|

| By David Phillips |

I’ve spent five decades helping people plan their estates.

Many are surprised to find out everything that goes into it.

Estate planning is more than just making sure everyone’s heirs get what’s theirs. Though that is the No. 1 goal.

It’s also the time to make sure your well-intentioned decisions don’t create long-term consequences for those you love most.

Like for your surviving spouse or life partner.

For decades, married couples have been told that leaving all assets to a surviving spouse is the most efficient estate-planning strategy.

On the surface, it appears simple and sensible to do just that.

After all, spouses trust one another. And the marital deduction allows assets to pass without immediate federal and state estate tax.

However, simplicity is not the same as effectiveness.

In reality, one of the biggest estate planning mistakes you can make is to leave everything outright to your spouse.

That is, without understanding the limitations of that approach.

Leaving everything outright to a spouse may solve a short-term concern. But it often creates long-term vulnerabilities.

One common justification for this approach was the introduction of “portability.”

That came with the passage of the “American Taxpayer Relief Act of 2012.”

The Act allows beneficiary children to use both federal estate tax exemptions. Regardless of which parent dies last.

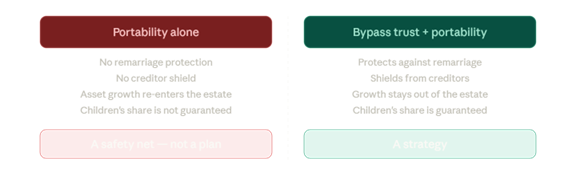

While portability has value, it is frequently misunderstood and over-relied upon.

Portability does not address many critical planning issues.

It does not:

- Protect future growth from estate taxation.

- Provide asset protection for the surviving spouse.

- Help manage how or when assets eventually pass to children or grandchildren.

- Protect assets from remarriage, creditor claims or poor financial decisions.

However …

Trust-based planning does address these gaps.

When assets are structured properly through well-drafted dynasty trusts, couples can preserve flexibility while protecting future outcomes.

Dynasty trusts can allow the surviving spouse to maintain access to income and principal. While also ensuring that assets ultimately pass according to the original intent.

This approach also allows future growth to occur outside the taxable estate, provides continuity in management and can incorporate safeguards for heirs.

Another overlooked issue is control.

When assets pass outright, the surviving spouse has complete discretion.

That may be appropriate in most cases. But it can also expose assets to unintended consequences.

Particularly in blended families or situations involving second marriages.

Proper planning allows couples to balance trust, protection and clarity.

Estate planning is not about restricting a spouse. It is about ensuring that decisions made today still work under future circumstances you cannot predict.

Leaving everything outright may feel safe. But it often shifts complexity and risk to the next generation.

A solid, properly set up estate plan lets you address questions now so that your beneficiaries won’t have to.

If your current plan relies entirely on outright transfers between spouses, it may be worth revisiting whether that approach still aligns with your long-term goals.

This article is the third in a series of the 10 most common … and costly … estate planning mistakes.

In next month’s column, we’ll examine another costly oversight: paying more income and capital gains tax than necessary due to poor asset positioning.

Questions about your estate plan?

Our office is available to help you review your current documents and discuss your options: 888-892-1102.

You can also click here to have us prepare your own personalized Estate Analysis.

In the meantime …

Live Well, Leave a Legacy!

David T. Phillips, CEO

Estate Planning Specialists

P.S. You can meet my son Todd and me at the 2026 Weiss Investment Summit this Sunday through Tuesday, May 3-5, at the Forbes Quadruple Five-Star Boca Raton resort here in sunny South Florida.

We only have a couple seats left, and we'd love it if you and your loved ones took them!