Here's What Jabil's Blowout Quarter Doesn't Tell You

We're stepping outside the usual crypto headlines today. But stay with us, because this one's closer to home than it looks.

The same data centers that power the AI boom are increasingly the same buildings your favorite Bitcoin (BTC, “B+”) miners are sitting in.

Core Scientific, Cipher Mining, IREN and Hut 8 are companies that used to live and die by hashrate.

Now, they are now hosting AI compute in the same racks, cooled by the same systems, built by the same handful of suppliers.

One of those suppliers is Jabil (JBL, “B-”).

Its latest earnings offer a useful test case for a thesis that crypto investors already know well.

That is, buying the shovel maker instead of the miner.

Particularly as it relates to a shovel maker that Bitcoin miners now depend on.

|

| By Jurica Dujmovic |

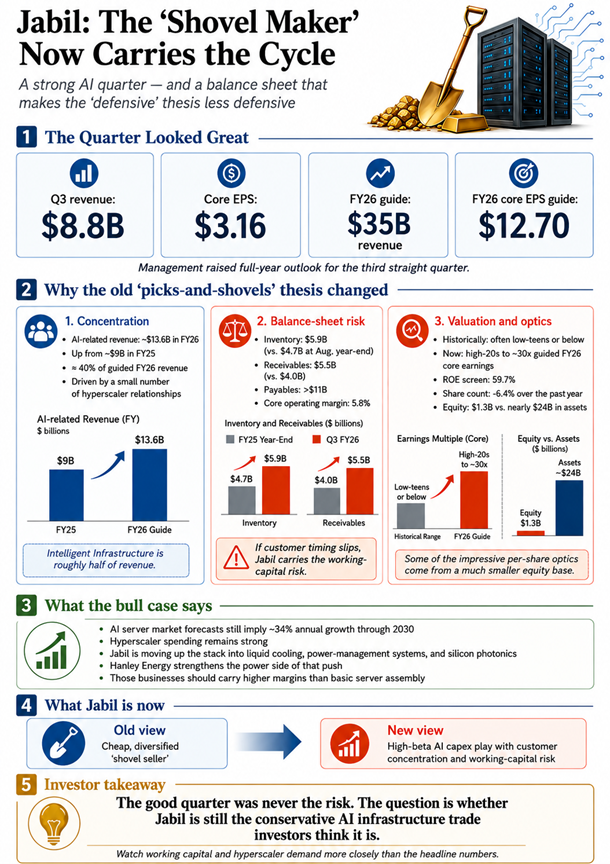

Jabil reported its fiscal third-quarter1 results Wednesday.

The numbers did exactly what the picks-and-shovels story promises.

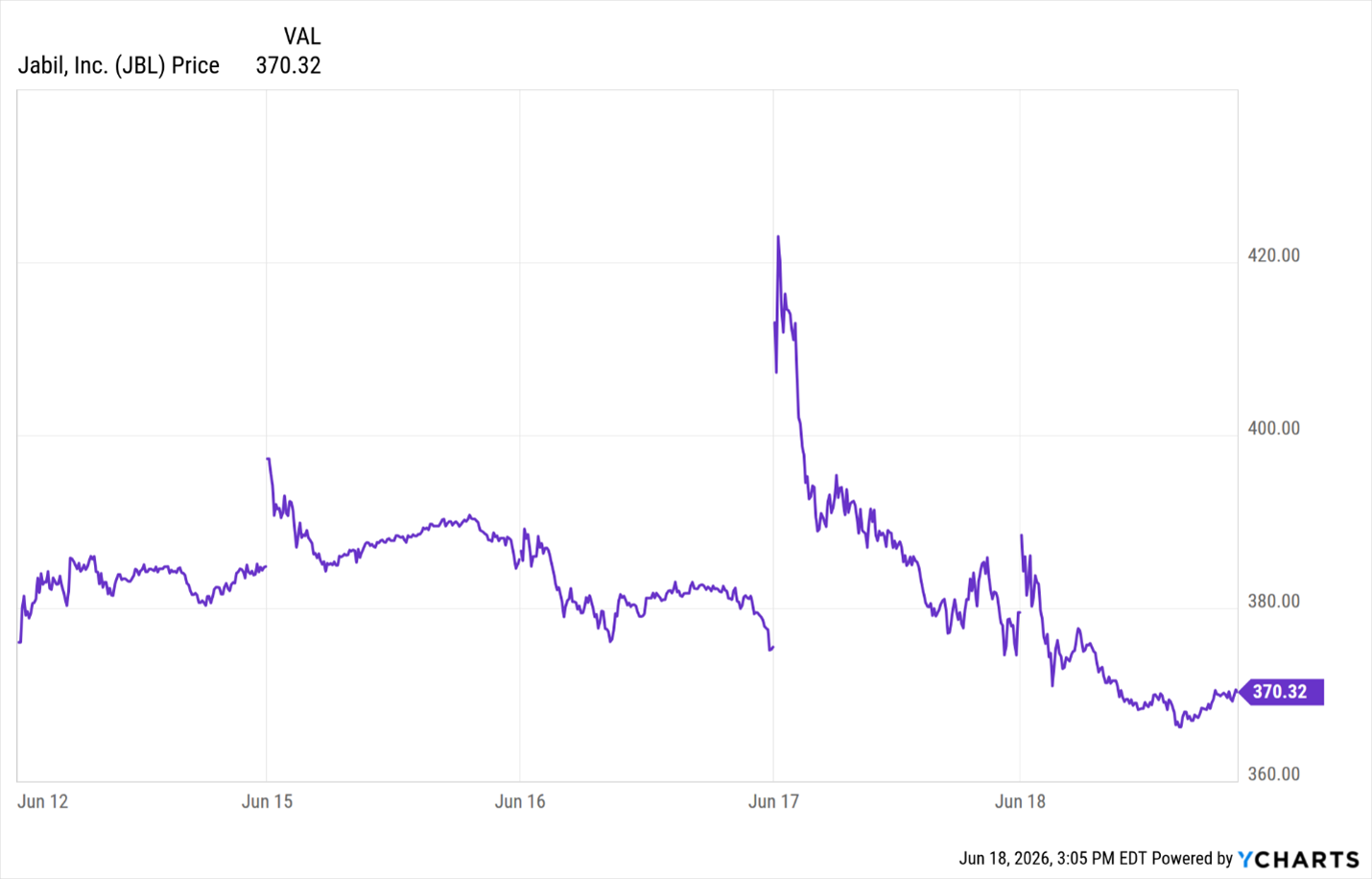

Still, you can see the big gap higher … and quick descent … on its earnings announcement day.

AI infrastructure demand was described as extremely strong. And the company's full-year AI revenue figure went higher.

The stock has more than doubled over the past year.2 Investors were happy. And it appears many took profits.

Or perhaps some more astute investors read the rest of the filing.

The appeal of Jabil has always been that you do not have to guess which AI company wins.

After all, it builds the hardware: server racks, networking gear, liquid cooling, power systems, and the semiconductor capital equipment that makes the chips that go into the racks.

In a gold rush, the logic goes, sell shovels. You collect a fee on everyone's digging and stay neutral on whose claim pans out.

It is a genuinely good model. And for a while, the market priced it like one, at single-digit to low-teens multiples3 of earnings.

A contract manufacturer that turns enormous revenue into thin margins is supposed to trade cheap. That was the deal.

The deal has changed, and the first place it shows is concentration.

The Intelligent Infrastructure segment, the cloud and data center side, is now roughly half of revenue.

It’s been growing better than 50% year over year, with AI-related work guided on Wednesday's call to around $13.6 billion4 for the year. That’s up from about $9 billion the year before.

By the company's own reckoning, AI infrastructure already drives about 40% of revenue.

That growth is not spread across a thousand prospectors.

It rides on a small number of anchor hyperscaler relationships. Management said in March that it was ramping a second hyperscaler and in discussions with a third.5

Selling shovels to the whole camp is diversification.

Selling them to a few miners — who happen to be spending more than anyone in history — is a leveraged bet on a handful of capital budgets staying open.

That is a different risk, wearing the same hardhat.

The second place it shows is the balance sheet, which is where the “neutral middleman” framing quietly falls apart.

A toll collector does not carry the cycle. Jabil now does.

Inventories climbed to $5.9 billion6 from $4.7 billion at the August year-end, and receivables rose to $5.5 billion from $4.0 billion.

The company is buying components and carrying product ahead of shipments it expects to make. It finances a good chunk of it by stretching its own payables past $11 billion.

When demand keeps accelerating, that working-capital build is just the cost of growth.

If that timing slips, even for a quarter, a 5.8% operating margin does not leave much cushion for excess inventory, delayed receivables, or customers pushing orders to the right.

This is supply-chain timing risk: parts, racks and finished goods have to move on the schedule customers implied.

Otherwise, the balance sheet starts doing the speculating.

The third place it shows is the price.

The market has taken a business guiding to $35 billion of revenue … and roughly $1.3 billion-plus of non-GAAP core earnings …

And re-rated it from the single-digit-to-low-teens multiple it carried for years to roughly 28x this fiscal year's guided core earnings.7

That’s the kind of valuation normally reserved for growth compounders.

The 59.7% return on equity8 that screens so beautifully is partly an accounting mirage.

Jabil has spent years shrinking its share count, including a 6.4% reduction over the past year.

And its equity has fallen to just $1.3 billion against nearly $24 billion in assets.

A smaller denominator flatters every per-share figure.

Part of the earnings growth investors are now paying a premium for is arithmetic, not operations.

The low multiple was not a knock on the company.

It was the market pricing the business accurately.

Electronics manufacturing services is a business with structurally thin margins and almost no pricing power.

That’s because the customer owns the design and has the option to move the work elsewhere.

The contractor absorbs the volatility and keeps a sliver of the value.

Markets have fallen for the growth version of this story before.

They repriced the assemblers during past capital-spending booms. Then they took the multiple straight back when the cycle rolled over and a few large customers trimmed orders at once.

The hardware changes. The position in the food chain does not.

Buying an assembler at a compounder's multiple is a wager that this cycle — unlike every previous one — does not end with the customers blinking first.

Put the three together, and the picks-and-shovels thesis inverts on itself.

The entire point of buying the shovel maker instead of the miners was caution: neutrality across the field, and a cheap multiple as a margin of safety.

Jabil has surrendered the neutrality, since its fortunes now track a handful of hyperscaler spending plans.

It has surrendered the cheap multiple, since it trades like a growth compounder.

And it has added balance-sheet risk it did not used to carry.

None of that means the quarter was anything other than excellent, because it was.

It means the safety that justified the trade has been spent.

The bull case is not naive, and it deserves a fair hearing.

- Some forecasts still put the AI server market on a roughly 34% annual growth path through 2030,9

- Hyperscaler budgets show no sign of closing, and

- Jabil's push up the value chain into liquid cooling, power-management systems and silicon photonics is real.

Hanley Energy strengthens the power side of that push.

Those businesses are higher-margin than basic server assembly.

- Celestica has more than tripled10 over the past year on the same theme.

- Sanmina paid about $3 billion to buy ZT Systems' data-center manufacturing business11 from AMD to chase it.

- And the broader contract-manufacturing shelf has re-rated alongside them.

If compute demand keeps outrunning supply for another two years, today's multiple will look reasonable in hindsight.

The bet can keep paying.

The question is whether it is still the conservative bet it was sold as.

Where This Leaves Investors

Treat Jabil as what it has become — a high-beta AI-capex play, not a defensive infrastructure holding.

Investors looking for AI infrastructure exposure with less direct EMS execution risk may want to look one layer deeper.

So, companies that sell components and subsystems across broader customer sets like:

- Amphenol (APH) in connectors,

- Vertiv (VRT) in cooling and power, and

- Lumentum (LITE) in optical.

The direct comparables are the other contract manufacturers:

- Celestica (CLS),

- Flex (FLEX), and

- Sanmina (SANM).

All carry the same customer concentration and cyclicality. So, owning several of them does not diversify the underlying bet.

The business is firing, the stock is priced for it to keep firing, and the balance sheet has quietly stopped being boring.

Investors should watch working capital and any wobble in hyperscaler demand more closely than the headline numbers.

Jabil delivered the quarter bulls wanted; the risk is that investors are now paying for a safety story that no longer fits.

Best,

Jurica Dujmovic

1 https://www.sec.gov/Archives/edgar/data/0000898293/000162828026043719/jbl-20260617ex991.htm

2 https://stockanalysis.com/stocks/jbl/statistics/

3 https://www.macrotrends.net/stocks/charts/JBL/jabil/pe-ratio

6 https://www.sec.gov/Archives/edgar/data/0000898293/000162828026043719/jbl-20260617ex991.htm

7 https://www.sec.gov/Archives/edgar/data/0000898293/000162828026043719/jbl-20260617ex991.htm

8 https://stockanalysis.com/stocks/jbl/statistics/

9 https://www.marketsandmarkets.com/Market-Reports/ai-server-market-141336410.html

10 https://www.fool.com/investing/2026/05/06/this-super-artificial-intelligence-ai-stock-has-so/