|

| By Jurica Dujmovic |

AI has become the load-bearing wall of the U.S. equity market.

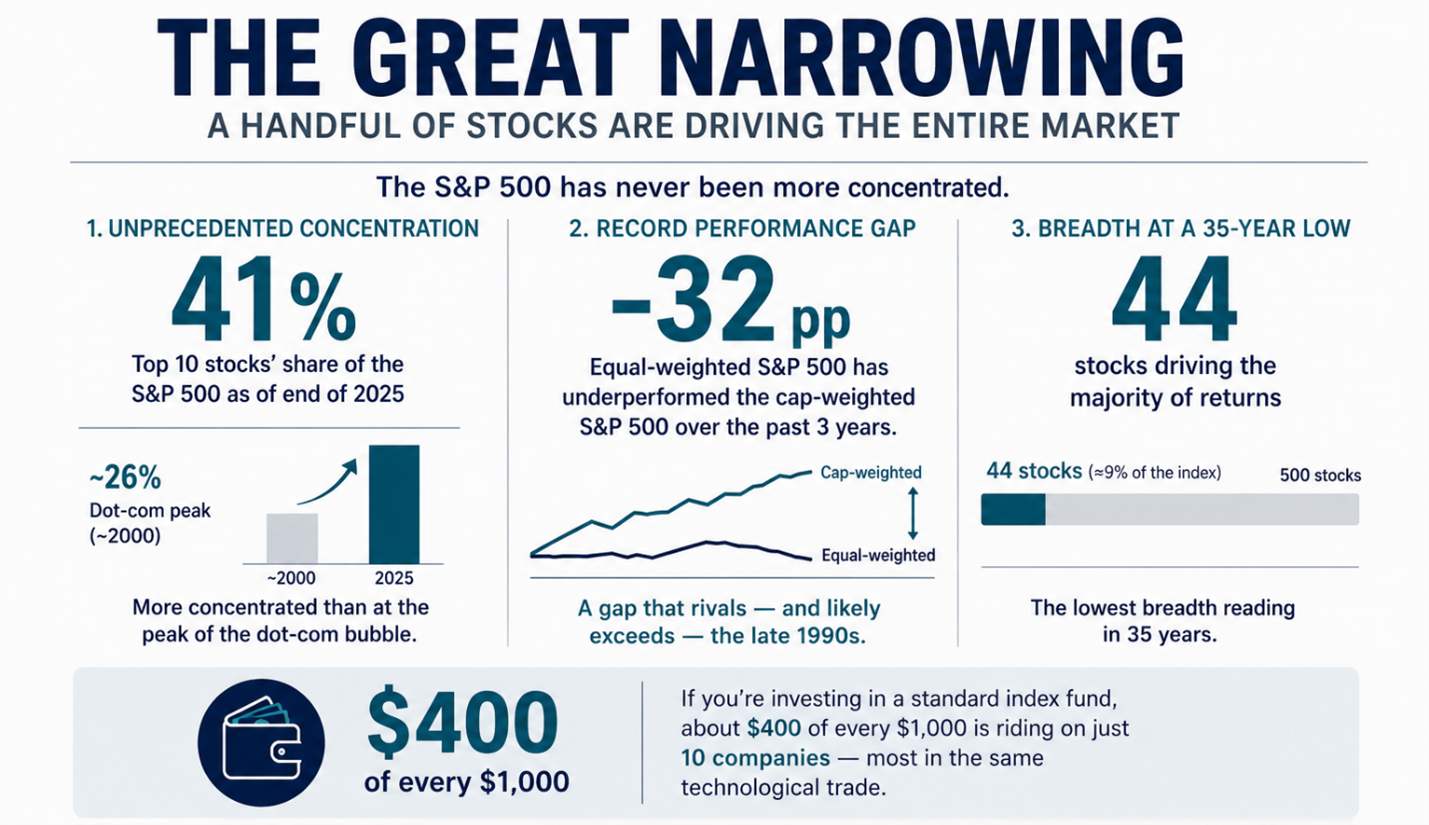

According to State Street Global Advisors1, only about 44 names within the S&P 500 are truly driving returns — the lowest breadth reading in 35 years. Bull market? More like a very expensive relay race with four dozen runners and 450 spectators.

Strip out a handful of AI-linked names and the S&P 500 tells the story.

As of the end of 2025, the ten largest companies in the index accounted for 41% of its total market weight. That’s nearly double their share from a decade ago!

And it’s a level that exceeds even the peak of the dot-com bubble.2 Back in 2000, concentration peaked at 26%. We are well past that now.

The equal-weighted S&P 500 — where every company carries the same influence — has underperformed its market-cap-weighted counterpart by roughly 32 percentage points over the past three years. That gap now exceeds the outperformance seen in the late 1990s.

Let me simplify this: If you are investing in a standard index fund, about $400 of every $1,000 you invest is riding on just ten companies. And most of them are in the same technological trade.

AI Is an Industrial Problem Wearing a Software Label

Obviously, this is a problem for diversification. But it’s one that extends beyond any individual portfolio.

See, load-bearing walls need foundations. But the floor of the AI boom is growing increasingly unstable. And with so much market growth tied into AI, any cracks in the floor could have outsized implications for everyone.

The biggest crack threatening AI stability is energy.

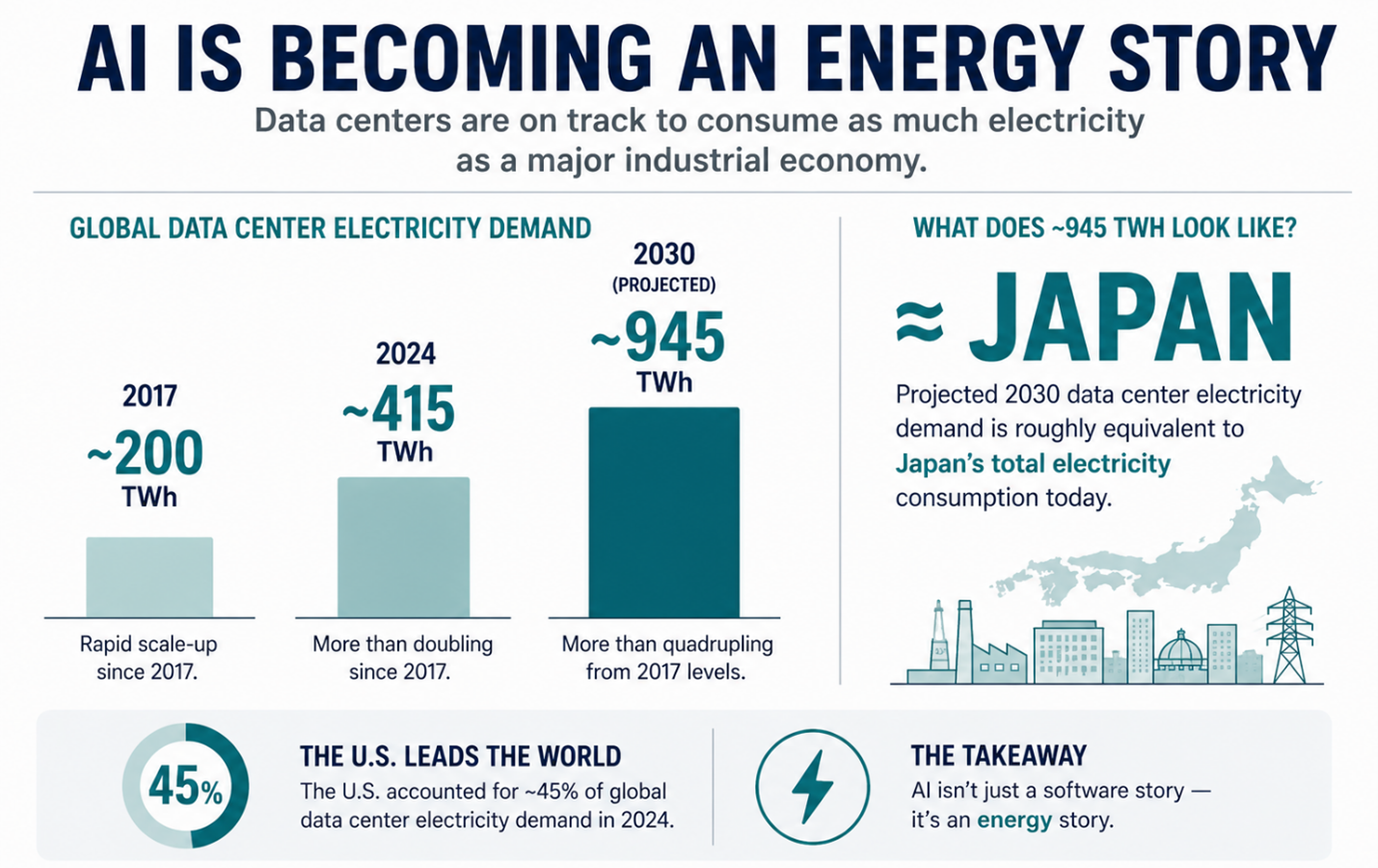

Data centers consumed approximately 415 terawatt-hours3 (TWh) of electricity globally in 2024 — about 1.5% of total world electricity demand. The U.S. alone accounted for 45% of that total.

By 2030, the International Energy Agency projects global data center consumption will roughly double, reaching approximately 945 TWh — comparable to Japan's entire annual electricity consumption today.

In the U.S., the trajectory is steeper.

Lawrence Berkeley National Laboratory4 estimates that data centers could account for 12% of all U.S. electricity by 2028. In Virginia — the nation’s largest data center hub — data centers already account for a significant and rapidly growing share of electricity demand, with projections suggesting they could dominate statewide consumption within the decade.

The question now is whether the existing grid can absorb what is coming. Evidence suggests that, if nothing changes, the answer will likely be “no.”

The Grid Cannot Scale Like a Software Update

Capital can be redirected in hours. Energy infrastructure cannot.

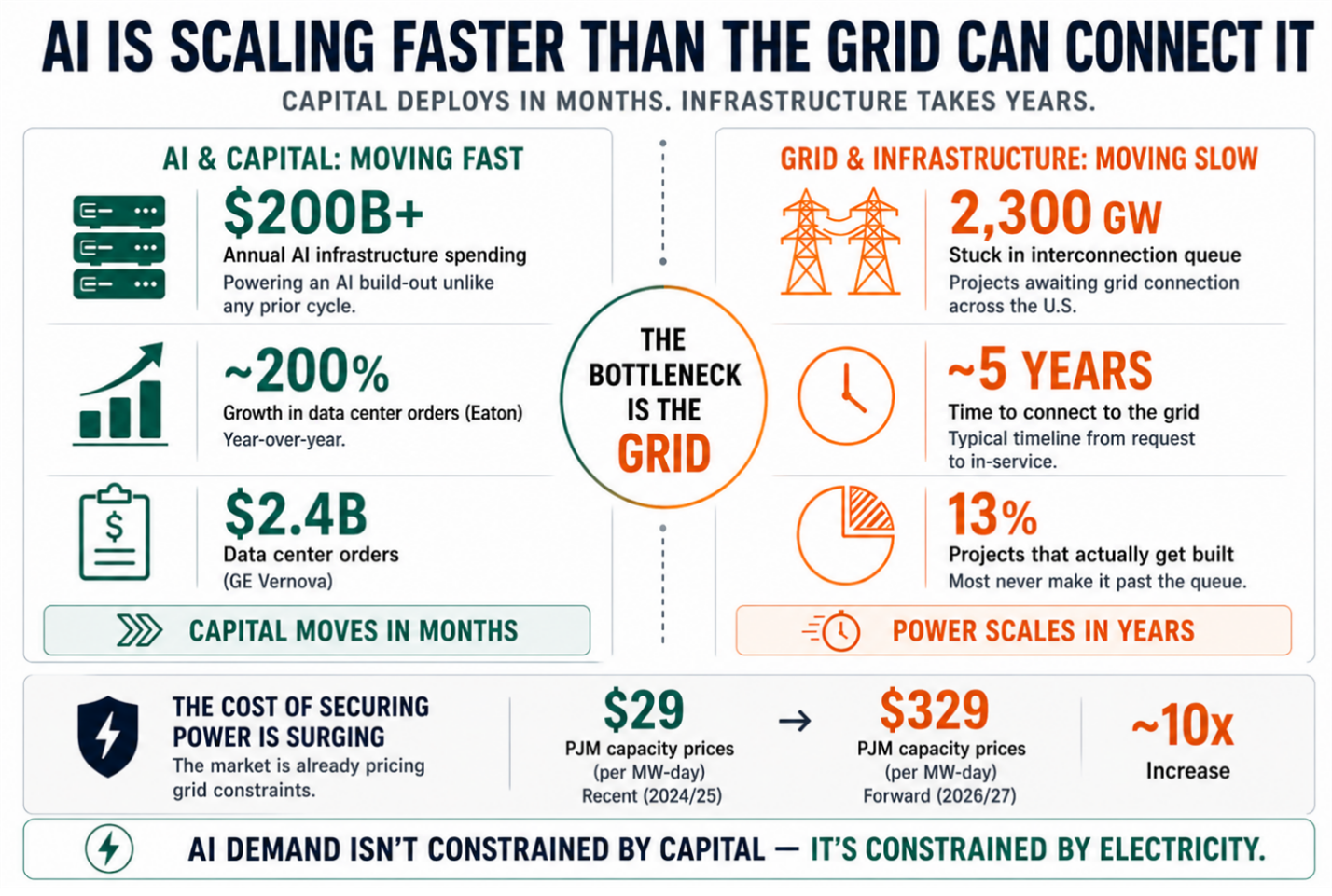

The time it takes to go from an initial interconnection request to commercial grid operation has more than doubled.5 As of late 2024, the active interconnection queue held nearly 2,300 gigawatts of capacity seeking connection — more than the entire installed U.S. power plant fleet.

Of all capacity that entered the queue between 2000 and 2019, only 13% had reached commercial operation by end of 2024.

Texas offers the clearest stress indicator: CenterPoint Energy reported a 700% increase in large-load interconnection requests between late 2023 and late 2024 — growing from 1 GW to 8 GW in a single year.6

Virginia has another 50 GW of data center projects sitting active in the queue, and developers there are seeing seven-year delays for some projects.

The cost signals confirm the squeeze.

Capacity market clearing prices in PJM — the grid operator covering much of the Mid-Atlantic and Midwest — jumped more than tenfold,7 from $28.92/MW-day to $329/MW-day for the 2026—27 delivery year.

That is a clear example of a market pricing in scarcity.

The clearest signal that this constraint is already binding is found in earnings calls. Eaton Corporation's (ETN) CEO described their data center backlog on the Q4 2025 earnings call as equaling "eleven years of what was built in 2025."

Data center orders at Eaton accelerated approximately 200%8 in Q4 2025, with sales up over 40% year-over-year.

It’s not alone, either.

GE Vernova (GEV) booked $2.4 billion in data center-related orders9 in Q1 2026 alone — already surpassing its entire 2025 total. CEO Scott Strazik has stated publicly that the company is at roughly 10% of what he sees as its total addressable market.

These companies are booking real-world contracts, not hype. Multi-year, signed, legally binding contracts for equipment to build the infrastructure that AI runs on.

That order backlog is the market's best real-time signal of how far the gap between AI demand and physical delivery has already opened.

What Happens When the Constraint Bites

Markets tend to price visible inputs — valuations, earnings, rate policy.

But physical infrastructure constraints are different. They do not show up in quarterly reports until project delays and cost overruns are already baked into the timeline.

By then, the market has been extrapolating smooth delivery for years.

When the AI buildout hits power constraints at scale, the effect will not spread evenly. It will concentrate. A data center campus that cannot get grid connection cannot generate revenue. A hyperscaler that has committed tens of billions in CapEx guidance cannot arbitrarily slow the burn or accelerate delivery of electrons that the grid is not yet positioned to supply.

That mismatch between committed capital and physical availability is where the adjustment happens.

Why Investors Care

The investment implication is not to short the AI trade.

The market is not fragile in the immediate sense. The AI narrative is real and the capex backing it is genuine.

But real narratives can still produce concentrated risk when they outrun physical delivery capacity. The stability is conditional on continued alignment between investment pace and infrastructure execution — and that alignment is beginning to show strain.

Instead, investors must recognize where value is flowing as the physical constraint becomes the dominant variable.

When power becomes the bottleneck, the companies that control or can more easily access the infrastructure that delivers them become critical choke points in the AI value chain.

That includes companies that …

- Create and sell the raw energy.

- Build the delivery systems and machines that generate and transport energy.

- Actually build the data centers themselves.

If you live outside the U.S. and want to keep some of these AI plays on-chain, you may want to look over in Ondo Global Markets to see if any stocks that caught your eye have been tokenized just yet.

The Bottom Line

The AI trade has been the most consequential macro force in U.S. equity markets for two years.

The companies at its center are genuinely profitable, the capital behind it is genuine and the demand for AI services is real.

None of that is in dispute.

What is underappreciated is that the delivery system for this trade runs on physical infrastructure that does not respond to capital flows the way financial markets do. And that hasn’t been properly prepared for the surge in demand AI has and will continue to create.

Consider this your early warning. Constraints are coming. But the market likely won’t notice until they are too obvious to ignore.

At that point, it’ll be too late for the average investor to get ahead of the move.

You also don’t want to divest from AI altogether. That’s another surefire way to be left in the dust.

My 2 cents is that the investors best positioned for what comes next will be the ones who recognized early that AI is fundamentally a physical-infrastructure story. The ones who see the demand building now and follow the electrons to where value was actually accumulating …

In the wires, the turbines, the cooling systems and the uranium enrichment facilities that make the digital economy physically possible.

The only question is whether you get there before or after the market catches up.

Best,

Jurica Dujmovic

1https://www.ssga.com/us/en/institutional/insights/mind-on-the-market-17-november-2025

2https://www.rbcwealthmanagement.com/en-us/insights/the-great-narrowing-sp-500-concentration

3https://www.iea.org/reports/energy-and-ai/executive-summary

6https://www.camus.energy/blog/why-does-it-take-so-long-to-connect-a-data-center-to-the-grid

7https://interestingengineering.com/energy/ai-power-grid-data-centers-us

8https://finance.yahoo.com/news/1-4-trillion-needed-ai-132108238.html