AI Isn’t Killing Software. It’s Forcing It to Adapt.

|

| By Jurica Dujmovic |

For about four months, owning enterprise software was the loneliest trade on Wall Street.

With the rise of AI agents — bots that can act on your behalf online without human oversight — came the first death knoll for software.

The thesis was simple and brutal …

If AI agents can do all the functions a software subscription can without the user needing to intervene, why pay for a software subscription?

That thesis had real-world impact. The kind that turned every Claude release became a sector-wide event!

Back in late February, for example, Anthropic — the company behind Claude AI — announced that its coding tool could modernize COBOL systems.

That’s the decades-old programming language that still powers the backbone of global finance.

On the news, IBM (IBM) dropped 13% in a single session1 in its worst day since October 2000. That was just one day of its worst month in more than three decades.

When a software giant has its worst day since the Dot Com Bubble, we should pay attention.

Industry experts already did:SaaS names, cybersecurity firms and IT consultants all took their turn in the woodchipper.

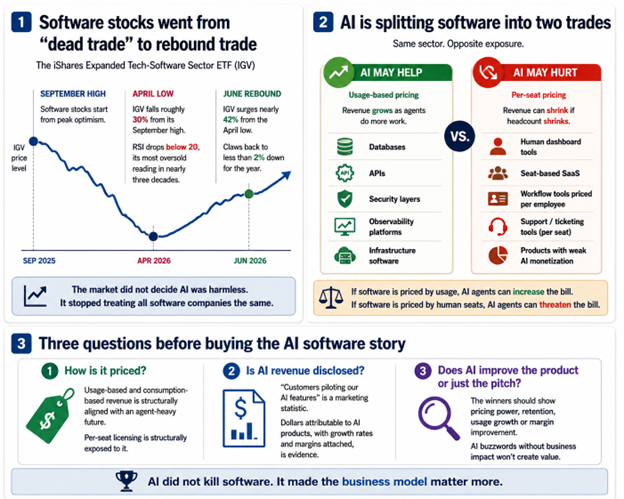

By the time the selling exhausted itself in April, the iShares Expanded Tech-Software Sector ETF (IGV) had fallen roughly 30% from its September high.

The market had effectively priced a chunk of the software industry for managed decline.

Then came the snapback.

An Unexpected Twist

Reuters reported on June 32 that IGV had surged nearly 42% from its April low, clawing its way back to a loss of under 2% for the year.

And over the past month, software ETFs have been outpacing the Nasdaq-1003 as money rotated out of crowded semiconductor trades and back into the names everyone left for dead.

But investors should be clear:I would resist the urge to read this as “software is back.”

This rally isn’t a wholesale pardon for software plays. It’s a verdict on pricing models.

What actually happened were two things.

- The market stopped grading the entire sector based on whether AI replace people,

- And it started to grade individual companies on a much harder metric: If what users get is actually worth how much they pay.

The evidence for that shift is in who is leading …

Investors were flocking specifically to firms that charge based on actual usage … and avoiding those dependent on per-seat subscription fees tied to headcount.

It’s the same thesis I mentioned earlier. Only now, it’s being applied fairly.

If AI agents shrink headcount, then per-seat revenue shrinks with it. So, the software companies that’ll survive are the ones innovating their fee structure.

If software is metered by consumption, then more agents doing more work means a bigger bill.

Same industry, opposite exposure.

Datadog (DDOG) is the cleanest case study.4

Its usage-based pricing means AI workloads feed directly into revenue. And demand from data centers powering AI has pushed the stock to record highs.

Shares nearly doubled this year, including a 31% single-day jump after the company raised annual targets on strong AI-driven demand for security tools.

Palo Alto Networks (PANW) tells a similar story from a different angle: AI multiplies the number of threats and the awareness of them.

As Eaton Vance’s Doug Rogers told Reuters5, the price Palo Alto can charge for defending against those threats should rise with them.

But the loudest voice talking about this sentiment shift is Jensen Huang — Nvidia (NVDA) CEO and software’s most motivated cheerleader.

Since February, he has campaigned against the software-death thesis since February, when he called it “the most illogical thing in the world”6 at a Cisco AI event mid-selloff.

Huang’s logic is genuinely interesting: Agents need tools. Those tools are software, which means demand explodes.

His argument works beautifully for software that agents consume programmatically, things like databases, APIs, security layers, observability platforms.

It is also worth remembering that Nvidia sells the shovels for this particular gold rush. It has every commercial incentive to insist that nobody downstream gets hurt.

That said, the argument does considerably less for software whose main interface is a human being clicking through dashboards …

Which happens to describe a large share of the “software-as-a-service” (SaaS) universe.

The Whipsaw Is the Tell

Look at how violently the market is still repricing individual names. That’s how you can see the sorting play out in real time.

- Salesforce (CRM) gained 9.7% on the Monday of the Huang rally. Then, it gave back 4.2% the very next day as IGV slid 2.8%.

- Oracle (ORCL) has swung from a roughly 30% loss this year to a 25% gain, with Huntington National Bank’s CIO arguing its enormous installed base buys it time to get its pricing model right.

- Microsoft (MSFT) fell as much as 26% before recovering to a 9% loss, tolerated despite its subscription dependence because Copilot and Azure give it credible AI revenue streams.

Notice the pattern in those endorsements: They’re all already big players that have the time to fix their pricing and credible AI products.

Even the bulls are framing their picks in terms of who survives the repricing.

This tells you the disruption thesis was never actually refuted. Just refined.

What I’m Watching from Here

The 42% rally has already happened, so the easy money from the oversold bounce is gone.

From here, the burden of proof shifts to earnings. And I’d apply three filters before believing any software company’s AI story.

1. Follow the pricing model.

Usage-based and consumption-based revenue is structurally aligned with an agent-heavy future.

And the older, per-seat licensing is structurally exposed to it.

When management announces an “agentic” product but keeps charging per human user, the business model is contradicting the press release.

2. Demand disclosed AI revenue, not AI adoption metrics.

“Customers are testing our AI features” is a marketing statistic. You want to see real revenue traced back to AI products, with growth rates and margins attached.

That’s evidence of a strong product and model.

Companies that publish vibes instead of real numbers usually have a reason.

3. Treat volatility as a feature of this market, not a bug.

It’s not quite crypto. But this is an emerging tech narrative, one that’s seen the sector fall 30% on a chatbot release schedule on one side … and rally 42% on a chip CEO’s keynote on the other.

This market will keep overreacting in both directions. In such an environment, you don’t want to chase strength.

Instead, the smart move is to build positions in the genuinely usage-aligned names the next time the next AI scare puts them on sale.

Given how this sector trades, the wait for one won’t be long.

Bottom Line

The SaaS-apocalypse trade was lazy because it treated software as a monolith.

The recovery trade will be lazy too if it does the same thing in reverse.

AI didn’t kill software. But it is forcing the sector to adapt. The investors who will succeed here will be the ones who understand the difference.

Best,

Jurica Dujmovic

P.S. There’s another frontier of cutting-edge tech you should have your eye on: Space.

But if all you know about this sector is Elon Musk’s upcoming SpaceX IPO, you may be missing out.

Startup Investing Specialist Chris Graebe already has one successful space IPO — one that saw the chance for 777% gains — under his belt. Now, he sees another promising private space play. One poised to benefit from SpaceX’s big day, too.

To learn more about it, click here.

1 https://finviz.com/news/321729/ibm-faces-worst-month-since-1992-is-anthropic-the-new-dot-com-moment

4 https://www.cnbc.com/2026/05/07/ai-winners-software-datadog-stock.html

6 https://finance.yahoo.com/news/nvidias-huang-dismisses-fears-ai-065001192.html