Bitcoin's Identity Crisis Is Now a Balance Sheet Problem

|

| By Jurica Dujmovic |

Bitcoin (BTC, “B+”) has a price problem. It also has a narrative problem.

The two are not unrelated.

After hitting an all-time high of $126,000 in October 2025, Bitcoin spent the following two quarters unwinding.

Now, as we close out Q1 2026, it has shed roughly 22% year-to-date — its second consecutive quarterly decline.

Gold, meanwhile, pushed past $5,000 an ounce as we started the new year. Despite correcting in response to the Iran War, it’s still up for the year by roughly 6%.

The yellow metal isn’t the only comparable asset that outperformed. Stablecoins processed $33 trillion in transaction volume in 2025, surpassing Visa's (V) annual throughput. And the Nasdaq, despite its own volatility, did not fall nearly as hard.

Bitcoin's advocates have a story for each of those comparisons: The digital gold crowd points to scarcity. The macro-trade crowd points to liquidity cycles. The monetary revolution crowd points to Lightning Network adoption.

Each camp is convinced they are right, and each camp has months — sometimes years — of price action to back their case.

To me, that is precisely the problem.

Bitcoin is simultaneously attempting to function as a store of value, a macro risk asset and the foundational layer of an alternative financial system.

In practice, it behaves inconsistently across all three roles. Now, that inconsistency is no longer just a talking point for critics. It is measurable — and it is showing up in institutional allocation behavior.

The Digital Gold Test — and Where It Breaks

The store-of-value thesis rests on a simple premise: When fiat confidence weakens, inflation persists or geopolitical stress rises, Bitcoin should behave like gold — rallying, or at minimum holding, while risk assets sell off.

But that thesis has been inconsistently proven.

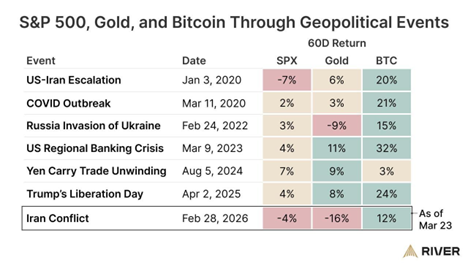

In an acute crisis, Bitcoin has outperformed gold. Marija Matic showed you just two weeks ago that in the seven major geopolitical conflicts since BTC’s launch, it has outperformed gold by the 60-day mark each time.

But if we zoom out, the safe-haven case gets a bit weaker.

Before the Iran War broke out, gold gained roughly 80% year-over-year. That rally saw it clear $5,300 per ounce … even as central banks accelerated reserve accumulation and geopolitical risk intensified.

During that same stretch, Bitcoin dropped 47% from its October 2025 peak.

The macro setup — weaker dollar, rising geopolitical risk, building expectations of Fed rate cuts — was precisely what Bitcoin bulls argued would send BTC higher.

Instead, Bitcoin consolidated and sold off while metals surged.

My colleague and cycles expert Juan Villaverde would likely argue that it is precisely because of the cycles that Bitcoin didn’t keep up with the yellow metal.

But a paper by Duke University's Campbell Harvey, published in September 2025, gives a little more clarity. It examined both assets' safe-haven properties directly and found that gold continues to maintain a more stable role during crisis periods.

Why? Because Bitcoin tends to move with broader risk assets, sometimes amplifying portfolio volatility rather than protecting against it.

This makes sense if you think about it. Many institutions that hold BTC on their balance sheets still treat it as a risk asset rather than a store of value. It’s only in times where access to traditional trading — like in a crisis when traditional markets are closed — that Bitcoin becomes the only accessible safe haven.

But if investors just feel an economic squeeze, muscle memory and concern over Bitcoin’s other identities will likely send them to gold.

A hedge that only hedges sometimes is not a hedge. It is a conditional trade. And institutions do not size conditional trades the same way they size structural allocations.

The Macro Asset Reality — Bitcoin Trades Like Liquidity

As I said, a lot of why Bitcoin is failing the gold test is because not every big foot investor treats it as a safe haven.

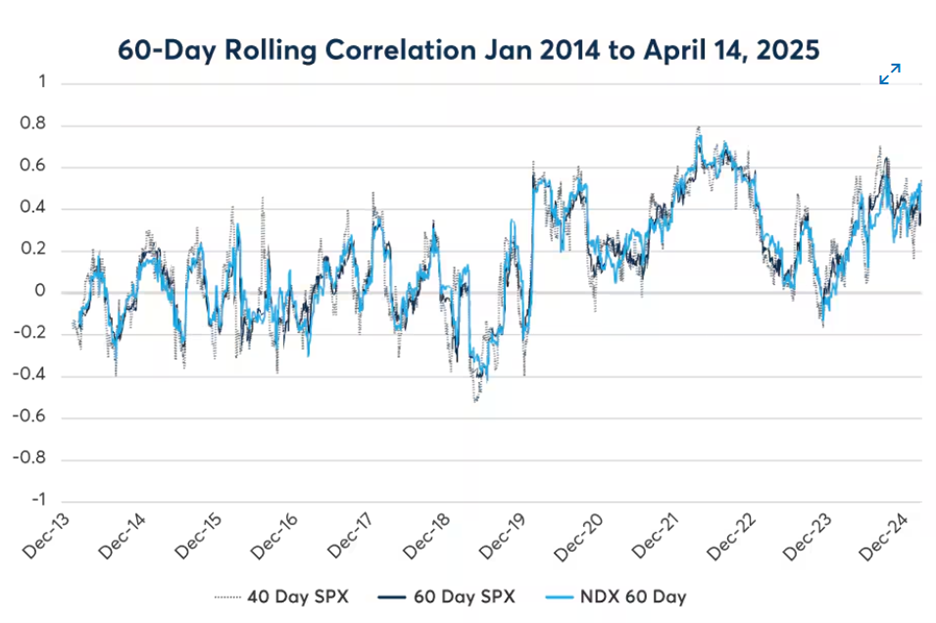

Instead, many understand it as a macro-risk asset. The clearest signal came from correlation data.

- In 2025, Bitcoin's rolling correlation with the Nasdaq-100 more than doubled its 0.23 average from the prior year.

- According to LSEG data, the BTC-Nasdaq correlation ran between 0.35 and 0.60, with some analysts measuring it as high as 0.68-0.75 during the worst of the January-February 2026 sell-off.

BlackRock's Robbie Mitchnick warned in February 2026 that heavy use of leverage in Bitcoin derivatives is undermining the asset's institutional appeal. He called its trading behavior similar to "levered NASDAQ."

The comparison is not flattery. A levered NASDAQ proxy is a legitimate portfolio tool. It is not a safe haven, a monetary network or a reserve asset.

The Monetary Network Thesis — Quietly Losing Ground

The original vision of Bitcoin as peer-to-peer money is the hardest identity to square with current data.

Not because the technology failed, but because a competing infrastructure won the use case.

Stablecoin transaction volumes hit $33 trillion in 2025, up 72% year-over-year, according to Artemis Analytics data cited by Bloomberg.

USD Coin (USDC, stablecoin) alone processed $18.3 trillion. Tether (USDT, stablecoin) processed $13.3 trillion. Together, the two tokens processed more transaction volume than Visa's entire annual throughput of $16.7 trillion.

McKinsey estimated that actual stablecoin payments — excluding wash trading and DeFi recycling — totaled approximately $390 billion in 2025, more than doubling from 2024 levels.

This growth happened during a period when crypto markets broadly were in a downturn.

The stablecoin use case that Bitcoin advocates long described as Bitcoin's destiny — global, borderless, permissionless payments — is being built and captured by dollar-pegged instruments instead.

The "money" use case exists, but Bitcoin is not winning it.

The Correlation Problem — the Clearest Symptom

Pull the three identity failures together and what emerges is a correlation problem — which is ultimately a portfolio construction problem.

Bitcoin sometimes correlates with equities. Sometimes it decouples.

Sometimes it moves with nothing. And sometimes it moves against everything, including gold.

That instability is not a minor inconvenience.

Institutional capital requires predictable correlations, definable behavior and repeatable patterns. Not because institutions are unsophisticated, but because their risk frameworks and portfolio mandates depend on them.

A commodity with unknown correlation properties does not fit neatly into a risk model. It floats between buckets: too volatile to be fixed income, too uncorrelated to be a reliable equity supplement, too speculative to replace gold.

The Investor Implication

The data across all three identity claims points to the same conclusion: Its correlations are not stable.

None of this means Bitcoin is broken. It means Bitcoin is unresolved.

The market has not yet decided what Bitcoin is. Until it does, capital will continue to treat it as something to trade — not something to hold.

For investors, that creates a specific problem: role ambiguity.

Bitcoin does not lack demand. It lacks definition. And an asset without a clear identity is an asset that sophisticated capital will continue to approach the same way: cautiously, tactically and with one hand on the exit.

And that’s exactly what we’ve seen in how institutions are actually sizing their positions — tactically, not foundationally.

For that to change, one of the three competing identities needs to win decisively.

Right now, none of those outcomes is imminent. Which is why savvy investors will have their eye on correlation over the coming months.

That’ll be the first clue to tell us which identity will win out. And what role it’ll play in your portfolio.

To see how Juan and his Crypto Timing Model play it, click here.

Best,

Jurica Dujmovic