CLARITY Will be the Key Variable for Crypto This Spring

|

| By Jurica Dujmovic |

For two years, Washington processed stablecoins as a plumbing problem …

How do you back them?

Who regulates the issuer?

What happens in bankruptcy?

Then, the GENIUS Act was signed into law in July 2025. And it answered many of those questions.

They’re backed by one-to-one reserves. They’re regulated within a federal framework with federal and qualified state oversight. And priority protections were put in place in the event of insolvency.

It’s boring, technical … and incredibly necessary.

But it was only the start. With the framework in place, details need to be hammered out as friction increased between TradFi institutions and crypto heavyweights.

That brings us to the CLARITY Act.

The Pass-Through from GENIUS to CLARITY

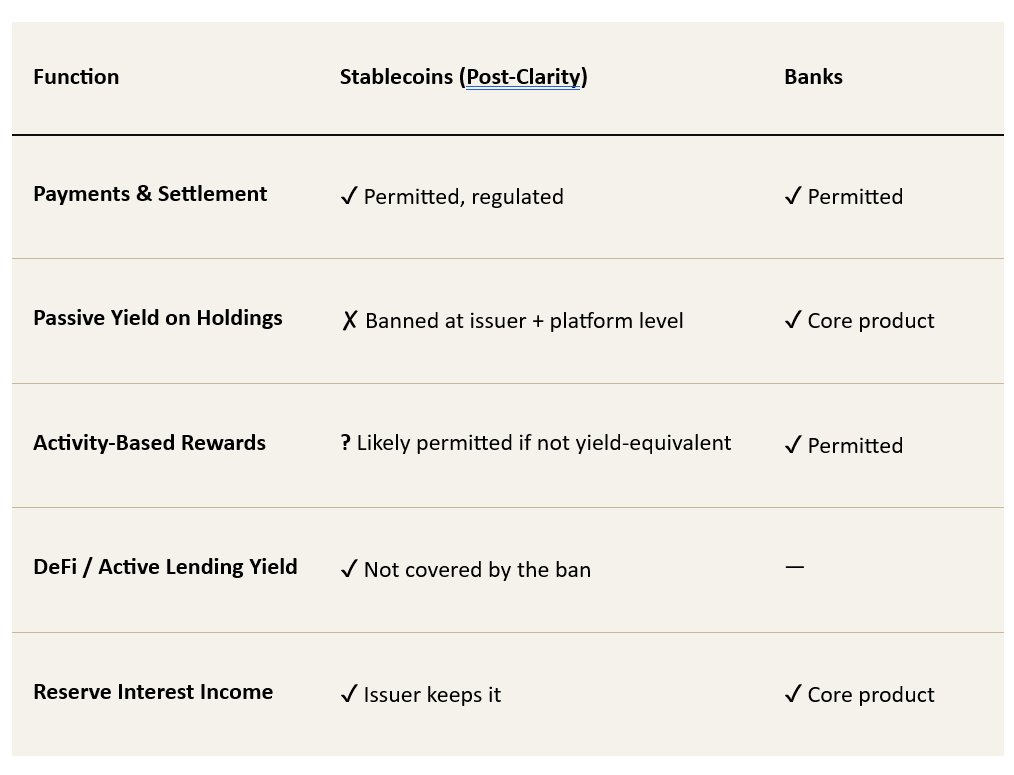

Under the GENIUS Act, stablecoin issuers were told they could not directly pay holders passive yield earned from the Treasury notes in their reserves.

Yield is a huge incentive for holders. So, issuers like Circle (CRCL) and Tether found a workaround.

Nothing in the 2025 law prevented them from sharing that income downstream. Which means issuers could collect the interest on the U.S. Treasurys backing USDC and share a portion of that revenue with Coinbase (COIN).

Coinbase then would offer stablecoin rewards to its users at roughly 3.5%.

The stablecoin holder gets yield. The issuer technically never paid it. And a crypto middleman — what a world — gets their cut.

Banks watched this arrangement and said that the functional outcome was identical to a savings account. And that was a big problem.

They argued that since traditional savings accounts pay a fraction of a percent, depositors will have an obvious reason to move money out of banks.

That would be a deposit flight. And it matters because it constrains lending.

According to the banks, allowing pass-through passive stablecoin yield would “drain deposits from regulated institutions, constricting the credit that fuels communities.”

The CLARITY Act is meant to resolve this conflict. And when the banks were unhappy with the initial draft that left this pass-through in, they drew a line in the sand.

Since late January, crypto and the banks have been fighting over a compromise. On Monday, we got to see the result of over a month of negotiations.

And there’s a clear winner: The banks.

The new Clarity Act draft bans not just the current pass-through system, but anything that regulators can characterize as economically equivalent.

What the Banks’ Win Means

To be clear, the new draft of the Digital Asset Market Clarity Act would ban yield not just at the issuer level, but across the entire stack: Exchanges, brokers, affiliates, any platform that offers rewards "directly or indirectly" for holding a stablecoin, or in any arrangement "economically or functionally equivalent" to interest, would be prohibited.

Rewards tied directly to activity are the only exception.

What the legislation would produce, if passed in its current form, is a legally enforced product segmentation.

Stablecoins become payment rails that benefit banks … and retail users are kept away from the increased income passive stablecoin yield offers.

This isn’t just the establishment fighting against innovation. Nor is it a matter of TradFi rejecting crypto out of hand.

This fight is happening because stablecoins are no longer a speculative instrument. It’s a lucrative sector.

- Total market cap has crossed over $310 billion.

- Annual on-chain transaction volume hit $30T+ in 2025.

- Visa's (V) stablecoin-linked card spend reached a multi-billion-dollar annualized run rate in the fourth quarter of last year.

- Mastercard (MA) agreed to acquire stablecoin infrastructure firm BVNK for up to $1.8 billion.

- PayPal’s global expansion of PYUSD is occurring in parallel with these regulatory constraints.

Stablecoins are here to stay. The fight now is over who gets to benefit the most — issuers and holders, or the banks.

Market Reaction: Tuesday, March 24

The market’s response was swift.

Circle's stock fell 20% on Tuesday. It was a move widely described as the company’s worst single session since going public.

The initial damage looks rough. But this sell-off requires more context to fully understand.

The sell-off requires some context. Circle had rallied more than 110% from late February on strong USDC circulation numbers and investor expectations that regulatory clarity would lock in the company's first-mover advantage.

Tuesday's reaction stripped roughly half that gain, but not all. And analysts at Citi are skeptical it’ll be a long-term reality. They called it an overreaction and suggested investors buy the dip.

They may be right about the short term. The long-term question is different.

Now, Circle's competitive advantage over Tether — the other major centralized stablecoin issuer — is in question. The latter has long resisted offering comparable yield programs. And with Circle’s offerings now banned, the gap between them will narrow.

And will likely continue to.

Tether announced this week that it hired a Big Four accounting firm for a full reserve audit, which would address the one structural credibility gap that has historically kept institutional money with USDC.

The timing was not accidental.

Things get murkier as we move down the pass-through pipeline. Coinbase dropped roughly 10%. That’s because the centralized exchange makes roughly 20% of its revenue from stablecoin-related activity.

If this draft of CLARITY passes, that revenue stream shrinks. Coinbase's USDC rewards become harder to justify as a user acquisition tool.

What Investors Should Watch

I want to make something very clear: The practical floor for stablecoins as an asset class is not yield. It is utility.

A $33 trillion annual transaction volume does not exist because people are chasing 3.5% on Coinbase. It exists because stablecoins are faster, cheaper and more programmable than existing payment infrastructure.

That utility does not disappear if passive yield is banned. The transaction layer survives. Only the savings vehicle is at risk.

For holders, that’s a big deal.

For issuers, it’s a challenge. Now, the question they have to answer is whether their revenue models are durable without the reserve-sharing arrangement that currently funds user acquisition.

To that, Circle says “yes.”

It made the argument this week that it strategically positioned itself as a broader fintech infrastructure provider, not just a stablecoin issuer.

Its Arc blockchain — designed to support global payments and tokenized real-world assets using USDC as the native currency — points in that direction. Though that is a longer and less certain path than the current model.

For platforms like Coinbase, USDC reward programs at current yields are a retention tool. Without them, the platform competes on execution quality and product breadth alone.

That is a winnable position, but a harder one.

Citi's buy call after Tuesday's drop reflects a view that the market overpriced the yield revenue stream in Circle's recent rally and that the underlying exchange business at Coinbase is not impaired by this development.

Those are smart guys. And they’re probably correct … as long as the CLARITY Act draft doesn’t expand into DeFi yield mechanisms.

Bottom Line

For now, all of this is still speculation. The CLARITY Act remains in Senate negotiations.

Though with many in the crypto community adopting a “anything is better than nothing” approach to negotiations, we should see CLARITY progress soon.

Especially since any further delays could be severe. Senator Moreno has warned that if the bill does not advance by May, digital asset legislation may stall for years.

Whether what eventually passes resembles Tuesday's draft will be the key variable heading into spring 2026.

Best,

Jurica Dujmovic