|

| By Beth Canova |

You don't think twice about sending an email across the world. Because you don't have to. But sending money that far still requires a waiting period.

Credit and debit cards dominate payments today. But merchants don't receive those funds for days. Cash was supposed to be the fastest option, but it’s disappearing — from 31% of all consumer payments in 2016 to just 14% in 2024.

Nothing clean has replaced it.

Until stablecoins.

They can enable instant, low-cost global payments. That means value stability in volatile markets and access to financial tools for those whose local currencies have inflated far worse than the dollar.

Within crypto, stablecoins also act as a coordination layer — a bridge between digital assets and the traditional financial world. You can hold them temporarily, then move into assets that better preserve your purchasing power.

But this solution comes with a catch.

Why Digital Dollars Aren't Enough

Stablecoins are digital dollars backed by a centrally issued currency, typically the U.S. dollar.

And we talk about them often within the context of the crypto ecosystem. But there’s a catch that most people forget about …

They are a bridge from the existing financial system. Not a break from it.

All the buzz in financial circles amounts to this: We are upgrading old money to a better database. But it is still the old money. Just with more surveillance than ever before.

The only difference between a stablecoin and a central bank digital currency (CBDC) is who issues it and who controls it.

CBDCs are controlled by central banks, which is why many crypto enthusiasts steer clear of them. But the most popular dollar-pegged stablecoins are controlled by centralized entities, as well. And they’re also at the mercy of the government.

If you are acting outside their definition of "good faith," your finances can be cut off. Same as before.

Circle — the company behind one of the largest stablecoins, USDC — has blacklisted wallet addresses at regulators' request. That includes a 2022 government crackdown on a privacy tool called Tornado Cash.

But beyond the threat of external control, there’s another concern: Dollar-backed stablecoins bring the dollar’s decline on-chain.

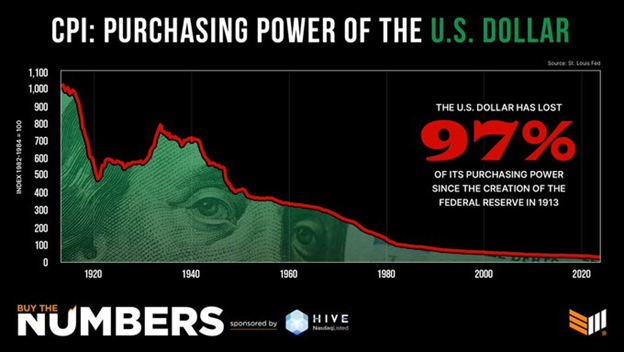

Since 1913, the dollar has lost 97% of its purchasing power. It is a currency built on debt. Wrapping that debt in digital code does not change the math.

By moving dollars into the crypto world, stablecoins create even more demand for a currency that is melting away.

That’s not a cure. That’s fuel for the fire.

This doesn’t mean you should discard your stablecoins. Far from it. Rather you should be careful what your stablecoins are backed by.

Because within crypto, there are far more use cases than fiat-backed stablecoins.

Grow Beyond the Dollar Trap

Stablecoins are scaffolding. Not the destination.

Today, U.S. dollar-backed tokens like USDC and USDT (digital dollars you can hold in a crypto wallet) make up more than 95% of the stablecoin market. They are useful for one thing: temporary shelter when markets get rough.

But holding them long-term means accepting the same 97% purchasing power erosion that plagues the paper dollar.

The dollar is the problem. And its digital version does not solve its underlying weakness.

So, if you must use a centralized stablecoin, my recommendation is that you do so as a bridge or part of a DeFi strategy. Not as a home for your idle capital.

And if you want stability without the dollar's debt, look at gold-backed tokens like Pax Gold (PAXG, stablecoin) or Tether Gold (XAUT, stablecoin), which are pegged to the price of physical gold.

In fact, Juan Villaverde’s Weiss Crypto Investors were able to pocketed a triple-digit gain on their PAXG earlier this year. To see how Juan’s Crypto Timing Model helped them pocket this win, click here.

There are also decentralized stablecoins, like USDS (formerly DAI). These are backed by code and digital assets, rather than a bank deposit. And they exist outside the control of any central authority.

Best,

Beth Canova