|

| By Sean Brodrick |

China just tightened a hidden chokepoint in a vital global market.

But I’m not here to complain about China. This is another unintended consequence of the war with Iran.

China announced that starting next month, it will halt exports of sulfuric acid — a key input for global copper production.

The motivation behind the move ties directly back to the Strait of Hormuz. Sulfur is produced as a byproduct of oil and gas production.

The Persian Gulf states ship sulfur to China, where it is turned into sulfuric acid for all sorts of industrial uses — including copper mining.

With supply through the Strait blocked, China wants to conserve sulfuric acid for domestic fertilizer and industrial use during the planting season.

Meanwhile, miners around the world use Chinese sulfuric acid in the leaching process to extract copper from oxide and lower-grade ore.

Global Stress Zones

Nervous traders are watching three countries: Chile, the Democratic Republic of Congo and Zambia.

Chile is the world's largest copper producer. A fifth of its production relies directly on acid-intensive leaching.

The DRC and Zambia are even more dependent — 60% of their copper output relies on sulfuric acid leaching.

And 90% of the elemental sulfur that the DRC and Zambia use comes from the Middle East.

When combining these regions with other acid-starved hubs such as Indonesia and Morocco, 15% to 20% of the global primary copper supply is currently vulnerable to this chemical bottleneck.

And already, copper prices are heading higher, after bottoming in mid-March.

How this affects you: Copper is used in just about every industry. This lights a bonfire under inflation.

And this is only the latest force lining up to push copper prices higher.

Copper supply has been under pressure for years.

Ore grades are declining across major deposits, forcing miners to move more material just to maintain output.

At the same time, the pipeline of new projects is nearly dry.

Large-scale copper projects can take more than a decade to move from discovery to production.

Many of the remaining undeveloped deposits are more complex, more expensive or located in areas miners would prefer to avoid for political reasons.

Disruptions are increasing.

Recent years have brought a series of high‑impact disruptions:

- Geotechnical issues at large open pits,

- Water and power constraints in arid regions,

- Protest‑driven shutdowns in Peru,

- The closure of Cobre Panamá after a political backlash and

- Intermittent problems at big names like Grasberg and key Chilean mines.

Demand from electrification and AI.

Electrification (EVs, charging networks, renewables, grid upgrades) is structurally copper‑intensive and expected to drive a multi‑decade increase in demand.

Meanwhile, new demand is surging from AI data centers, cloud infrastructure and energy infrastructure buildouts.

The Perfect Storm for Copper Prices

How far prices will go up depends on who you ask.

Senior analysts at CRU are targeting the $20,000 to $30,000 per tonne range.

As of April 10, copper was ranging from $12,600 and $12,900 a tonne.

Bank of America may be dragging its feet because analysts report that $15,000 per tonne is becoming the new “base case” for the second half of this year.

To be sure, a lot depends on how soon the Strait of Hormuz reopens. But even if it opens tomorrow, there are already huge disruptions working their way through the global supply chain.

And it may stay closed for a while. Within my lifetime, the Suez Crisis closed the Suez Canal for seven long years.

I’m not saying that will happen this time. I’m saying the market is still pricing for a quick resolution to the crisis.

How You Can Play It

If you’d rather bet on higher for longer prices, you could buy the United States Copper Index Fund (CPER).

It uses a rolling position in COMEX copper futures — currently spread across near-term contracts like May, July and September 2026 — backed by cash and short-term Treasurys.

The result is a cleaner play on the metal itself, though it comes with a 1.06% expense ratio.

A better way might be the Global X Copper Miners ETF (COPX).

It holds a global basket of miners, including Freeport-McMoRan, BHP, Southern Copper and Zijin.

Since miners are leveraged to the metal, this can amplify gains. It has an expense ratio of 0.65%.

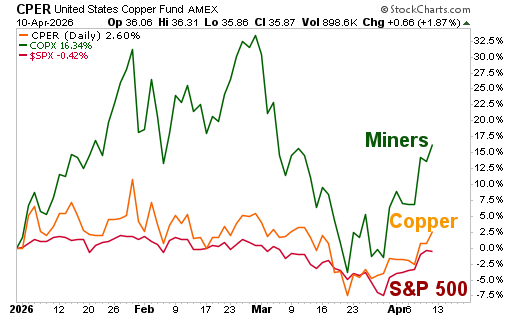

Here’s a performance chart showing how COPX and CPER have performed since the start of the year.

You can see miners are more volatile.

Both are outperforming the S&P 500.

I believe the most bullish days for copper are yet to come. And you’d be wise to hop on board as the metal hits the pedal!

One More Thing!

Because a significant portion of the world's silver comes as a byproduct of copper mining, an “acid-starved” copper market will create a secondary supply shock for silver.

Copper isn’t the only metal that will power higher.

As the world goes Strait to Hell in a handbasket, keep your eye on precious metals, too!

In fact, I already have selected seven metal miners in the best position for this bull rally.

You can come hear all about them on Tuesday, April 21, at 2 p.m. Eastern. Here’s your ticket.

All the best,

Sean