How Annual Tax-Free Gifts Can Help You Pass Along More of Your Wealth

|

| By David Phillips |

Over the past 50-plus years, I’ve worked with thousands of families from every walk of life.

Some accumulated modest estates.

Others built fortunes worth millions of dollars.

And one common theme unites them.

That is, most people spend their entire lives focused on accumulating wealth.

Yet they spend very little time thinking about how that wealth will ultimately transfer.

The result is that many families miss one of the greatest opportunities available in estate planning.

That is, strategically sharing wealth while they are still alive.

When to Share Your Wealth

Now, I am not suggesting that you give away everything you own or jeopardize your own retirement security. Doing so before you’re ready would be reckless.

What I am suggesting is that many affluent families become so focused on preserving their assets that they fail to recognize the tremendous advantages of lifetime gifting.

The irony is that the people we love most often need help long before we pass away.

- A grandchild may need assistance with college tuition.

- A child may be struggling to purchase their first home.

- A family member may be starting a business.

- Another may be facing unexpected medical expenses.

Yet, many parents and grandparents sit on substantial assets. They await some future day when those assets will eventually pass through their estate.

The question becomes: When can your wealth do the most good?

For many families, the answer is not 20 years from now.

It’s today.

The Estate Planning Opportunity Many Affluent Families Never Fully Utilize

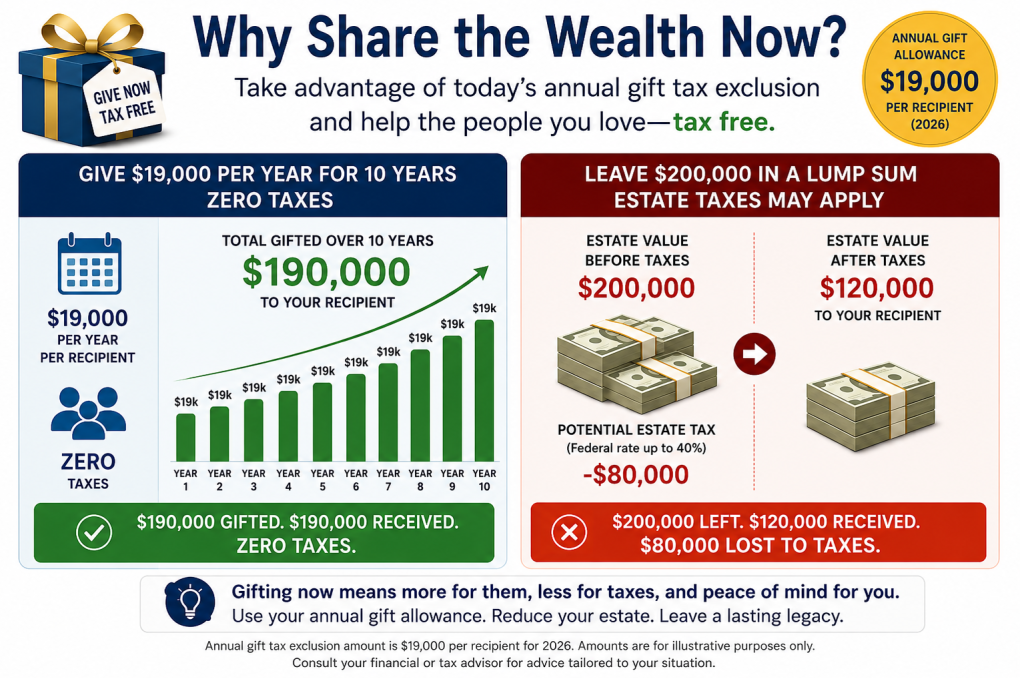

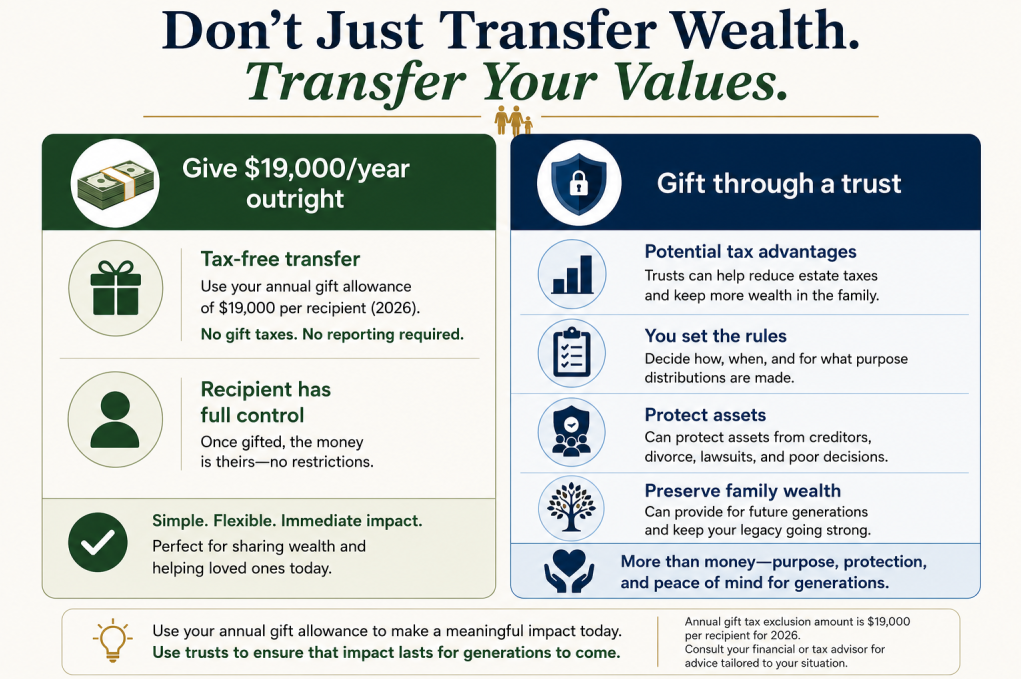

One of the most overlooked provisions in the tax code is the ability to make annual gifts during your lifetime. (Currently $19,000 per year, per beneficiary, or $15 million lifetime.)

While most people are familiar with the concept, few fully appreciate how powerful gifting can be when incorporated into a broader estate plan.

Let’s say you give your child or grandchild $19,000 a year for the next 10 years.

That $190,000 is nothing to sniff at. But look at when estate taxes get taken out.

That $190,000 can turn into $120,000 very quickly once the tax man gets involved.

So, not only is $80,000 of your savings gone. But during that time, your beneficiaries may have taken out loans (with interest) or postponed their plans …

Only to receive less than you intended them to have.

Proper gifting can benefit you as well. It can help:

- Reduce future estate shrinkage,

- Move future growth outside of your estate, and

- Allow you to witness the positive impact of your generosity while you are still here to enjoy it.

Just as important, it allows you to be intentional.

Using the previous example, if you kept your nest egg intact so that it would grow in your account …

You would have to gift $316,667 just for your recipient to walk away with that same $190,000.

That’s with all things, including the tax code, being equal.

That also assumes you get peace of mind seeing how that cash gets used.

Don't Just Transfer Wealth. Transfer Your Values

One of the greatest concerns I hear from clients is not whether their children or grandchildren will receive an inheritance. Their concern is whether those assets will be used wisely.

That concern is valid.

History is filled with stories where sudden wealth creates unintended consequences. Fortunately, proper planning can address many of those concerns.

Estate planning is not merely about transferring assets. It is about transferring values.

The most successful families understand this principle.

They do not simply leave money behind. They create a trust or another plan that reflects their beliefs, goals and priorities.

Giving Is Easy. Giving Wisely Takes a Plan

Unfortunately, many families never have these conversations.

Instead, they postpone planning year after year because they believe they have plenty of time. They assume they will eventually get around to reviewing their estate plan, discussing gifting opportunities, or updating their documents.

Then life happens.

Health changes.

Tax laws change.

Family circumstances change.

And opportunities disappear.

This is why procrastination remains one of the greatest threats to wealth preservation.

Another mistake I frequently encounter is random gifting.

- A parent writes a check here.

- A grandparent helps with a car purchase there.

While these gestures are often appreciated, they rarely fit into an overall strategy.

A thoughtful gifting plan should work alongside your retirement plan, your estate plan, your tax planning and your long-term family goals.

Every family is different.

The right strategy for a retired couple with a $1 million estate may be dramatically different from the right strategy for a family worth $10 million.

That is why cookie-cutter solutions rarely work.

America’s 250th Birthday Is a Good Time to Review Your Financial Independence

Before discussing gifting strategies, it is important to answer several key questions:

- How much income will you need throughout retirement?

- What assets do you currently own?

- How are those assets titled?

- What tax liabilities may exist?

- What happens if one spouse dies unexpectedly?

- How much of your estate could ultimately be lost to taxes, probate costs or inefficient distribution?

Most people simply do not know the answers.

That is where proper planning begins.

One of the most valuable services we provide is a personalized Estate Analysis.

By taking a snapshot of your current situation, we can identify potential weaknesses, uncover opportunities and help determine whether gifting strategies make sense for your family.

Many clients are surprised by what they learn. Some discover opportunities they never knew existed. Others find risks they never knew they had.

But almost all leave with greater clarity.

Estate planning is not about predicting the future. It is about preparing for it.

The families that achieve the best outcomes are rarely the families with the largest estates. They are the families who act before circumstances force their hand.

If you have not reviewed your estate plan recently, or if you are curious whether gifting strategies could benefit your family, now may be an excellent time to schedule a personalized Estate Analysis consultation.

Our office would be happy to help you evaluate your current plan.

Together, we can determine whether there are opportunities to strengthen your family's financial future while you still have the ability to guide the process.

Call our office at 480.899.1102 to schedule a time to discuss your personal options or email [email protected] to request an appointment.

Live Well, Leave a Legacy!

David T. Phillips, CEO

Estate Planning Specialists