|

| By Jurica Dujmovic |

I have already covered the physical bottlenecks of the AI buildout, including …

But there is another bottleneck underneath all of it: Financing.

Which is strange because the most valuable collateral inside these long-lived projects is also the fastest-aging part of the stack: the GPU.

Banks, private-credit funds and infrastructure investors are bankrolling something that looks — on a term sheet — like ordinary infrastructure: data centers, power contracts, cooling plants, fiber and long-term customer leases.

But the buildout has its own gravity.

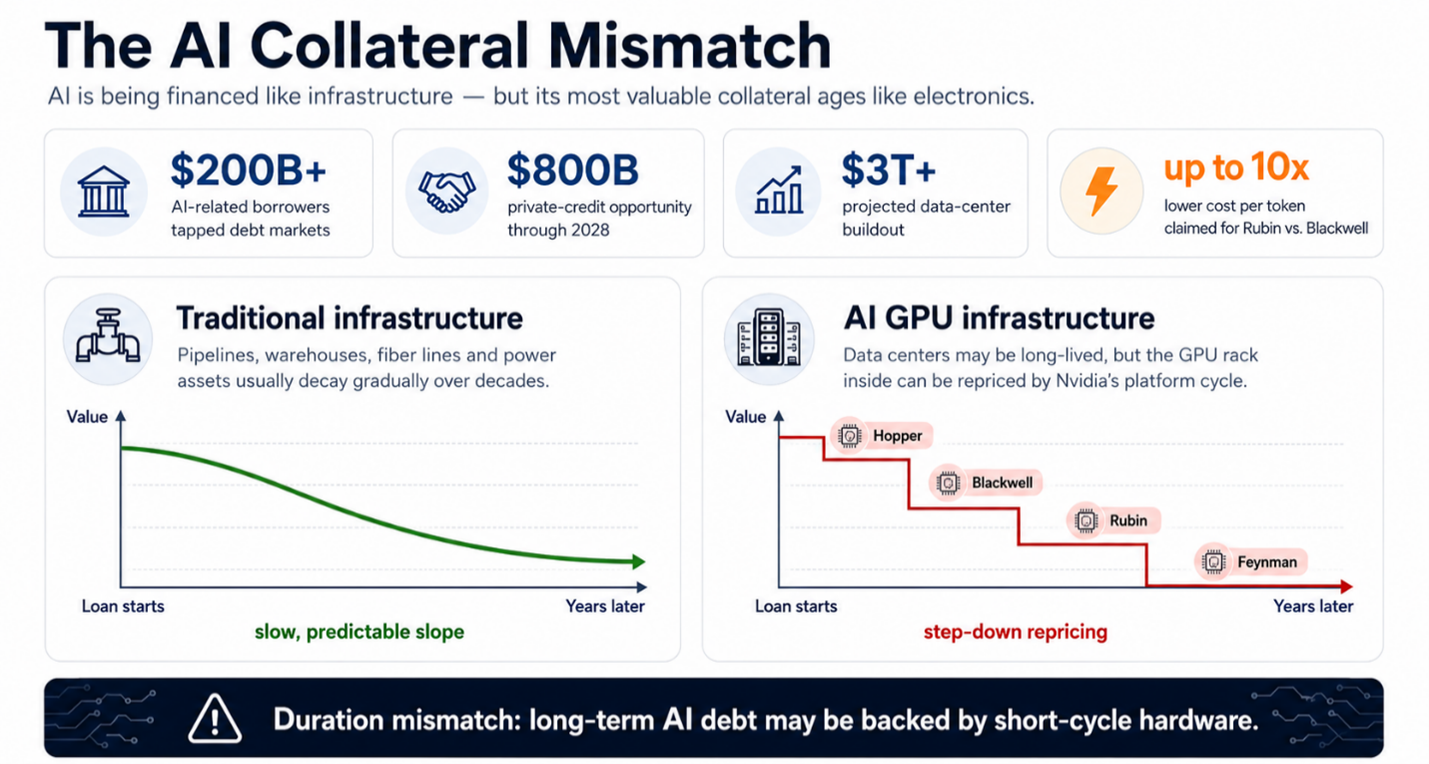

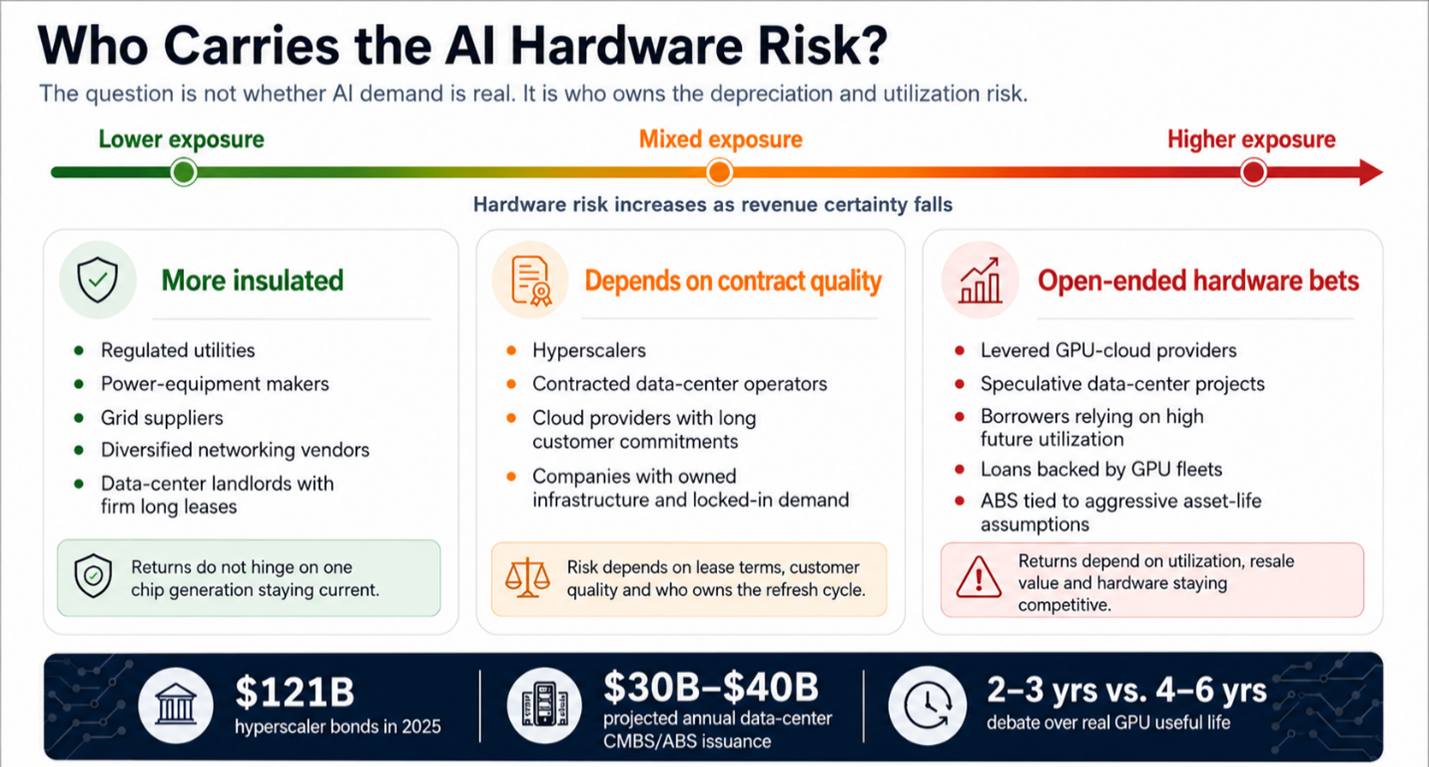

AI-related borrowers tapped debt markets for at least $200 billion1, and Morgan Stanley expects private credit alone to supply another $800 billion over the next two years2. Hyperscalers floated roughly $121 billion in bonds in 2025, more than 4x their five-year average.

The total bill for the AI buildout effort runs past $3 trillion.

Lenders are pricing most of this the way they price toll roads and pipelines — as long-duration assets that decay slowly and predictably.

That assumption is where the trouble hides.

AI’s Collateral Mismatch

The most valuable thing inside an AI data center is not the building or the substation. It is a rack of Nvidia (NVDA) hardware.

These chips’ economic life is set not by wear and tear …

But by Nvidia's product calendar.

Wall Street has begun to notice part of the problem … but filed its complaint under the wrong heading: an earnings story.

Michael Burry — an American investor and hedge fund manager — spent late 2025 shorting Nvidia and Palantir3. He also accused hyperscalers of understating depreciation by about $176 billion4 between 2026 and 2028.

How? By stretching the useful life of GPUs to five or six years when the real cycle runs closer to two or three.

Specifically, Burry called extended useful lives one of the more common frauds of the modern era.5

That’s the sort of phrasing that gets a man quoted. And AI and compute companies were quick to answer with their own numbers.

- CoreWeave pointed to five-year customer contracts and resale values it pegs near 95% on older A100 and H100 chips.6

- Nvidia, in a memo rebutting Burry, said its customers depreciate the hardware over four to six years7, citing real-world longevity and utilization.

This framing, while worth separate examination, misses the more interesting risk. Depreciation is an accounting choice. Collateral value is not.

A lender does not care how Meta (F) books its servers. It cares about the value the hardware securing the loan will fetch if the borrower stops paying.

Which means lenders should focus on hardware cycles, not accounting policy.

This is where Nvidia's own roadmap becomes the evidence for the prosecution.

In early June, the company said its Vera Rubin platform had ramped into full production.8 Nvidia claims it can deliver up to 10x lower cost per token9 than Blackwell.

Sit with that figure.

A Blackwell compute rack — financed just last year in 2025 on a six-year schedule — will already be facing competition later this year marketed around a fraction of its inference cost.

The Blackwell hardware still runs. It simply earns less per dollar of power and floor space.

And that’s the only metric the cloud operator paying the electricity bill actually cares about.

Lenders do not get to wait for full deployment to find out. Collateral reprices on expectations, and the expectation is now public.

Blackwell did the same thing to Hopper a year earlier. Rubin will do it to Blackwell. And the next anticipated platform, Feynman, will do it to Rubin.

When the market standard moves, the previous generation does not necessarily depreciate like a pipeline. Older racks can keep earning in secondary workloads for a while.

In fact, that is the heart of the bull case and the reason CoreWeave can still quote high resale figures.

But all that means is their pricing power resets in steps, rather than gliding down a straight line. Because it is undeniable that each new platform resets the cost per token that the whole market pays.

And that creates a very different risk profile from the one a pipeline carries over thirty years.

Not only that, but companies like Nvidia are producing the next-gen chips today. And, according to the company’s plans announced at Computex earlier this month, there will be rollouts through 2030.

This pressure brings the collateral problem comes into focus.

A solar farm, a fiber line or a warehouse has a useful life measured in decades.

But an AI rack has a useful life measured in competitive generations, and Nvidia is compressing those generations on purpose.

The lender believes it is financing infrastructure. But when it comes to AI, what’s being financed behaves more like high-end electronics inventory.

And electronics inventory ages badly.

This means the risk that lives in this gap is being packaged and resold. Data-center debt is increasingly flowing into asset-backed securities.

JPMorgan, for example, projects $30 billion to $40 billion10 of issuance in both 2026 and 2027.

Lawyers who worked through the last structured-credit blowup have already flagged the parallels11. In 2008 the contested assumption was housing prices. This time it is GPU lifespan.

Both had layered debt, thin disclosure on terms, and valuations that rest on assumptions rather than anything observable.

Stay Smart About AI Opportunities

The honest takeaway is not “avoid AI.” The demand is real, and the better operators will be fine.

The trick for investors will be to sort AI exposure by who carries the hardware risk.

The safer end of the spectrum holds companies with locked-in, long-duration revenue that does not hinge on any single chip generation, like …

- Regulated utilities,

- Power-equipment makers,

- Grid suppliers,

- Networking vendors with broad demand,

- And data-center landlords with firm tenants on long leases.

The riskier end holds the open-ended hardware bets …

- Heavily levered GPU-cloud providers,

- Speculative data-center projects without committed customers,

- And any borrower whose loan only pencils out if utilization stays high and the silicon stays current.

The market has not priced this collateral gap in yet. Which means you still have time to adjust your approach to AI.

Because the time is coming when it can’t be ignored. And by then, it may be too late for retail investors to adjust course.

Savvy investors should make sure their AI plays have the stability and longevity to see things through to the other side.

Best,

Jurica Dujmovic

1 https://www.insurancejournal.com/news/international/2026/02/03/856623.htm

3 https://www.aol.com/articles/michael-burry-ai-stocks-wrong-151803706.html

5 https://finance.yahoo.com/news/fast-does-ai-chip-depreciate-164511602.html

6 https://www.aol.com/articles/michael-burry-ai-stocks-wrong-151803706.html

7 https://www.cnbc.com/2025/11/25/nvidia-pushes-back-on-charges-that-ai-investment-is-a-bubble.html

8 https://nvidianews.nvidia.com/news/vera-rubin-full-production-agentic-ai-factory

9 https://www.sec.gov/Archives/edgar/data/0001045810/000104581026000019/q4fy26pr.htm