|

| By Marija Matic |

I recently let you in on one of the key factors to determine altcoin strength in this coming cycle: real revenue.

Gone are the days of memecoin dominance. With Wall Street on the blockchain and adding cryptocurrencies to their balance sheets, they want stability. They want projects with real utility that can monetize and earn profits from their ecosystem.

But revenue alone isn’t enough. Because not all revenue is reflected in a project’s token price.

Which is why investors should run every potential investment through the same two questions:

- Does the money actually reach the token?

- And how much of that money is real demand versus the protocol paying for its own activity?

I gave you examples of three cryptos that top DeFiLlama’s revenue ranking last week, each their own way of capturing revenue and giving token holders their share.

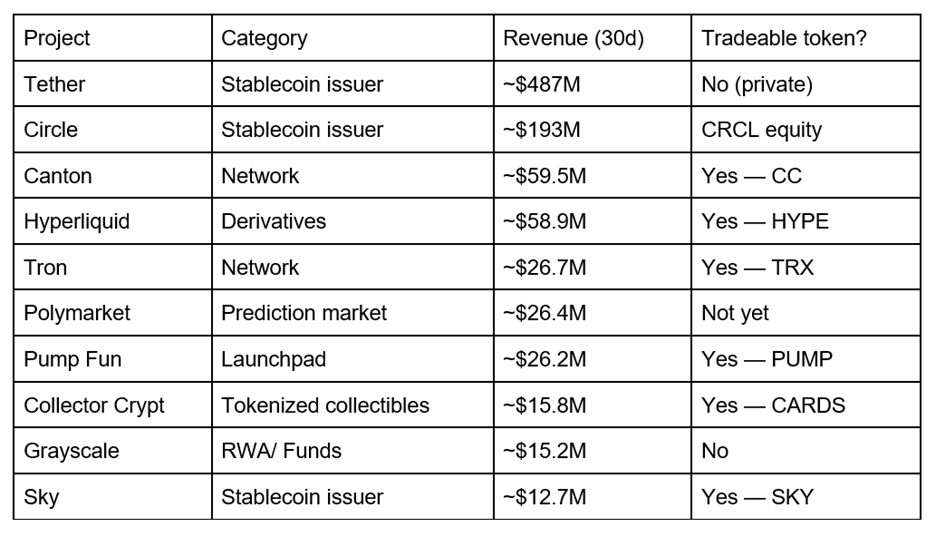

Today, I have three more examples for you, also among the top 10 of DeFiLlama’s revenue ranking.

These are more speculative, and reveal how revenue capture is still imperfect and what red flags you should watch for.

Pump: The Cautionary Tale of the Bunch

Pump.fun (PUMP, “D+”), the Solana memecoin launchpad, earned about $26.2 million in 30 days and has cumulatively cleared over $1 billion in protocol revenue.

On paper, that should make PUMP a revenue-narrative darling.

But in practice, it is the clearest warning on this list of how revenue alone doesn't save a token.

PUMP's nine-month price history is brutal: It listed in July 2025 then rode the tail end of the last big memecoin wave to an all-time high near $0.0088 in September 2025.

That rally was speculative momentum during peak meme-season froth, not a fundamentals story.

How can I tell? Because PUMP has been grinding down ever since.

It printed a fresh all-time low on June 25, 2026, sitting roughly 76% below that September peak.

The damning part: Pump.fun has spent on the order of $350 million-plus buying back its own token. That’s nearly all its daily revenue, and it has barely dented the chart.

A major token unlock around July 12-14 — which will release a large tranche of insider-held supply — acts as the latest overhang. And the platform's new "GO" bounty feature, launched in June, drew real reputational damage, including New York's governor branding it a "dystopian model" amid reports of bounties for risky stunts.

So PUMP is a degen play, full stop.

The revenue is genuine and the buyback is aggressive. But the combination of a momentum-based core business (memecoin launches), some insider supply still to unlock and headline risk has overwhelmed the cash flow.

Here’s the TL;DR …

PUMP belongs on this list because it earns money.

But it also belongs in the high-risk bucket because earning money hasn't been enough to translate into higher token prices.

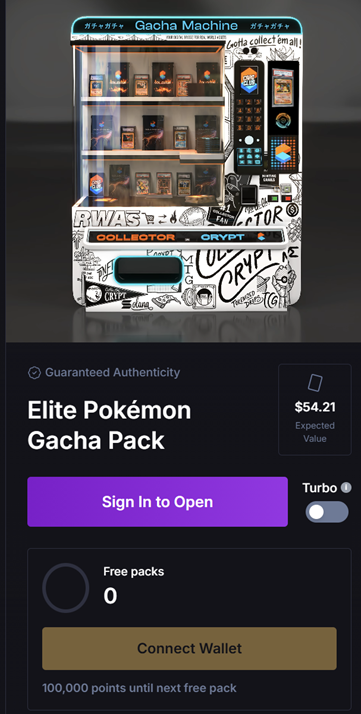

Collector Crypt: The Surprise, and It's (Mostly) Real

Probably the most unexpected name on this list today is Collector Crypt (CARDS, Not Yet Rated), whichearned about $15.8 million over 30 days by tokenizing physical trading cards.

And to answer the first question directly, no this is not a memecoin.

Collector Crypt has a real, doxxed team, which includes CEO Tuom Holmberg and CTO Dax Herrera. And it had a seed round dating to early 2023 backed by recognizable names including market maker GSR, real physical infrastructure (a large insured, climate-controlled vault in Montana) and genuine product-market fit.

Here's how it works …

You send a professionally graded card — like Pokémon cards or, increasingly, One Piece cards — to an insured vault run by partners like Fanatics Collect (formerly PWCC) or ALT. Then, it gets minted as a 1:1-redeemable non-fungible token (NFT) on the Solana (SOL, “B-”) network.

You can then trade that NFT, sell it back to the platform or burn it to get your physical card shipped to you.

But the vast majority of the platform’s revenue — which has cumulatively crossed $50 million — comes from "Gacha."

This is a Japanese capsule-toy mechanic where users buy randomized digital "packs" at fixed price tiers (from ~$50 up to $1,000), open them for a random card, and can instantly sell unwanted pulls back to the platform at roughly 85%–90% of indexed market value.

That instant buyback caps your downside and, combined with the dopamine of the pull, is what keeps people spending.

It works: Single-day pack-opening volume hitting record highs in June!

The token, CARDS, is tied to the platform via planned systematic buybacks funded by profit. That’s the same revenue-to-token logic as the others.

But this is where the caution lives, and it's worth being blunt about the sustainability of that revenue …

- Collector Crypt is gambling adjacent. Randomized paid packs are drawing regulatory scrutiny of "loot box" mechanics; that's a real overhang.

- Low float, big overhang. Only a small share of supply is currently in circulation. The market cap is currently around $55M against a fully-diluted value near $430M. That indicates dilution is coming.

- A mutable contract. On-chain risk scanners flag that the token contract retains the authority to change fees, mint more tokens, or restrict transfers. That’s a meaningful caveat to trust.

- Concentration. A tiny fraction of users reportedly generates a third of the revenue. In addition, the whole business leans heavily on a single IP (Pokémon), which exposes it to licensing and fad risk.

Verdict: This is a legitimate business with a genuinely novel revenue engine. But it’s wrapped in a speculative, structurally risky token.

Sky: The DeFi Blue Chip with a Deliberately Throttled Link

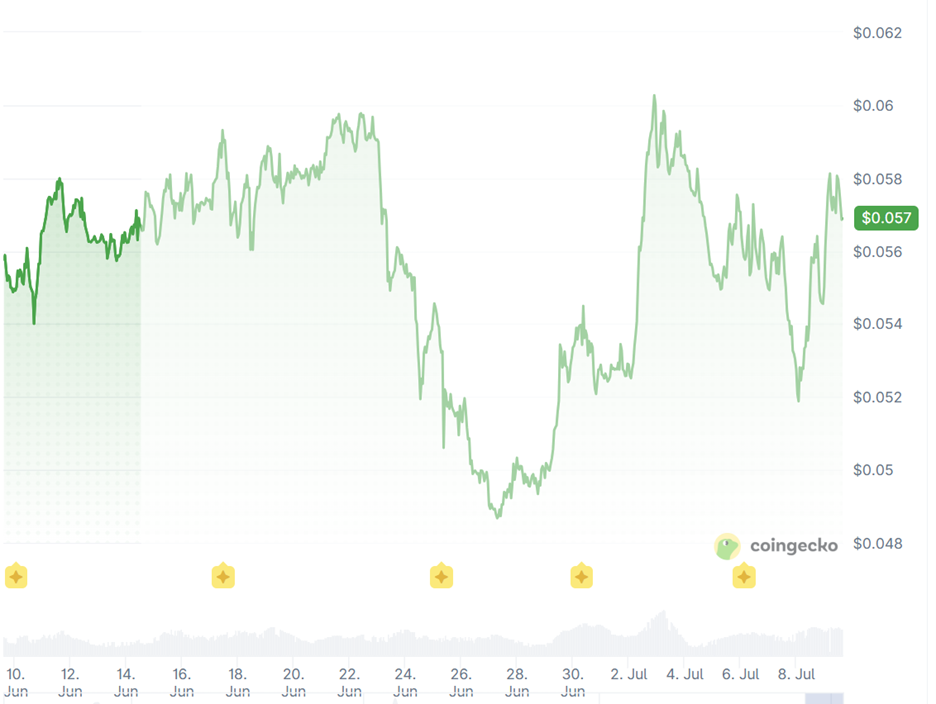

Sky (SKY, “D+”) — the protocol formerly known as MakerDAO — is the most boring name here, in the best sense.

It earned about $12.7 million over 30 days and runs the largest decentralized stablecoin ecosystem for years, with roughly $10 billion of its USDS stablecoin outstanding and billions more in collateral.

Its price action has been the most predictable of the group: SKY trades in a well-worn range around 5 cents and looks to be settling near levels that have historically acted as support.

For a DeFi blue chip with capped supply (around 23.5 billion SKY, fully circulating), that range-bound behavior is the point.

What's driving the revenue is the genuinely interesting part: the Sky Agent Network. It’s run through its Obex incubator, which is backed by a $2.5 billion mandate.

It's a diversified, real-economy revenue base. And it’s exactly why Sky reads as the "adult in the room" of this list, even if its token is engineered for stability rather than fireworks.

Here’s how it works …

Independent capital allocators borrow USDS from the protocol. Then, it can be deployed across yield strategies, including …

- On-chain lending,

- Tokenization,

- AI infrastructure,

- Energy,

- And mortgages.

The yield they generate flows back to Sky protocol as revenue, which in turn helps set the Sky Savings Rate, currently around 3.6%. This program allows savers earn on sUSDS — a product that has paid out more than $250 million to holders since inception.

Like Pump.fun, Sky connects its revenue to its token through a burn mechanism. It’s called the Smart Burn Engine, which uses protocol revenue to buy SKY on the open market and burn it.

In 2025, it destroyed over $100 million of SKY. To date, more than a billion tokens have been repurchased.

On the other side, the protocol emits roughly 600 million SKY per year as rewards to USDS savers, so the net supply effect is a tug-of-war between burns and emissions — with governance steadily cutting emissions to tip it toward deflation.

But there is a deliberate disconnect right now that investors should know about …

In March 2026, Sky governance voted to slash the share of surplus earnings that went into buybacks from 75% down to an interim 7.5%. The difference would be redirected into building a roughly $150 million solvency reserve, with buybacks set to be restored once that reserve fills.

In other words, the revenue-to-token pipe is currently turned down on purpose to prioritize balance-sheet strength over near-term token support.

Think of it like a partial road closure due to construction — a short-term inconvenience is suffered for long-term benefit. That's prudent for a protocol courting institutions.

But it mutes the very flywheel that makes the revenue story exciting in the short term.

Bottom Line

Each altcoin generates revenue and connects it to its token differently. There is no “one size fits all” approach.

And the mechanisms each has — far more than the raw revenue figure — are what separate a fundamental hold … from a fast exit.

Best,

Marija Matić