|

| By Sean Brodrick |

America and Iran seem to be stumbling toward a peace deal.

If we’re lucky, and the peace holds, one of the next big steps is rebuilding the wrecked energy infrastructure across the Middle East.

Let’s talk about one thing that isn’t coming back quickly — and an American industry that will benefit.

I’m talking about natural gas and the smoking craters where nat-gas facilities used to be in the Persian Gulf.

Iran and Qatar both took massive amounts of damage in the war, and the United Arab Emirates got hit hard, too.

Iran lost about 50% of its hydrocarbon production. Natural gas is up to 70% of Iran’s oil-and-gas mix.

Its huge South Pars gas field — which it shares with Qatar — was taken offline.

It should take about six to 12 months for Iran to return to its prewar production.

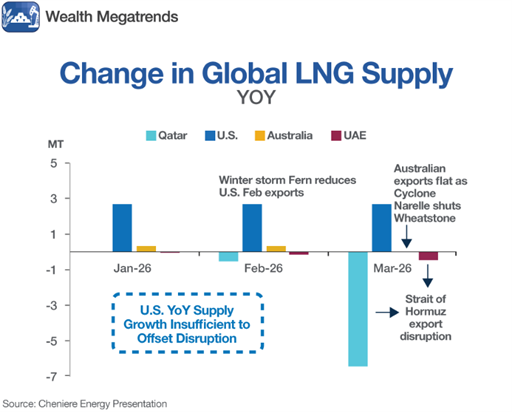

Meanwhile, Qatar’s Ras Laffan complex took the single largest hit, damaging two liquefied natural gas (LNG) trains — a “train” is a set of compressors and equipment that cools natural gas down to LNG — and triggering major fires.

Much of Qatar’s natural gas infrastructure will be repaired in a matter of months. But the damaged facilities at Ras Laffan will take three to five years to repair, keeping 17% of Qatar’s LNG export capacity offline.

That’s about 12.8 million tonnes per annum (mtpa).

In the United Arab Emirates, the Habshan gas processing facility — the biggest on the planet — was hit by Iranian missiles.

About 60% of that was repaired through rapid, even heroic engineering.

Another 20% should come back online by the end of the year.

But Habshan won’t come totally back online until sometime next year.

These disasters are upending global natural gas supply.

Importantly, the world was preparing for a wave of new LNG supply led by Qatar’s North Field Expansion.

Now, it will take Qatar years just to get back to where it was.

At the same time, global demand for liquefied natural gas is projected to surge by 200 mtpa by 2030.

That’s a 25% increase from current global demand.

Who is going to fill the gap?

America’s Soaring Nat-Gas Exports!

U.S. LNG export capacity is already ramping up, with a compound annual growth rate (CAGR) of 10.6% through 2030.

As a result, U.S. LNG export capacity should nearly double from mid‑2020s levels by 2030.

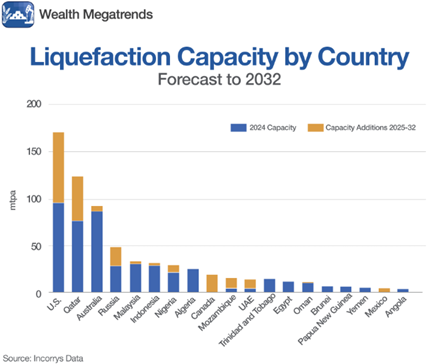

As you can see, most of the world’s new natural gas liquefaction capacity through 2032 is coming from the United States.

Beyond that, LNG export capacity should slow.

That’s okay. That’s years away. And even then, growth should continue.

Through 2030: The Big Build-Out

- The U.S. exported around 11.9 billion cubic feet per day (Bcf/d) of LNG in 2024 and about 14.6 Bcf/d in 2025, setting new records as Gulf Coast terminals ran hard.

- Multiple analyses project U.S. LNG export capacity in the low‑ to mid‑20s Bcf/d range by 2030, effectively a near‑doubling from 2024 levels.

- U.S. LNG export capacity was about 15.4 Bcf/d at the start of 2024. The U.S. Energy Information Administration says U.S. LNG exporters have announced plans to add an estimated 13.9 Bcf/d of liquefaction capacity between 2025 and 2029. So, an increase of 90%.

Meanwhile, demand for U.S. natural gas is projected to increase by about 25% by 2030 compared with 2024, with nearly 60% of that growth coming from LNG exports.

Demand Will Push Up Prices

Foreign demand for U.S. LNG is expected to rise about 15% this year on top of a 15% rise last year, according to the EIA.

In fact …

- Exports to Europe are hitting new records, though Latin America and Asia are also big customers.

- Europe’s structural loss of Russian pipeline gas, Asian urbanization and power demand from AI/data centers all underpin sustained LNG demand into the 2030s.

- The EIA forecasts Henry Hub prices will climb about 65% by 2050, not including inflation. LNG exports are forecast to grow until 2040.

- Around 62 Bcf/d of new pipeline capacity is projected to enter service between 2026 and 2030 to feed LNG plants and exports.

In other words, through 2030, the outlook is for strong exports, fueled by higher prices.

So, 2026 to 2030 is the high-growth window … and exactly when we want to be investing in this industry.

I gave my top pick to play this opportunity to my Wealth Megatrends subscribers last week.

But there’s more than one way to play it.

Another idea is the Alerian MLP ETF (AMLP).

It is the heavyweight benchmark for the midstream energy sector, tracking the Alerian MLP Infrastructure Index to provide exposure to energy Master Limited Partnerships.

And looking at a weekly chart, you can see AMLP is near the bottom of its recent range … and ready for a bounce.

The fund completely bypasses direct commodity price exposure by investing in the "tollbooth" infrastructure assets — such as pipelines, storage hubs and fractionation units — that transport raw fuel from inland shale plays down to Gulf Coast liquefied natural gas terminals.

Its holdings include midstream powerhouses like MPLX (MPLX), Energy Transfer (ET) and Enterprise Products Partners (EPD).

The ETF carries a net expense ratio of 1.01% and has a blockbuster dividend yield of 7.93%.

I believe AMLP will break out eventually. And holders will be paid a nice dividend to wait.

The Persian Gulf nations are picking up the pieces after the war.

Bringing nat-gas production and exports back online will take months, and in some cases, years.

This is an opportunity for America’s natural-gas industry. And smart investors will make the most of it.

All the best,

Sean Brodrick