|

| By Jurica Dujmovic |

The spending numbers at the top of the AI story have become genuinely difficult to contextualize.

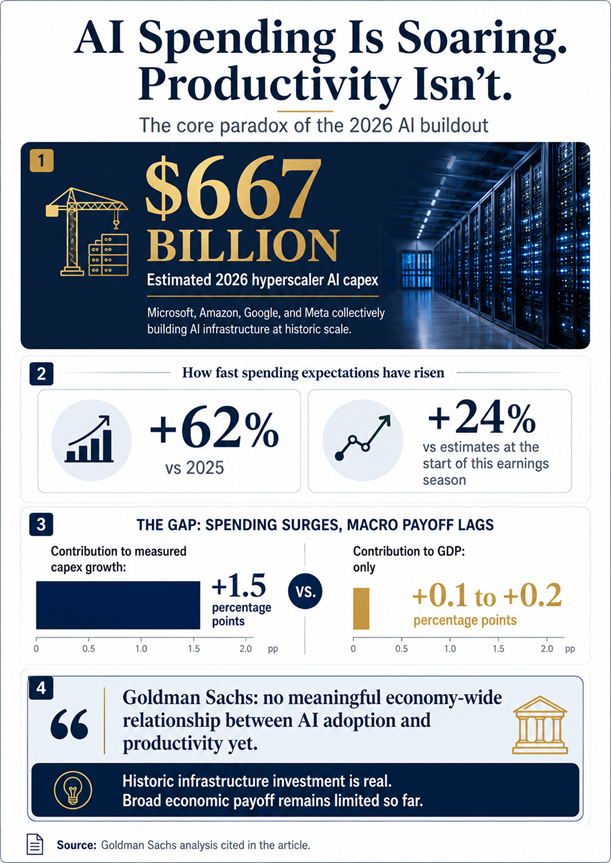

Analysts recently readjusted their capex projections for hyperscalers. Now, they expect those tech giants to invest roughly $667 billion in long-term infrastructure this year. That’s a 62% jump from 2025 and a 24% increase from estimates made at the start of this year's earnings season alone.

Microsoft, Amazon, Google and Meta are collectively building AI infrastructure at a pace that has no precedent in the history of corporate capital allocation.

Measured purely by investment, the AI era has never looked more real.

But that’s not the only measurement that matters.

Experts Identify a Concerning Gap

Those who crunch numbers for a living can’t help but notice that something isn’t adding up.

Goldman Sachs economist Ronnie Walker recently analyzed fourth-quarter corporate earnings. The result? He and his team did not find a meaningful relationship between productivity and AI adoption at the economy-wide level.

That $667 billion investment in AI by hyperscalers is expected to contribute roughly 1.5 percentage points to measured capex growth this year. But that’s only expected to convert to 0.1 to 0.2 percentage points in GDP.

In short, the economic return on investment hasn’t yet appeared in the projected data.

That gap is the story of AI in 2026.

And it is a more interesting investment story than either the infrastructure bulls or the doomsayers are currently telling.

Because the gap is not uniform. It is bifurcating, rapidly, in ways that the market is only now beginning to price.

What the Return Data Actually Shows

Two surveys bracket the state of enterprise AI returns in 2026. And they paint a consistent picture.

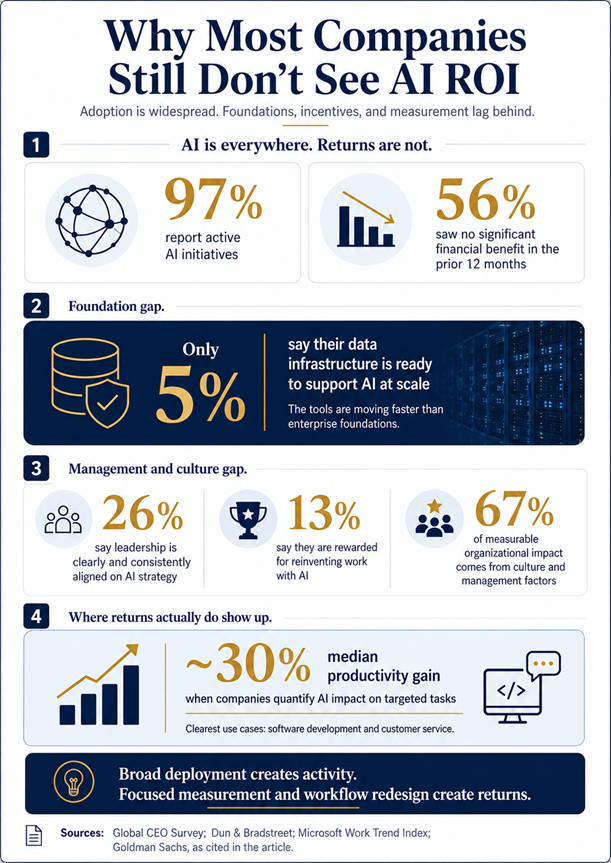

The first is the 29th Global CEO Survey. Published at Davos in January, it drew on responses from 4,454 CEOs across 95 countries. And it found that 56% of companies had seen no significant financial benefit from AI in the prior 12 months.

That means more than half of all businesses that invested and used AI didn’t see higher revenues or lower costs within a year.

The second is a Writer and Workplace Intelligence survey of 2,400 executives and employees, published in April 2026. It found that 97% of companies have deployed AI agents in the past year. And of those, 79% of executives struggle with lagging ROI or strategy gaps.

Only 29% report significant returns from generative AI.

The survey captures a specific failure mode that runs through every dataset on this topic: Individual productivity gains from AI are real and measurable. But translating them into organizational financial outcomes is where almost everyone gets stuck.

Separately, BCG's 2026 AI Radar found corporations planning to double their AI spending in 2026 to approximately 1.7% of revenues, with 90% of CEOs committed to continuing investment even if returns take time to materialize.

Simply put, the money is flowing unconditionally. But it seems early returns are arriving selectively.

The Problem Isn’t AI; It’s How We Approach It

The technology is not the bottleneck. A Dun & Bradstreet survey of 10,000 businesses published in May found that 97% report active AI initiatives.

The problem is everything around the technology.

Only 5% of those businesses say their data infrastructure is ready to support those initiatives at scale. And Microsoft's 2026 Work Trend Index, found that only 26% of AI users say their leadership is clearly and consistently aligned on AI strategy.

And that last bit can’t be ignored. In fact, it’s one of the main causes of this gap, as the report attributes 67% of AI's measurable organizational impact to cultural and management factors — not to the models themselves.

On April 13, PwC released a dedicated AI Performance Study. Based on interviews with 1,217 senior executives across 25 sectors at large, publicly listed companies, the study found that 74% of AI's total economic value is being captured by just 20% of organizations.

The remaining 80% are sharing what is left.

The key difference between the winners and the losers is simple: Those in the top 20% are using AI as a catalyst for growth and revenue reinvention.

The rest remain focused on cost reduction applications that produce narrow, hard-to-measure gains.

The result is an enterprise landscape where AI is nearly universal at the deployment level and nearly absent at the financial outcome level.

PwC is explicit: Without a shift in approach, the gap is likely to widen further.

Where Returns Actually Exist

Goldman's analysis provides a useful complement to PwC's macro picture. It found that management teams specifically quantifying AI-driven impacts on targeted tasks reported a median productivity gain of around 30%.

The pattern across all the data is consistent: Concentrated deployment in well-defined workflows, with clear measurement built in from the start, produces real returns. Specifically, the data bears this out most in software development and customer service.

Goldman Chief Global Equity Strategist Peter Oppenheimer notes that this is nothing new. History is littered with infrastructure buildouts that attracted enormous capital … only to see low returns. Even when the underlying technology proved genuinely transformative.

The Investment Implication

This is not a bubble call.

The technology works — Goldman's 30% productivity gains in targeted use cases are real, and PwC's 25%-40% gains for AI leaders are not noise. The infrastructure being built by hyperscalers will be used.

The question is who will capture the value when the productivity dividend finally broadens.

No one can say that for sure at the moment. But I can say that broad AI exposure — owning the index, the infrastructure basket, or the category — is ultimately a bet that the 80% can close the gap with the 20%.

With the evidence pointing the other way, savvy investors should start to narrow their AI exposure.

Here are the signs that, in my opinion, indicate an opportunity likely to find itself in the successful 20% ….

-

How management talks about AI. Do decision makers understand AI in terms of revenue, product design and customer experience? Or is their focus mostly on internal efficiency?

Cost-cutting AI can be useful, but the upside is usually narrower and harder to prove. Product-level AI is where the leaders appear to be separating.

- Whether there are measurable workflow gains. A company that can point to shorter software cycles, lower service costs, higher conversion rates or faster product launches is giving investors something more concrete than adoption statistics.

- Whether the foundation for AI success and scalability has already been built. That means integrated systems, clear ownership, incentives and management alignment. Those are not flashy developments, so you may have to dig deep to find them. But they are what turn AI from a tool into an operating advantage.

Now, here’s a red flag to avoid: A company that keeps increasing AI spending while describing the payoff in vague language.

You want a pick that can show where AI is already changing margins, revenue, speed or customer behavior.

That’ll be the biggest indicator whether a company is turning to AI because it’s trendy … or if can actually convert today’s spending into tomorrow’s returns.

Best,

Jurica Dujmovic

P.S. To help you narrow down opportunities for long-term AI exposure, I encourage you to check out Weiss Ratings Plus.

This useful tool can help you find the top Weiss-rated stocks in any sector, including AI. Plus, it puts all of our research right at your fingertips.