|

| By Mark Gough |

Most stablecoin coverage follows the same script …

The market is massive. Growth is explosive. Traditional payments are about to be disrupted. Banks are scrambling. Soon we’ll all be buying coffee with USDC.

But a new McKinsey report, Beyond Stablecoins: The Emerging Architecture of On-Chain Money, offers a much more grounded perspective.

Not because stablecoins are failing.

But because the larger investment opportunity may be developing elsewhere.

The Headline Number Doesn’t Tell the Full Story

Stablecoins processed roughly $35 trillion in transaction volume last year.

That figure gets repeated constantly, usually alongside comparisons to Visa (V) or Mastercard (MA).

It sounds enormous.

But here’s where the average investor can get lost in the data: Transaction volume and genuine economic activity are not the same thing.

Researchers stripped out actual payment activity from the surrounding market noise. And what they found was shocking …

The estimate came in at ~$400 billion in organic payment flows, supplier settlements, remittances, payroll and real-world commercial transactions.

That means roughly 99% of the reported volume wasn’t actual payment activity. The rest came from trading activity, arbitrage, exchange transfers, internal wallet movements and automated DeFi settlement.

None of that invalidates stablecoins as infrastructure. Crypto markets generate legitimate demand for fast settlement.

But it does challenge the idea that stablecoins have already become a mainstream global payments rail.

And it reveals a potentially bigger infrastructure opportunity.

The Bigger Story Is Inside the Banking System

While crypto markets focused on stablecoin adoption, major financial institutions built their own blockchain payment infrastructure.

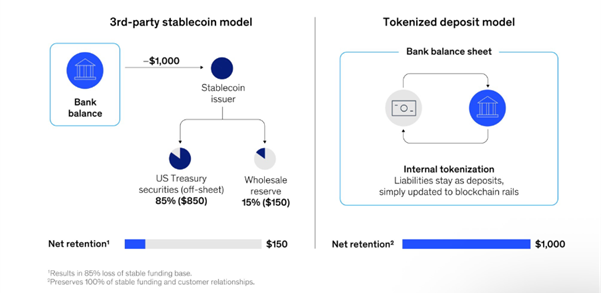

Rather than keep capital in third-party stablecoins like USDC or USDT, banks can now use stablecoins to tokenize their deposits.

Why would they do so? To get the benefit of the blockchain while keeping their capital inside their existing financial systems.

The scale of this strategy is already substantial.

JPMorgan’s Kinexys platform now handles more than $1 trillion annually in tokenized payment flows, largely across treasury management and institutional settlement.

That’s just one institution …

- Citi has active tokenization initiatives.

- BNY Mellon has live infrastructure.

- More than a dozen institutions are already running pilots or production systems.

Across the broader banking system, tokenized deposit flows are already estimated above $4 trillion annually. That makes the actual stablecoin payments market look relatively small by comparison.

For institutional treasury teams, the decision is straightforward …

Option 1: Adopt a third-party stablecoin that requires new counterparties, fresh operational risk frameworks and expanding compliance obligations.

Option 2: Use tokenized dollars issued by your existing banking partners.

The volume data suggests institutions already know their preference.

This matters for one key reason: It’ll determine if your stablecoin infrastructure plays are on the winning track.

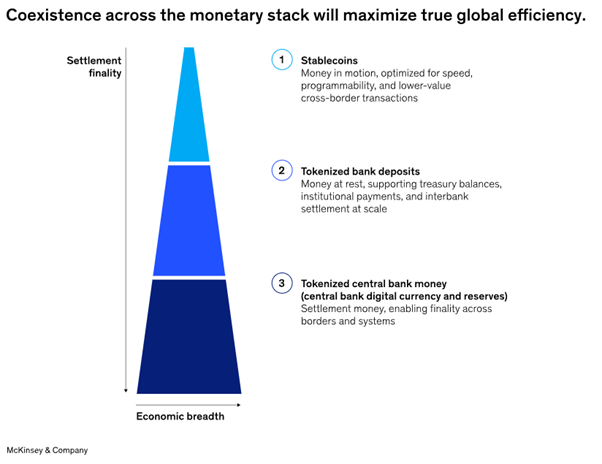

See, this tokenization of bank deposits is just one part of a three-layer system McKinsey has identified.

The evolution of this sector from a single, dominant asset — stablecoins as a whole — to a fragmented system where types of stablecoins can coexist and interact could redefine the future of on-chain dollars.

And how investors need to approach it.

That’s because this new system is facing the exact same problem as early crypto.

The Real Bottleneck

This is where the investment story gets interesting: Tokenized deposits may already be moving trillions, but they remain fragmented.

A tokenized JPMorgan dollar works inside JPMorgan’s ecosystem. That does not automatically make it interchangeable with a tokenized Citi dollar.

The banking sector has effectively created blockchain-based payment islands. Just like how, in the early days of crypto, each network was its own island.

Naturally then, the next major goal is seamless connectivity between those systems.

That is where the real infrastructure opportunity sits …

- Shared settlement networks

- Orchestration layers connecting traditional financial rails

- Interoperability protocols bridging separate systems.

The bigger opportunity may not be stablecoin issuers themselves. It may be the infrastructure providers enabling communication between fragmented digital money systems.

Because once multiple forms of digital money begin operating at scale, somebody has to connect them.

What Investors Should Focus On

To be clear, this new analysis does not invalidate the stablecoin thesis.

Stablecoins clearly have product-market fit in cross-border payments and crypto-native settlement.

What it does tell us is that the cleaner investment opportunity may sit deeper in the stack.

The interoperability rails.

The identity and compliance middleware.

The oracle infrastructure linking traditional financial systems with blockchain networks.

The settlement layers connecting closed banking ecosystems with open digital asset markets.

The more interesting investment question may not be whether stablecoins win. It may be who earns fees connecting stablecoins, tokenized deposits and settlement systems once they all need to interoperate.

In short, digital finance is starting to look less like disruption and more like infrastructure modernization.

And that may be where the real long-term opportunity sits.

Best,

Mark Gough