|

| By Gavin Magor |

The Fed is trapped. And the consequences could be dire for anyone who still holds Wall Street’s favorite stocks.

Yes, I’m going to talk about the Mag 7. But not the ones you’re used to.

In a moment, I’ll tell you how to be the first to hear about the next Magnificent 7 stocks you’ll want to own.

Not even one is a tech stock.

That’s because this next generation of must-own companies operates in another vital space.

Before I get into those details, let me show you why the Fed is stuck …

And why it’s setting off a changing of the guard in the market.

The Strait Truth

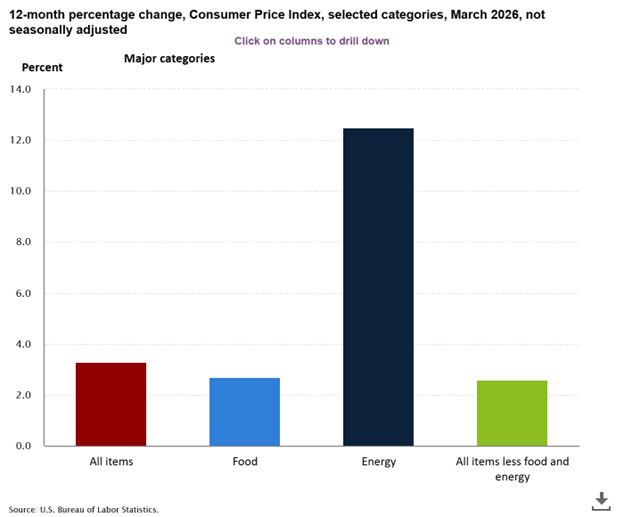

Yesterday oil jumped above $100 a barrel on the ongoing situation in the Strait of Hormuz.

That is driving up prices for everything else. Not just gas.

Higher energy prices trickle into nearly everything we consume — from food (via higher fertilizer costs) and consumer goods (through transportation costs) to staples like cleaning products (because of chemical input costs).

The result: higher overall inflation — no matter what metric you prefer.

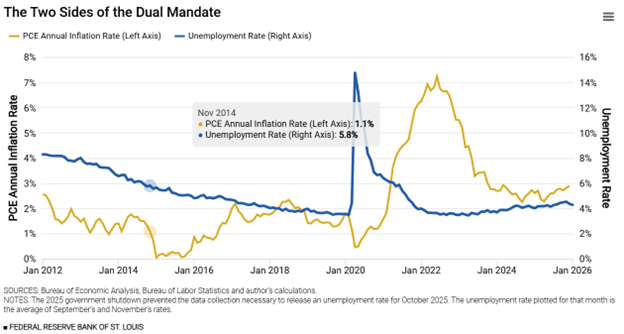

At the same time, the economy has slowed.

While March job numbers were better than expected, February’s large loss of 92,000 jobs was revised to show an actual decrease of 133,000 jobs.

That’s not the overall direction any of us wants to see … especially Fed members.

You see, their dual mandate means that the main tool at their disposal can’t help them.

- If they raise interest rates to combat higher inflation, it could worsen the economic picture.

- If they cut rates, it could send inflation back to 2022 numbers.

- And if they do nothing, both problems could worsen, or at the very least leave us where we are today.

This problem has a corresponding effect on just about everything — housing, debt, savings and spending.

This last is a problem.

Not just for us as consumers, but also as shareholders.

That’s a big reason why the original Mag 7 are becoming less beloved as investments.

They aren’t just raking in the cash … they’re spending their fortunes on AI infrastructure. To the tune of $1 trillion by 2030.

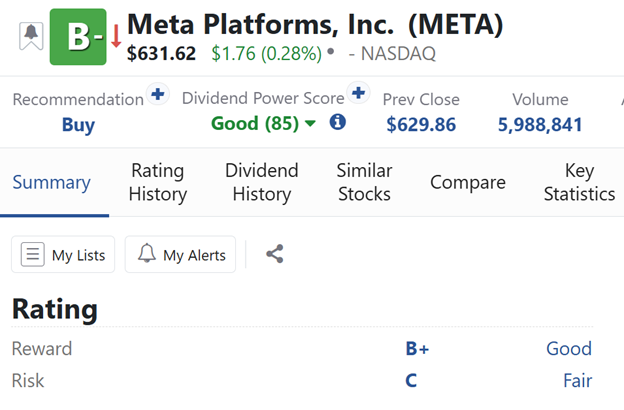

Those investments should pay off in time. We’ve already started to see that with Meta Platforms (META).

But we believe there’s more research and development ahead of it than behind.

For now, Meta and its “magnificent” brethren are taking a backseat to the more immediate beneficiaries of the AI revolution.

Who will be the next big winners?

Commodity producers.

- Oil and gas drillers are obvious, as higher energy prices increase their margins instantly.

- You should also look toward some potentially magnificent miners — gold, silver, copper and other critical mineral producers.

After all, inflation eats away at dollars, but not physical metal.

Inflation only makes those more valuable.

And even if the economy suffers, the AI buildout won’t go away.

Remember, the previous Mag 7 are committed to AI spending.

So, we should buy what they’re buying.

That’s the metals they use for their chips, data centers and fiber cables.

That’s why my colleague, Sean Brodrick, is set to present what he’s calling the “Mag 7 Miners” on Tuesday, April 21, at 2 p.m. Eastern.

Each miner is a small, unknown company that’s only starting to get the attention of investors.

Grab your spot for the event here.

Sean’s findings got my wheels turning.

After all, many of the companies we give “Buy” ratings tend to be larger.

That’s because the Weiss Ratings lean into safety.

So, often you’ll see a Risk Grade of “B” or higher for our “Buy”-rated stocks.

But there’s another way to look for investment ideas that can pop even higher, if you assume a little more risk: our Reward Grades.

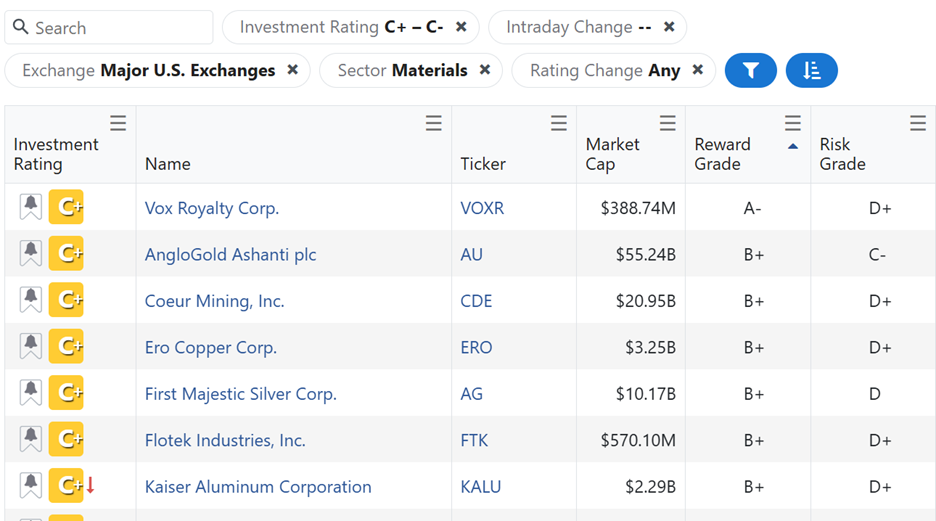

So, I filtered for mining and material companies that fall into our “Hold” category by their Reward Grade.

Several popped up. But I want to look at the top name — Vox Royalty (VOXR).

- It carries a low Risk Grade of “D+.”

- But it also has the only “A-” Reward Grade on the list.

- More importantly, look at its size. It carries a market cap of just $389 million.

A deeper dive shows something even more important.

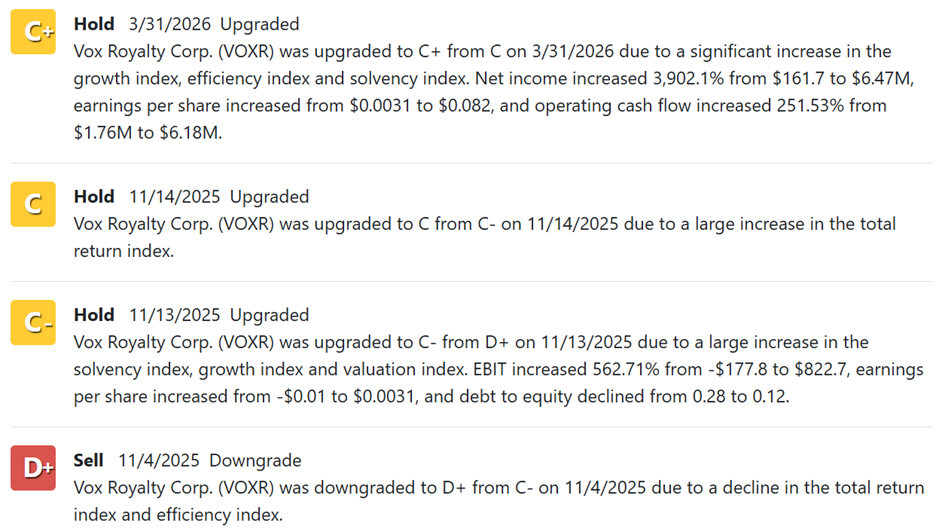

VOXR’s Weiss Stock rating has quietly been climbing for months:

At “C+,” it is only a small upgrade away from “Buy” territory.

As current events continue to favor companies like VOXR, that could happen any day now.

So, let’s look at why VOXR is starting to rise in our proprietary ratings.

Vox Royalty, as the name suggests, is a royalty company.

Meaning, it doesn’t mine any metals itself. Instead, it finances other miners in exchange for royalties when production begins.

Business is good. It has massive, growing royalty interests.

It’s diversified, but geopolitically protected.

And it’s still a very tiny company without the actual costs of mining.

As you can see from its upgrades, net income recently turned positive — a major milestone on the way to a Weiss “Buy” rating.

It also saw growth across the board and an improvement to its balance sheet.

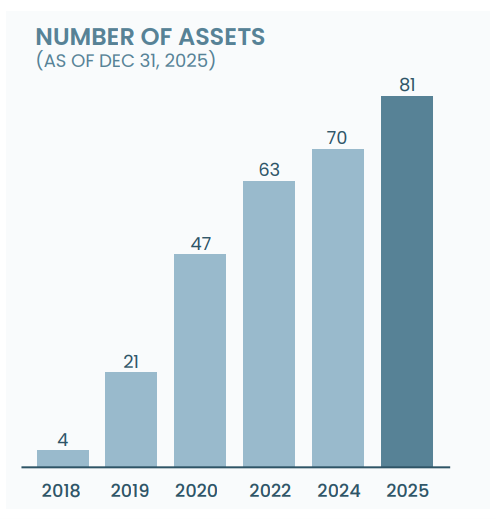

Through its royalties — the number of which has exploded over the past few years — it is leveraged to gold, silver, copper, iron and other metals.

That’s why it carries a high-risk/high-reward proposition for investors.

If these metals continue to climb, investors will be rewarded. If they slump, that’s the risk.

Finally, VOXR got another recent boost. It was just officially added to the VanEck Junior Gold Miners ETF (GDXJ).

As always, I recommend you do your due diligence if you want to buy this or any stock.

And the perfect place to start doing your research is at Sean’s special event next week.

Though, I’ll warn you: Vox Royalty is not one of his seven.

But at least one other might just be on the screen above.

The only way to find out is to reserve your front-row seat to Sean’s Tuesday afternoon event.

You can do that right here now.

Cheers!

Gavin