Crypto’s Quiet Giants Could Be the Big Brother of the Blockchain

|

| By Jurica Dujmovic |

In the shadow of Bitcoin's price fluctuations and the memecoin circus, a quieter revolution has been steadily gaining momentum: Stablecoins are silently infiltrating the mainstream financial system.

Often overlooked in headlines dominated by AI tokens and NFT collectibles, these digital assets pegged to fiat currencies are reshaping global payment networks in ways that deserve attention … and scrutiny.

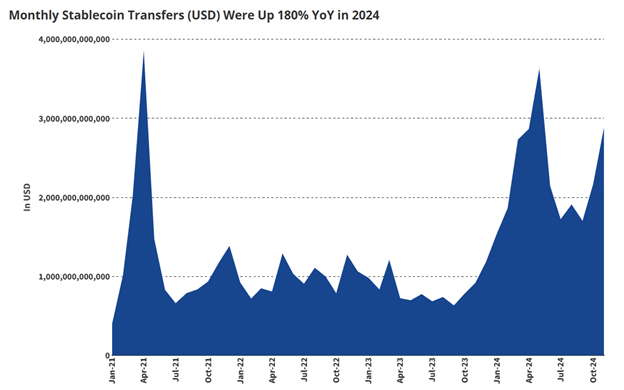

Let’s start with the obvious. On-chain activity for stablecoins reached all-time highs in March 2025, with market capitalization reaching over $230 billion.

That’s a number that would have seemed impossible just a few years ago.

Industry forecasts from VanEck suggest daily stablecoin transfers could hit $300 billion by December. That’s roughly 5% of the volume processed by major traditional payment networks and significantly higher than the $100 billion in daily transfers seen in 2024.

For a financial instrument that barely registered on the radar five years ago, this trajectory is nothing short of remarkable.

And it’s on track to accelerate, especially as …

Corporate Giants Enter the Game

The clearest sign of stablecoins breaking into the mainstream comes from recent moves by payment behemoths.

According to a March 24 Reuters report, Visa (V) is in discussions with Sam Altman's Worldcoin (WLD, Not Yet Rated) network. The idea is to integrate stablecoins into the network so they can then bring Visa card functionality to World Network wallets.

This would then enable stablecoin-based payments across Visa's vast merchant network.

This partnership with Worldcoin — a controversial biometric cryptocurrency project founded in 2019 by Altman (who is also the CEO of OpenAI), Max Novendstern and Alex Blania — is more than just your standard TradFi/crypto collaboration.

It could potentially bring about a fundamental shift in how digital dollars move through the global economy.

If implemented, shoppers could theoretically spend their stablecoins — like USD Coin (USDC) — anywhere that accepts Visa payments. That’s millions of retail locations worldwide! And it would also mean merchants would receive settlement faster than traditional card payments.

Naturally, MasterCard (MA) and other major financial players are reportedly exploring similar initiatives, though they've been more guarded about their plans.

In short, this partnership could bring even more people into the crypto economy via stablecoins.

But there’s another edge to this sword. One that is set to split the crypto masses.

The partnership with Visa would significantly expand Worldcoin's reach and influence. And there are a lot of voices speaking out against that spread.

Not because they don’t want more stablecoin activity in the market. But because they fear what will happen to privacy on the blockchain when a centralized payment giant like Visa pairs up with a crypto project that has already faced substantial criticism for its privacy implications and data collection practices.

Related story: In Worldcoin’s World, Data Is Currency and Privacy Is Dead

That fear has two main components:

- The reduction of privacy on the blockchain through stablecoin monitoring, and

- The reliance on a third-party for security.

Let’s start with the first concern.

Stablecoins: Privacy Vs. Security

To be clear, I don’t see stablecoins themselves as inherently problematic. Their core function — maintaining parity with fiat currencies while leveraging blockchain efficiency — serves a valuable purpose in the crypto ecosystem.

Used responsibly, stablecoins can facilitate faster, cheaper transactions without compromising user sovereignty. That fundamental utility explains why they’ve raced ahead when it comes to adoption.

The concerns arise when they become vehicles for government overreach and surveillance capitalism rather than simply being digital dollars.

Now, if you’re coming from TradFi, it could be hard to understand my concern. After all, your bank cards and financial transactions are already being tracked.

But that is not the case for crypto. Or rather, it was never intended to be.

See, crypto was designed to eliminate the need for that sort of oversight. As a “trustless” system, you don’t need to trust …

- A banking platform to custody your assets. You hold them yourself in your own software wallet.

- Another person to pay back the assets you loaned them. The smart contract you both signed using your crypto keys will automatically make sure payment is processed if the set conditions are met.

- A broker to buy/sell assets on your behalf. You are in control of your own financial destiny.

By cutting out the middleman, you give yourself a new level of privacy and security thought to be impossible in the digital age.

Of course, some services adopted a more centralized model in order to interact with the TradFi system and increase adoption. Platforms like centralized exchanges, for example, need to be compliant with regulations, which includes keeping track of who trades what on their platforms.

However, there is a more concerning push to bring that type of oversight and control to the rest of the blockchain.

I’ve written about this in regards to Central Bank Digital Currencies (CBDCs). And what the Visa/Worldcoin partnership proposes is not too different from that of CBDCs. Both systems offer programmable money, accelerated settlements and — most concerning — unprecedented transaction surveillance capabilities.

Related Story: The Challenges Facing the ‘Digital Dollar’

And both the Visa/Worldcoin stablecoin and CBDCs enable the potential for mass surveillance under the marketing banner of "preventing terrorism and money laundering."

There are some minor differences between them, of course.

Unlike CBDCs, stablecoins can currently be self-custodied in soft wallets like MetaMask or hardware wallets. That means they are stored beyond the reach of governments and can be traded peer-to-peer without oversight.

This is a freedom that CBDCs likely wouldn’t permit.

And if Visa or Mastercard integrates stablecoins, users can expect full KYC, geo-blocking and transactional oversight. Which would make their stablecoins just like a regular bank card.

In short, it is possible in the near future that the only difference between stablecoins and CBDCs could be who operates them — corporations or governments.

And that concern is only amplified when the question of security comes into play.

Worldcoin: The Big Brother of Crypto

I can understand how some investors — particularly those outside the crypto ethos — argue that institutional-grade projects need to gather and store your personal information. The belief is that doing so allows them to offer enhanced security and user protections.

That’s a comforting thought … though it ignores actual evidence to the contrary.

For example, the Bybit hack in March rocked the markets as hackers washed $400 million. Now that is a scenario where freezing assets makes sense … and yet Circle took over a day to blacklist the address associated with the hackers.

That delay certainly raised a few red flags.

Now image it wasn’t only your crypto that was compromised … but your biometric data.

Because that’s how Worldcoin operates. Rather than more popular “know-your-customer” approaches — like uploading a copy of your driver’s license or entering your personal information for verification — Worldcoin uses a futuristic "orb" device called World ID to scan users' irises and “verify their humanity.”

That means if adoption takes off, we could face a scenario where accessing your own funds may require surrendering biometric data.

Which is a level of oversight even the average person may feel queasy about. And crypto enthusiasts — who still believe in a truly decentralized and trustless financial system — are adamant that it is a step too far.

Especially considering Worldcoin has already been involved in a security scandal.

TechCrunch reported in May 2023 that several Worldcoin operators lost login credentials during a cyberattack, potentially exposing users who had provided their iris scans.

The company's response followed a familiar crisis management playbook. Worldcoin spokesperson Jannick Preiwisch assured TechCrunch that "no sensitive or personal user data" was accessed. He claimed the biometric data is always encrypted and never accessible to Orb operators.

But these reassurances ring hollow when examined alongside independent security assessments.

Blockchain security firm CertiK uncovered vulnerabilities within Worldcoin's system in 2023. And numerous analysts have flagged the inherent risks of Worldcoin's centralized data storage model.

The fundamental issue remains: Once your iris scan is captured, you're placing permanent, unchangeable biometric identifiers in the hands of a private company with a concerning security track record.

If this data is leaked or compromised, you simply can't "get a new iris"— the risk follows you forever.

And with Visa entering the scene, these vulnerabilities could affect a much larger pool of users.

Final Thoughts

My concern isn’t based in a few projects or parterships that push the boundaries of crypto privacy. Rather, my fear is in the potential for today's voluntary system to become tomorrow's requirement.

If World ID becomes widely adopted for online verification, participation may become socially or economically coercive. That could effectively force people to surrender their biometric data to participate fully in financial matters.

This realization forces us to confront an uncomfortable question about the true nature of emerging payment systems, like the Visa/Worldcoin stablecoin partnership.

Being aware of this danger may feel scary. But it can also be a superpower with two key benefits.

First, once you recognize this trend will persist regardless of privacy debates, you can better protect yourself.

For example, you may consider diversifying your stablecoin holdings.

Regulated options like USDC will likely benefit from TradFi integration. But decentralized alternatives like Dai (DAI, stablecoin) and even privacy-focused variants that use zero-knowledge proofs could be better for staking, lending and other DeFi activities.

And second, awareness of this push to regulate stablecoins can also reveal the best opportunities in the stablecoin sector.

The clearest plays in my mind lie in the infrastructure powering stablecoin transfers, such as …

- Layer-1 blockchains optimized for stablecoin transactions, like Solana (SOL, “B”) and Avalanche (AVAX, “B+”),

- Cross-chain bridge protocols, like Wormhole (W, “C-”) and Axelar (AXL, Not Yet Rated), and …

- Liquidity platforms that specialize in stablecoin swaps, like Curve Finance (CRV, “D”).

Crypto developments like the Visa/Worldcoin stablecoin require a delicate balance between reasonable concern and optimism.

You should always be aware what information you trust to a third party and how much control they have over your financial independence.

On the other hand, I wouldn’t let this stop you from finding opportunities in crypto. You’ll just need to be more discerning as you navigate this ever-evolving market.

Best,

Jurica Dujmovic