The Enormous Tax Time Bomb Hidden in Most Retirement Accounts

|

| By David Phillips |

When I last wrote to you, I told you that a proper estate plan needs to consider everyone involved — spouses, children and other beneficiaries.

Today, I’m giving you another setback I don’t want to see you make when you plan your estate — not fully considering taxes.

It’s the next part in our monthly series examining the 10 Most Common Estate Planning Mistakes and How to Avoid Them.

You Pay Too Much Income & Capital Gains Tax

At first glance, this may not seem like an estate planning issue.

After all, most people think of taxes as simply a cost of investing or earning income.

But over time, excessive taxation quietly erodes wealth, reduces flexibility and diminishes what eventually passes to the next generation.

For many affluent retirees, taxes may ultimately become one of the largest financial expenses they face.

The unfortunate reality is that many investors spend decades building assets without fully considering how those assets will eventually be taxed.

They focus heavily on accumulation but very little on distribution efficiency.

That can become a costly mistake.

Today, many retirees hold substantial portions of their net worth inside qualified retirement accounts such as IRAs and 401(k)s.

These accounts can provide valuable tax deferral during working years.

But eventually, the tax bill arrives.

And far too many are surprised to learn that, along with their nest egg, they’ve also built a large “IOU” to the IRS!

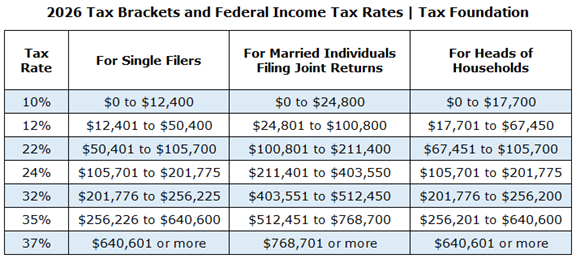

Required Minimum Distributions force taxable income into retirement years, whether the money is needed or not.

Those distributions can:

- Increase taxable income.

- Impact Medicare premiums.

- Increase taxation on Social Security benefits.

- Push retirees into higher brackets than expected.

The problem does not stop there.

Under the “Setting Every Community Up for Retirement Enhancement (SECURE) Act of 2020,” most non-spousal beneficiaries now have only 10 years to fully distribute inherited retirement accounts.

This creates a potentially significant tax burden for children and grandchildren, who are often already in their peak earning years.

As a result, they push off the distribution as long as possible, creating an enormous tax time bomb that will explode in the 10th year.

In many cases, families unknowingly leave behind highly taxable inheritances.

Another common mistake is assuming that all investment growth is created equally.

Traditional brokerage accounts may provide liquidity and flexibility. But they also create ongoing exposure to capital gains taxes, dividend taxation and market volatility.

While long-term capital gains rates are generally favorable today, tax laws change.

Investors who build their retirement plan entirely around assumptions of permanently low tax rates may eventually find themselves disappointed.

This becomes especially important when we consider the direction of federal spending, deficits and long-term debt obligations.

Regardless of political affiliation, most economists agree on one thing: Future tax uncertainty is real.

That is why proper estate and retirement planning should not focus solely on growing assets.

It should also focus on how efficiently those assets can ultimately be used and transferred.

One of the most overlooked planning opportunities available today is the strategic use of tax-free financial vehicles.

Unfortunately, many investors immediately dismiss this category. They assume it involves unnecessary complexity or outdated products.

In reality, some of today’s most sophisticated planning strategies center around creating tax diversification.

Tax diversification simply means not having all your retirement assets exposed to the same future tax treatment. For example:

- Tax-deferred accounts will eventually create taxable income.

- Taxable investment accounts will create capital gains exposure.

- Tax-free structures, when properly designed, can provide an additional layer of flexibility during retirement and estate distribution planning — both without taxation.

That flexibility matters more than most people realize.

During periods of market volatility or rising tax rates, retirees with multiple tax buckets often have greater control over where income is sourced.

That can help reduce overall tax drag and improve long-term portfolio efficiency.

Liquidity also matters.

One challenge many retirees face is that they become asset-rich but tax-inefficient.

Large retirement accounts may appear substantial on paper. But after future taxation, the spendable value may be significantly lower than expected.

Proper planning attempts to address these issues before they become problems.

This is the main reason why many proactive families often work to create greater balance between taxable, tax-deferred and tax-free assets throughout retirement.

The objective is not necessarily to avoid taxes altogether.

The objective is to legally and strategically reduce unnecessary taxation while preserving flexibility for both you and your heirs.

As I often remind clients, it is not simply what you earn that matters.

It is what you keep after taxes, fees, inflation and market losses.

It’s the score at the end of the game that matters.

The good news is that many of these mistakes can still be corrected with thoughtful planning.

If you are unsure how exposed your retirement or estate plan may be to future taxation, this is an excellent time to review your current strategy.

Questions about your estate or retirement plan? CLICK HERE to order your copy of my book, 10 Most Common Estate Planning Mistakes and How to Avoid Them.

We appreciate our readers who come our way via Weiss Ratings. Please be sure to mention “Weiss” in the Special Instructions field.

Our office is also available to help you review your current documents, accounts and tax exposure through a personalized consultation.

Just call 888-892-1102.

Live Well, Leave a Legacy!

David T. Phillips, CEO

Estate Planning Specialists