|

| By Nilus Mattive |

About a year ago, I told my Safe Money readers to use a special backdoor way to invest in Berkshire Hathaway (BRKB).

It is a unique vehicle that gave us access to the shares at a massive discount to their current value.

But I recently recommended they exit that position with a small profit.

You might think it’s because Berkshire — and the proxy we used — have failed to deliver bigger gains over the last year.

That’s not the reason at all. It’s actually something a lot more disturbing.

And it’s something our Weiss Ratings system — which is still assigning the shares a “B-” rating — simply can’t pick up on just yet.

See, for my entire career, Warren Buffett has served as a north star — an ever-present reminder to avoid reckless speculation in favor of investments trading at discounts to their true, readily-understood values.

As the Dot-Com Bubble inflated, he famously stayed on the sidelines …

When the Financial Crisis ensued, he was ready with a sizeable war chest pouncing on deals …

And right up until his retirement from Berkshire Hathaway at the end of last year, he was building his biggest cash position to date.

That should come as no surprise.

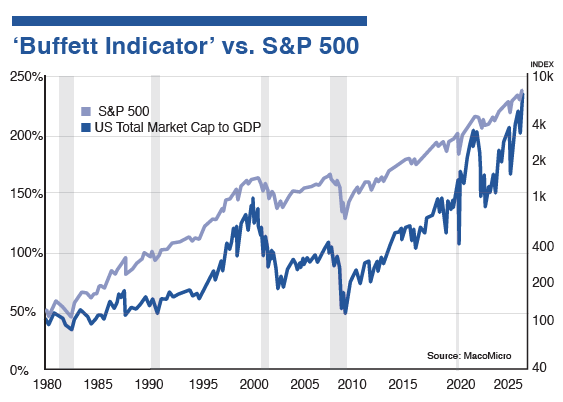

Indeed, as I’ve shown you plenty of times before, his own preferred gauge of stock valuations — dividing a broad index by U.S. gross domestic product (GDP) — currently indicates the priciest market in history.

So, it only makes sense that Buffett was very cautious again … ostensibly building up for the next big crash and a plethora of bargain-basement opportunities.

Meanwhile, Berkshire has also been largely invested in old line companies — the type of stocks getting left out in the cold as a handful of AI-related names drive the majority of the market’s recent gains.

Just to drive home what I’m talking about, here’s a piece of research from our ratings department.

It shows the performance of each S&P 500 sector from April 17 through May 29:

As you can see, tech companies accounted for almost all the gains while some of the most defensive sectors actually lost ground.

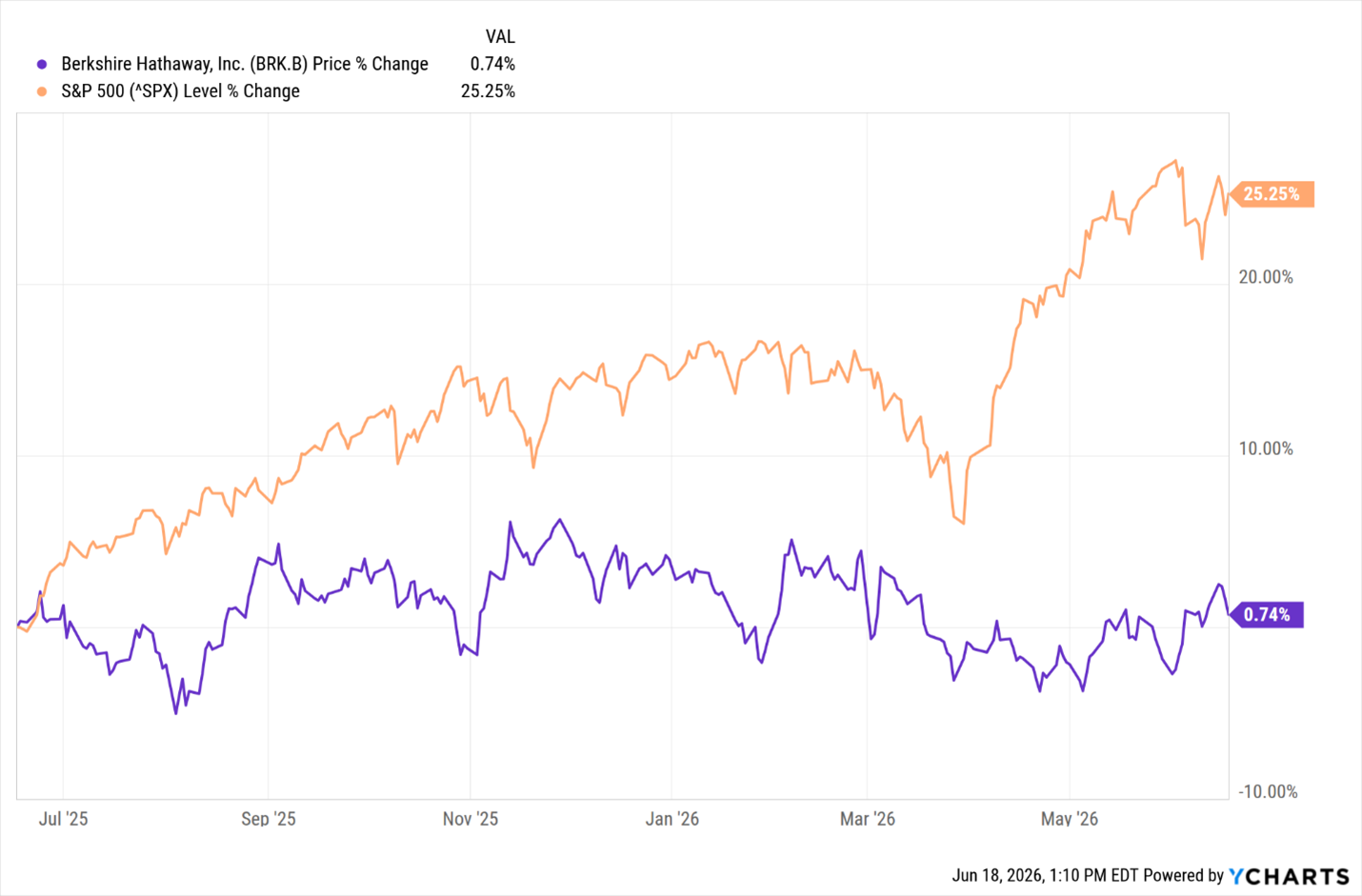

So between its big cash pile and its focus on less exciting businesses, it’s no surprise that Berkshire has underperformed over the last year.

As you can see, from the middle of June last year through the middle of June this year, the stock gained just 0.74% versus a 25.3% rise for the S&P 500.

Like I said, this is NOT what bothers me.

We saw the same type of underperformance from Berkshire during the height of the Dot-Com Bubble, too.

What concerns me is that Greg Abel, Buffett’s successor, just did a deal to buy $10 billion worth of Alphabet (GOOGL) in a private placement offering.

The company began investing in the firm late last year. And after this investment, the stock is now one of Berkshire’s largest holdings.

To be fair, Abel also just did another deal to buy Taylor Morrison Homes (TMHC) for $6.8 billion.

That acquisition looks a lot more Buffett-like since it fits with other homebuilders in Berkshire’s portfolio.

But plowing into an AI-related stock at this point in the market cycle is not in keeping with Berkshire’s history at all.

Google at 28x trailing twelve-month earnings is hardly the type of bargain Buffett would buy.

Abel also initiated a position in Delta Airlines (DAL), a company that operates in an industry that has burned Berkshire before.

Heck, Buffett once said …

"The worst sort of business is one that grows rapidly, requires significant capital to engender the growth and then earns little or no money. Think airlines."

Another time, he put it this way:

"The best way to become a millionaire is to be a billionaire and invest in an airline."

If anything, Berkshire should either remain patient with its cash pile or only look to investing in the same types of quality businesses outside the tech sector it has always found success with.

So I’m worried that Abel, eager to imprint his own stamp on the company, is starting to deviate from the wisdom that made Berkshire work so well for decades.

Hey, maybe he’s right and Google still represents a great value at current levels.

Maybe Delta is a bargain, too.

But two out of three non-Buffett-like deals are enough to give me pause.

So I’d rather move to the sidelines and watch Abel’s next few moves before telling anyone this is the same old Berkshire I’ve always known and loved.

And frankly, even if Berkshire’s core principles remain intact, it’s highly likely there will be a better entry point between now and the time it’s using its still-sizable cash pile in the wake of yet another big market panic.

That doesn’t mean you have to sit on the sidelines yourself. I am actively telling my readers where to put their cash to protect against what’s coming and find profits in the meantime.

Best wishes,

Nilus Mattive