8 million to 10 million barrels a week flowed out of reserves.

At that rate, more than 100 million barrels can disappear in a single quarter.

The Coming Crisis

Many investors assume the SPR can keep releasing oil indefinitely. Nope!

There is a practical floor that policymakers are extremely reluctant to breach.

Analysts estimate the United States needs roughly 180 million to 200 million barrels in reserve to satisfy international obligations and maintain a credible emergency stockpile.

Below that level, national security concerns begin to outweigh the political benefits of lower gasoline prices.

In other words, the United States doesn't have to reach zero barrels before it has a problem.

It merely has to approach what might be called “operational bottom.”

According to Brookings Institution researchers, global inventories could approach operational stress levels as soon as July if current drawdown rates continue. And industry executives are sounding the alarm.

Exxon Mobil (XOM) Senior Vice President Neil Chapman recently told a conference: “We're approaching unheard of inventory levels. I mean, really, really low levels.”

He added: “Once you get to the minimum inventory levels and all-time low inventory levels, there's only one way to go.”

Could Prices Jump 50%?

Chapman is looking for oil prices to jump another 50% once inventories hit those minimum levels.

Meanwhile, oil futures reflect widespread confidence that the Hormuz crisis will soon be resolved and normal trade flows will resume.

The market appears unconcerned … for now.

And maybe we won’t hit operational bottom in July. It might be August … or September.

On the other hand, JPMorgan (JPM) recently projected that global oil inventories could fall to roughly 7.45 billion barrels by July, the lowest level in any comparable period since at least 2017.

History shows that when inventories break through multi-year lows, prices can spike.

That's why the real risk isn't that America runs out of oil. The real risk is that America burns through too much of its emergency buffer before the global market recovers.

The Strategic Petroleum Reserve can delay a crisis. It cannot solve one.

And if inventories continue to fall while policymakers keep treating the SPR as a price-control mechanism, investors may discover that the “operational minimum” arrives long before anyone expected.

When? Maybe the real fireworks for the Fourth of July could be the drop in gasoline prices.

How You Can Play It

When oil prices were low, oil services stock snoozed.

Now, with prices above $80, oil services are waking up again.

And many oil services stocks are priced way below where they should be.

You can buy a basket of oil services stocks in the Van Eck Oil Services ETF (OIH).

Its expense ratio is low at 0.35%, it has a Weiss Rating of “C+” and it sports a 1.16% dividend yield.

While OIH enjoyed a good run this year, it peaked right before bombs started dropping in the Persian Gulf.

While it’s been up since then, it’s mostly gone sideways.

Higher-for-longer oil prices are NOT priced in.

A sustainable price surge will trigger more oil drilling. And OIH’s share price could gush higher.

All the best,

Sean Brodrick

P.S. I recently took a trip to one of the most important mines in America.

It has been a gold and silver juggernaut for over 80 years. But that’s not why I went.

There’s another metal that’s critical. And it’s found at that ancient mine.

Here’s the full story … and the two sub-$10 companies leading the way.