|

| By Jurica Dujmovic |

America's most powerful monetary actors now include Tether and Circle. Washington is only beginning to understand what that means.

The Federal Reserve controls interest rates, manages the money supply and serves as the lender of last resort for the world's reserve currency.

It is the most powerful financial institution on the planet, which is why it is designed to be independent.

Now imagine a private company — no elected officials, no public mandate, no emergency backstop — quietly taking on many of the same functions.

That company doesn't exist yet. But the system for one already does.

Crypto’s Shadow Central Bank

Over the past several years, stablecoins have graduated from crypto's internal plumbing to something considerably more consequential: a private, parallel dollar-liquidity layer.

And it isn’t idle. It now intersects with the U.S. Treasury market, short-term funding markets and the monetary system itself.

Let’s start with the balance sheets …

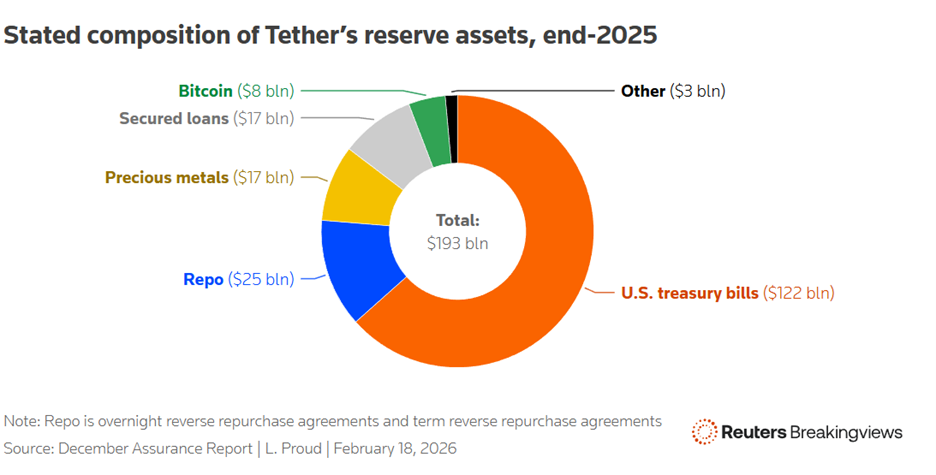

Tether, the issuer of USDT, has accumulated $122 billion in U.S. Treasury holdings. To put that into perspective, that’s so large that it can be compared to a mid-sized sovereign nation. In fact, at one point, Tether held more U.S. Treasury notes than Germany.

This puts it squarely among the world's significant buyers of short-term U.S. government debt.

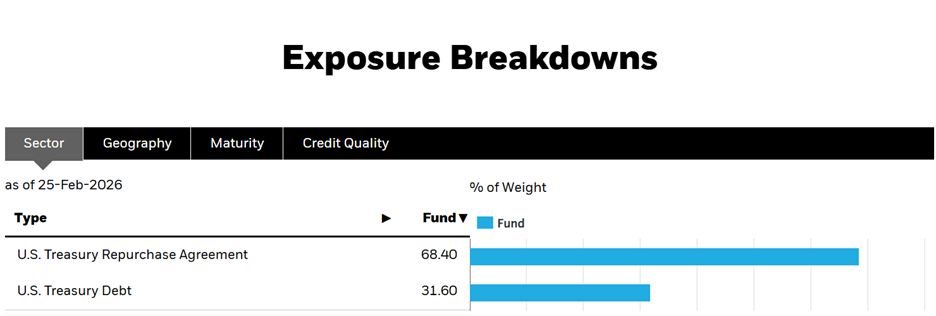

Circle, the issuer of USDC, backs its reserves through the BlackRock Circle Reserve Fund, a money-market-like vehicle that channels stablecoin circulation directly into Treasury instruments.

Circle's USDC circulation has surpassed $75 billion, generating reserve income at a scale that looks increasingly like bank seigniorage.

These are not marginal holdings, either. The Financial Stability Oversight Council has explicitly flagged stablecoin issuers. That’s because the concentration of Treasury demand is significant enough that a disorderly run could force large-scale asset liquidations.

And as we know, that could have serious consequences for broader asset pricing.

The policy establishment has noticed this trend. The markets have noticed.

What remains is for retail investors like us to notice … before the next stress event makes it impossible to miss.

The Run Mechanics Look Familiar

The New York Fed established what practitioners had long suspected: Stablecoins tend to show flight-to-safety dynamics and break-the-buck-style acceleration under stress.

That behavior is functionally similar to what we see in money market fund runs.

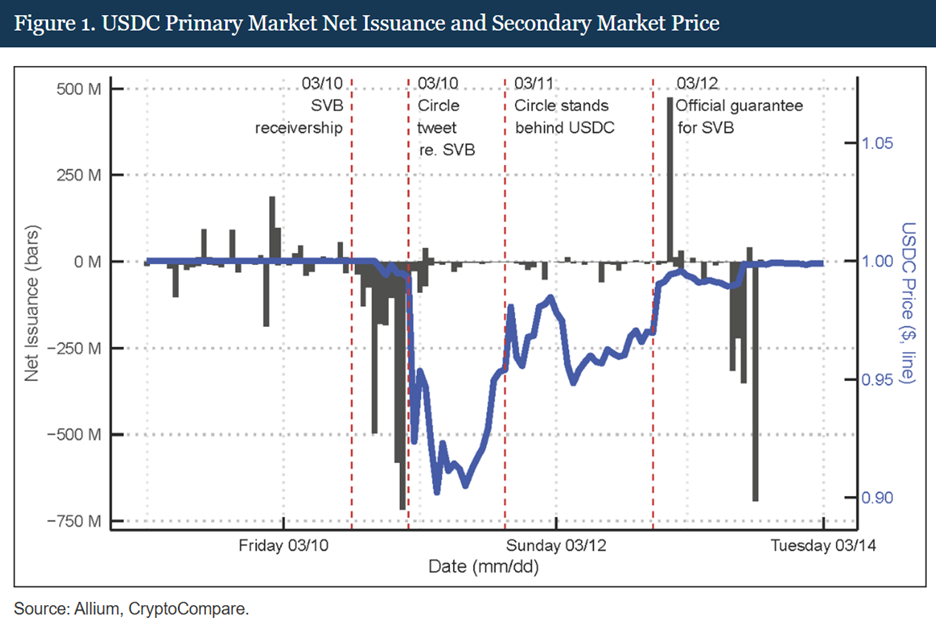

We even had a stress test: The Silicon Valley Bank collapse in March 2023. Federal Reserve FEDS Notes documented how SVB's failure transmitted directly into USDC markets. This caused the stablecoin to lose its peg to the U.S. dollar.

It was a quick moment of weakness that briefly pushed the coin to 87 cents. But even though the markets stabilized and system moved on, it still happened.

And it was enough to shake investor confidence.

But at the time, the scale was still small enough that liquidation pressure could be absorbed without visible disruption to the broader funding system.

In short, the shock remained recognizable as a crypto-only story.

Today, stablecoin reserves are embedded even deeper in the U.S. Treasury market. The major dollar-backed stablecoins collectively hold hundreds of billions of dollars in short-term government securities.

Which means that if we have a similar run, it’s unlikely the shock will stay contained.

A 10% outflow at current scale would imply tens of billions of dollars in forced transactions over a compressed time frame.

In a market that prices liquidity in basis points, that magnitude matters.

The Bottom Line

Stablecoins are now large enough to influence the market that underpins global dollar funding. Yet they remain structurally redeemable liabilities — promises of one dollar, payable on demand, backed by finite pools of assets that must be sold if confidence falters.

And that’s a big potential glitch in the system.

The IMF’s recent modeling of systemic stablecoin redemptions describes the mechanism plainly:

- redemption pressure compels reserve liquidation

- liquidation transmits stress into bond market liquidity

- liquidity stress widens spreads and distorts pricing

A sufficiently large redemption episode would not remain a confidence event inside crypto markets, as it has in the past.

Now, the scale is great enough that it would register as liquidity pressure inside the Treasury market itself.

As long as redemptions remain orderly, that overlap appears manageable. The open question is how the system behaves when they are not … and whether the institutions responsible for stabilizing dollar liquidity will be prepared for a disturbance that originates outside their own balance sheets.

To be clear, this isn’t a call to abandon your stablecoin strategies.

But it does mean you now need to be aware of the bigger picture to keep those strategies — and your capital — safe.

Best,

Jurica Dujmovic