|

| By Mark Gough |

The deadline for U.S. residents to file their taxes is right around the corner.

When it comes to crypto and taxes, things can get confusing. To help you keep track, we’ve previously covered what counts as a taxable event for your digital assets.

But this year, the IRS has a curveball for us.

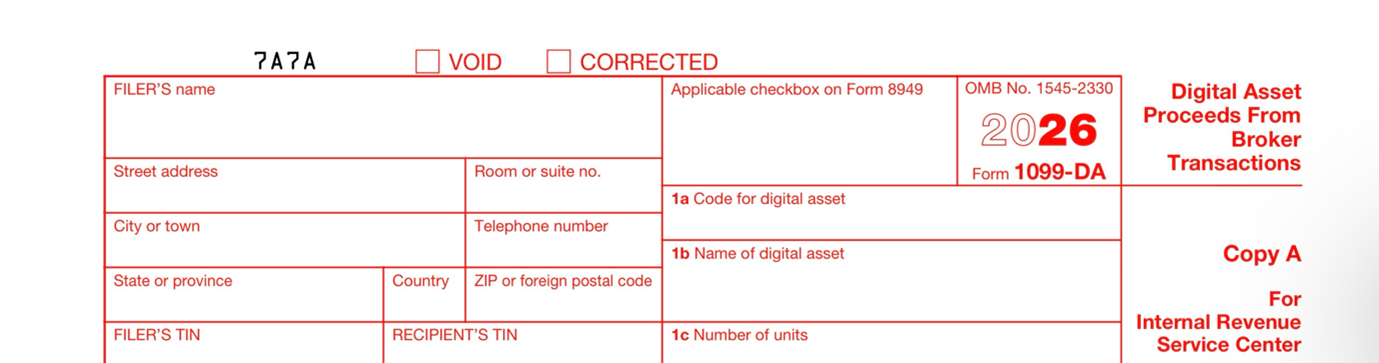

For the first time, many U.S. crypto investors are opening their inbox to find a new form waiting for them: Form 1099-DA.

And that changes how investors need to approach their filings.

What Is Form 1099-DA?

The 1099-DA (“Digital Asset Proceeds from Broker Transactions”) is a new IRS tax form specifically for cryptocurrency and other digital assets.

It debuts for the 2025 tax year, meaning investors are receiving these forms in early 2026 as they prepare their filings.

The purpose is simple: Centralized, regulated crypto exchanges (CEXes) and brokers who trade digital assets must now report certain transaction data directly to the IRS.

This includes:

- Crypto sales

- Token swaps

- NFT transactions

- Stablecoin trades

- And other digital asset dispositions

In practical terms, it works similarly to the 1099-B that stockbrokers have used for decades.

Now, crypto platforms are being required to do the same.

A Big Shift for Crypto

Historically, when it came to your crypto, the IRS had limited direct visibility. Investors were expected to track their own trades, transfers and gains across wallets and exchanges.

In short, it was basically an honor system. The 1099-DA changes that.

Exchanges now report gross proceeds from transactions directly to the IRS. Which means the agency may already have transaction records before you file your return.

Just like it does with your TradFi trades.

If you only use a single CEX, this form is great news. It simplifies a lot of your end-of-year accounting.

But if you use multiple exchanges or DeFi platforms, things can get tricky. That’s because there’s an important nuance in how the 1099-DA works: The form typically reports gross proceeds, not your actual taxable gain or loss.

And this distinction is where things get complicated.

The Key Problem Investors Are Running Into

Crypto activity often spans multiple platforms and wallets.

It’s not uncommon to buy a token on a centralized exchange, move it to your own wallet and deposit it on a DeFi platform for yield.

Or swap it on a decentralized exchange for a token not yet listed on CEXes …

Or store it in a hardware wallet …

Or end up selling it for fiat on a different exchange.

With such a piecemeal system, the data a CEX or broker sees is often incomplete.

For example, let’s say you bought $18,000 worth of crypto on a DEX. Then, you staked it to earn some yield. Assume your rewards equal $2,000.

Then, to cash out, you move your entire $20,000 balance to Coinbase and swap everything for fiat.

In that case, Coinbase may report that you sold $20,000 worth of crypto. But if you originally purchased those tokens for $18,000 somewhere else, your actual taxable gain would only be $2,000.

Without cost basis information, the IRS only sees the $20,000 proceeds … and calculates accordingly.

Which means meticulous recordkeeping for the more active crypto user is still necessary. And it means you can’t just copy the numbers from your 1099-DA into your tax return.

Doing so could create some serious inaccuracies.

Inaccuracies don’t mean you’re in trouble with Uncle Sam. But when flagged, they create a lot of headaches and continued talks with the IRS.

So, a little extra effort now … means you could save yourself a lot of frustration tomorrow.

What Crypto Investors Should Do Next

The best way to think of your 1099-DA is like a SparkNotes guide.

It gives the highlights. It’s up to you to fill in the rest of the story and reconcile the activity around them.

If you received a 1099-DA and know it doesn’t contain the full picture, here’s your game plan to make sure can fill in the rest.

- Gather All Your Transaction Data

Start by collecting records from every platform you used. This includes:

- Centralized exchanges

- DeFi protocols

- Wallet activity

- NFT marketplaces

- Staking platforms

Many exchanges allow you to export a full transaction history. You’ll want those records before attempting any tax calculations.

- Reconstruct Your Cost Basis

To calculate actual gains or losses, you need to determine what you originally paid for each asset.

That means matching purchases, transfers, sales and swaps. And recording any airdrops or yield earnings.

This process can become complex if you’ve moved assets across multiple platforms. That’s why keeping records in real time is the best approach to avoid the April stress.

There is also tax software platforms — like Koinly, CoinLedger and CoinTracker — that can help you automate capital gains calculations and track your DeFi and NFT activity.

- Reconcile the Numbers

Once you’ve rebuilt your transaction history, it’s time to compare your calculations with the totals reported on the 1099-DA.

The goal isn’t to force your return to match the form exactly. Instead, your focus should be on explaining any differences clearly.

If your cost basis reduces the taxable gain significantly, that’s legitimate … as long as it’s properly documented.

Why This Is Just the Beginning

The introduction of the 1099-DA is part of a broader regulatory shift. One that means the era of loosely tracked crypto activity is coming to an end.

Governments around the world are moving toward greater transparency in digital asset markets. Tax reporting expectations are becoming much closer to what traditional investors have dealt with for years.

But this isn’t necessarily a negative development.

Clearer reporting standards can help legitimize the industry and make institutional adoption easier over time.

But for better or worse, it’s a change that isn’t going away any time soon. And with the IRS increasing oversight of digital assets, documentation matters more than ever.

To avoid the yearly panic, you’ll want to keep a record of …

- Exchange statements

- Wallet transaction histories

- Trade confirmations

- Transfer records

Throughout the year. Having a clear paper trail makes resolving discrepancies far easier.

Or, if you prefer a human touch, you may consider reaching out to a crypto-aware accountant to help accurately reconstruct that cost basis.

The Bottom Line

Receiving a 1099-DA doesn’t automatically mean you owe more taxes. It simply means your crypto broker reported transaction data to the IRS.

The critical step is ensuring your tax return accurately reflects the true gains or losses from those transactions.

That can be a tall ask for active investors who rely on multiple exchanges, DeFi protocols or self-custody wallets to enact their strategies. But taking the time to do this properly is essential.

The regulatory environment around digital assets is evolving quickly.

Understanding how these reporting rules work now can save you significant stress and potentially costly mistakes down the road.

Best,

Mark Gough