|

| By Jurica Dujmovic |

The debate over whether crypto can serve as legitimate collateral is over.

BlackRock and Bank of New York Mellon settled it with the tokenized shares of BackRock’s Treasury Trust fund. And recently, even Uncle Sam — via Fannie Mae — accepted the decision, allowing Bitcoin (BTC, “B+”) to be used as collateral for a mortgage downpayment.

Even Moody’s has jumped on board. As of last month, it is now the first credit rating agency to bring independent credit analysis to infrastructure on the blockchain.

Now a more consequential question is taking shape …

Who gets to define what collateral is?

Washington took a swing at answering it last year … and only made things more complicated.

How Collateral Actually Controls the World

Most coverage of monetary policy focuses on interest rates. But the deeper lever central banks pull is collateral.

By determining which assets qualify for repo operations, discount window access and regulatory capital treatment, the Federal Reserve and its peers control the raw material of credit creation.

That matters. Because collateral eligibility is how monetary policy moves through the financial system.

That mechanism has always depended on one assumption: The state holds a monopoly on defining what counts as safe.

U.S. Treasurys anchor global collateral markets because a sovereign entity guarantees them. Investment-grade ratings carry weight because regulators have codified them into capital frameworks.

The entire architecture of modern credit rests on that sovereign backstop.

But crypto is building an architecture that partially integrates with that system … and partially escapes it.

The Scale Is No Longer Theoretical

Over the past two years, on-chain credit infrastructure grew from a niche experiment into a market that demands attention.

Crypto-collateralized lending hit a record $73.6 billion in Q3 2025 according to Galaxy Research, surpassing the previous peak from Q4 2021. On-chain lending now commands 66.9% of that market.

To put that in perspective, the broader DeFi market is valued at $238.5 billion in 2026, projected to reach $770 billion by 2031.

What made this cycle different from 2021 is the collateral quality.

The previous boom ran on uncollateralized credit and opacity. This one is built on verifiable, overcollateralized positions with automated liquidation. And an expanding class of assets previously locked out of credit markets entirely.

The tokenized real-world asset market grew from $8.4 billion in early 2024 to over $24 billion by mid-2025. Active on-chain private credit surpassed $18.9 billion by late last year.

By early 2026, institutional RWA and DeFi TVL combined sits at roughly $17 billion, with tokenized Treasuries now outpacing decentralized exchanges as a source of on-chain collateral.

At this point, the question is no longer whether these assets can serve as collateral. We now have to ask whether they start competing with Treasurys for that role.

And the establishment’s answer to that is where things get interesting.

What Regulation Actually Did

Regulation has not stopped cryptos growing collateral competition.

In fact, it has formalized it.

The GENIUS Act — signed into law by President Trump in July 2025 — is the first major cryptocurrency legislation to become U.S. law. It requires payment stablecoins to be backed one-for-one by dollars or equivalent low-risk assets, and hands oversight to the OCC, FDIC, Federal Reserve and relevant state regulators.

Implementing rules from the OCC and FDIC were proposed in March and April 2026, with final rules due by July.

With MiCA already fully active across Europe, the regulatory era for stablecoins has arrived.

The reflex interpretation is that this brings crypto to heel — that reserve requirements and compliance layers re-anchor stablecoins to the sovereign system and restore central bank control.

That reading misses what regulation actually does to collateral dynamics.

Regulated stablecoins do not slow collateral velocity. They accelerate it. A GENIUS Act-compliant stablecoin backed by Treasurys …

- Settles instantly,

- Moves 24 hours a day, seven days a week,

- And is accepted across protocols with no geographic restriction.

Simply put, it is a faster, always-on version of the money market fund — and banks know it.

The ongoing fight over whether stablecoins can offer yield without draining bank deposits is not a technical dispute. It is banks defending their deposit base against a collateral instrument that outcompetes them on every operational dimension.

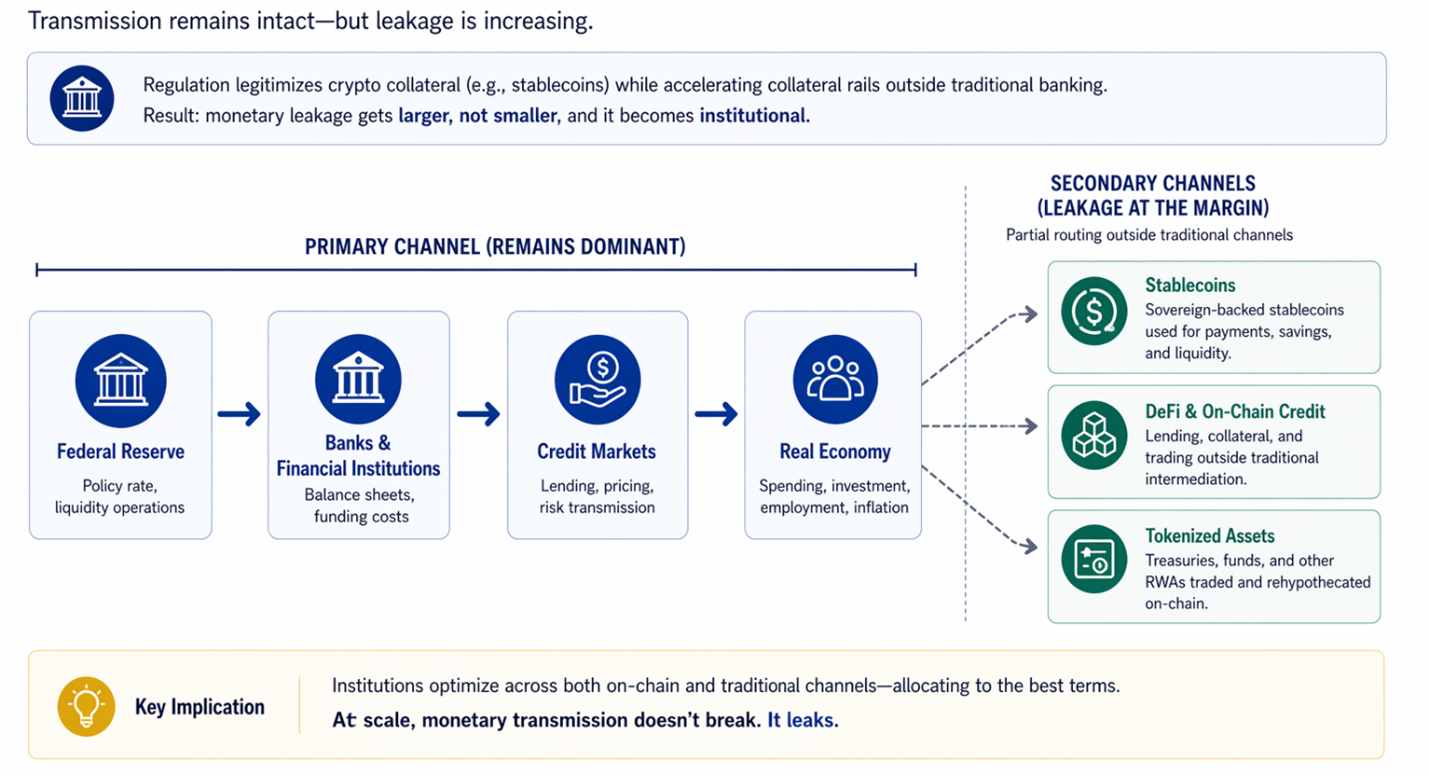

So regulation does two things simultaneously.

First, it legitimizes a class of crypto collateral by anchoring it to sovereign backing. And second, it accelerates the adoption of collateral rails that operate outside traditional banking channels.

In this way, the monetary leakage gets larger, not smaller. But more importantly, it becomes institutional.

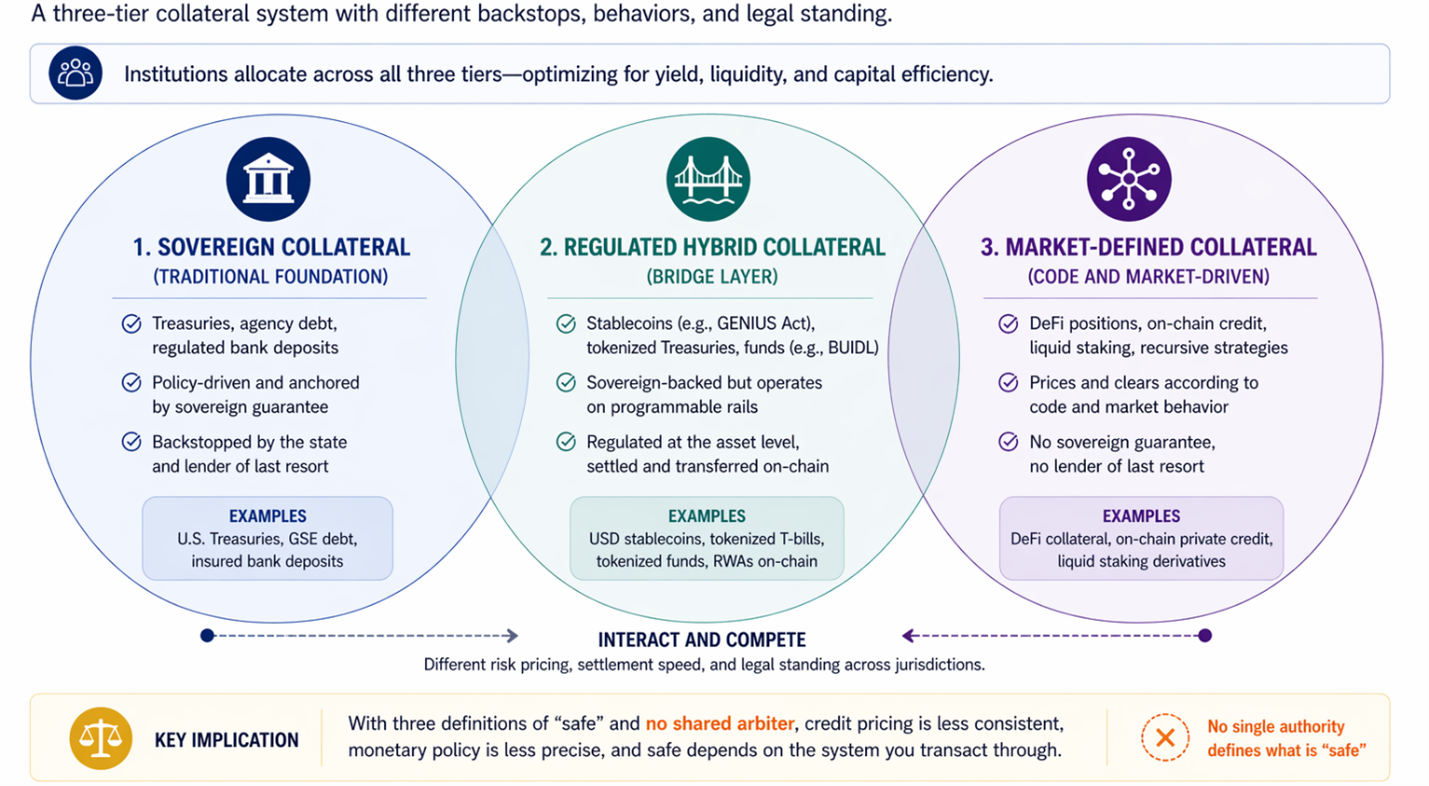

Three Tiers, Three Definitions of “Safe”

What has emerged, with or without intent, is a three-tier collateral system.

The first should be familiar: Sovereign collateral, which includes Treasurys, agency debt and regulated bank deposits. This remains the foundation of traditional credit markets, policy-driven and backstopped by the state.

Next comes the regulated hybrid tier. Collateral here including GENIUS Act stablecoins, tokenized Treasurys and BlackRock's BUIDL. It acts as a middle layer that carries sovereign backing while it operates on programmable rails.

Finally, there’s the market-defined collateral tier. This is where DeFi users live. Where unregulated DeFi positions, recursive liquid staking strategies, on-chain private credit counts as collateral. Here, prices and clears are according to code and market behavior, with no sovereign guarantee and no lender of last resort.

Understanding these three tiers is vital. Because they don’t behave identically under stress.

They price risk differently, clear at different speeds and carry different legal standing across jurisdictions.

That’s its own problem. As the Fed's influence over credit conditions depends on those tiers behaving consistently.

But they do not.

Which is why yield-bearing stablecoins in institutional treasury strategies grew from $9.5 billion to over $20 billion over the past year.

Institutions are already optimizing liquidity across bank deposits, money market funds and stablecoins — rotating toward whichever instrument offers better terms.

That is regulatory arbitrage at the collateral level.

BCG and Ripple project the tokenized asset market could reach $19 trillion by 2033. At that scale, monetary transmission does not break. It leaks.

And leaky transmission is the kind of problem central banks only discover after inflation has already moved.

Who Absorbs the Loss

The Housing Crisis in 2008 was defined by mispriced collateral within the sovereign system. However, the mortgage-backed securities at the center of this collapse were ultimately backstopped by federal guarantees.

What is being built now is collateral defined outside that system — or at least, alongside it with no shared enforcement mechanism.

The communal nature of the third tier — market-defined collateral — ideally should prevent mispriced collateral. But the Terra/LUNA collapse also taught us the risk of being wrong without a failsafe.

Research published in the Journal of Risk and Financial Management documented how the speed at which failures propagate across governance tokens, stablecoin pegs and oracle infrastructure in DeFi.

Ideally, the hybrid tier will take the strengths of both sovereign and market-defined collateral to overcome the potential pitfalls of both. However, that is an optimistic outlook with little to confirm how likely that is. Because one key question that no regulatory framework has answered — not GENIUS, not MiCA — is what happens when the tiers disagree.

What happens if a TradFi institution that holds tokenized assets faces a margin call … while an on-chain protocol prices the same asset differently?

It can happen. Afterall, these tiers operate under different rules, in no common jurisdiction and with no shared enforcement mechanism.

That gap is the central risk of the next credit cycle.

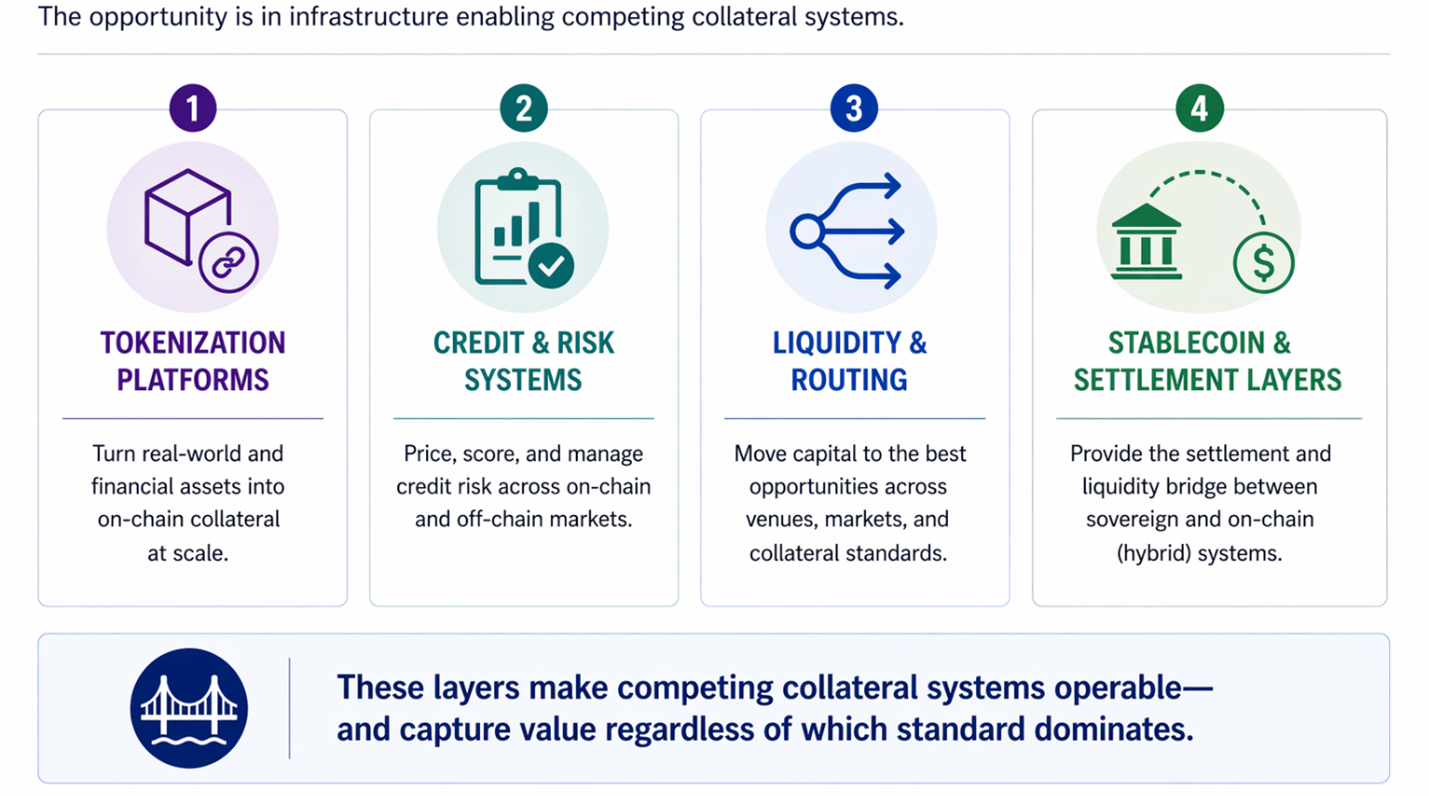

Where the Investment Case Sits

The opportunity for investors lies is in the firms building the infrastructure that makes competing collateral standards operable.

These include your …

- On-chain credit scoring systems,

- Liquidity routing protocols,

- And regulated stablecoin issuers bridging the sovereign and hybrid tiers.

These are picks-and-shovels plays in a credit infrastructure buildout that regulation has now accelerated rather than contained.

The macro implication is harder to trade. But it is more important to understand.

A world with three collateral standards — sovereign, hybrid and market-defined — is a world where credit pricing is less consistent …

Monetary policy is less precise …

And the meaning of “safe” collateral is determined not by a single authority but by whichever system an institution happens to be transacting through.

And from this point on, the system will behave differently from anything we’ve seen before.

For investors, especially those using leverage both on-chain and off, this trend needs to be on your radar.

Because how this new tiered system plays out will become pivotal in optimizing strategies and targeting long-term success.

Best,

Jurica Dujmovic