Stay a Step Ahead of Rising AI Costs with 5 Picks

|

| By Jurica Dujmovic |

Artificial intelligence is supposed to be getting cheaper.

Model providers advertise lower prices.

Chipmakers deliver more calculations per watt.

And smaller models increasingly match capabilities that once required the most expensive systems.

Here’s the problem …

Corporate AI bills are moving in the opposite direction.

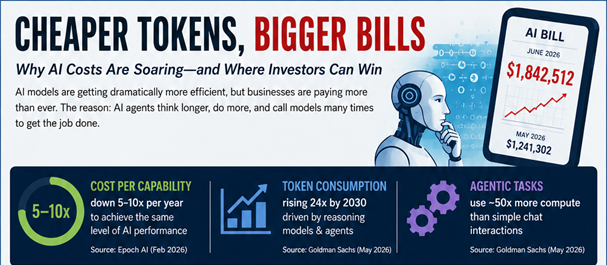

Businesses have discovered that the price of a token and the cost of completing useful work are two very different things. That gap is becoming one of the most important investment questions in technology.

Yesterday’s AI Is Cheaper

The argument that AI is becoming cheaper is not fiction; it is simply easy to misinterpret.

Epoch AI’s analysis of inference-price trends1 found that the price of reaching fixed benchmark-performance milestones has fallen rapidly. A model capable of doing work that required a frontier system several years ago can now often do it at a fraction of the cost.

But companies are rarely buying yesterday’s intelligence.

They’re investing in the newest reasoning models, longer context windows, web searches, code execution and autonomous workflows.

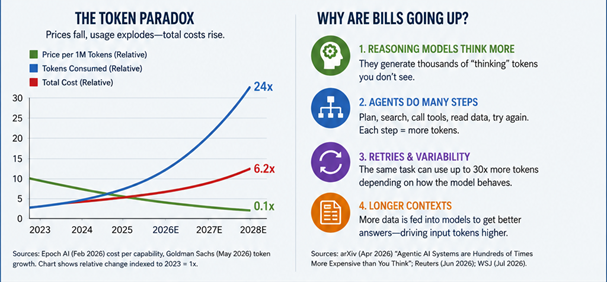

With frontier pricing still substantial, the result is a peculiar form of deflation: The cost of a fixed level of capability declines, while the frontier moves forward and creates new, more computationally demanding products.

Consumers see a smarter model. The accounting system sees more context, more reasoning and more billable work.

Agents Turn One Prompt into a Workload

The shift from chatbots to agents magnifies the effect.

A chatbot generally waits for a request and returns an answer. An agent may break a job into subtasks, retrieve information, interact with software, verify the result and repeat failed steps without asking the user for permission.

A 2026 study of agentic coding tasks2 found that agents could consume roughly 1,000x as many tokens as conventional code chat or code reasoning. The time to complete the same task can vary by as much as 30x.

But importantly, higher consumption did not reliably produce better results. The models also struggled to predict their own eventual token use.

This unpredictability matters. A traditional software subscription is easy to budget: Multiply the number of employees by the annual seat price.

But that’s not how an AI agent operates. It acts less like software and more like a worker who can independently order cloud resources, hire subcontractors and repeat a project until satisfied.

And that can expand the budget quickly. Without oversight.

Goldman Sachs Research expects agentic AI to drive a 24-fold increase in token consumption by 2030.3 The forecast assumes falling unit costs will stimulate enough new demand to increase total spending.

Recent corporate behavior suggests that process has already begun.

Reuters reported in June4 that soaring bills are pushing businesses toward cheaper models, open alternatives and systems that route each job to the least expensive model capable of completing it.

The paradox is now visible in real budgets: AI can become cheaper per unit … while becoming more expensive in aggregate.

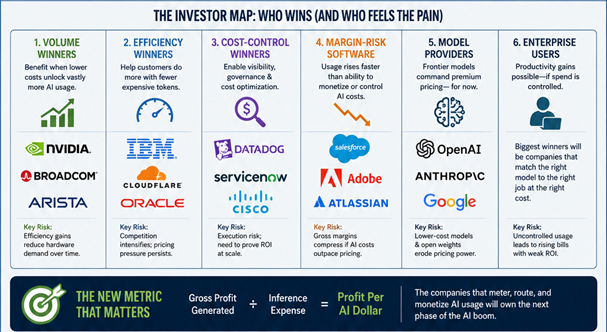

Which means that the first phase of AI — that rewarded companies that supplied scarce computing power — is over.

The next phase will turn its rewards in a new direction. Toward companies that can …

- Convert exploding consumption into recurring revenue,

- Help customers reduce waste,

- And quietly absorb variable AI costs inside fixed-price software subscriptions.

Which means the metric investors should watch has changed. Now, the focus is on gross profit generated per dollar of inference expense.

And I see three categories that these new winners will fall into.

Category 1: Volume Winners

For Nvidia (NVDA), Broadcom (AVGO) and the cloud platforms, the bullish case is straightforward: Token consumption must grow faster than efficiency improves.

Of these, Nvidia remains the clearest volume bet.

Each new generation of accelerators reduces the cost of inference. But lower costs can unlock more applications, larger models and longer-running agents.

The risk is not that AI use stops growing. It is that hardware and software efficiency eventually reduce the number of accelerators required faster than new workloads emerge.

Broadcom and Arista Networks (ANET) offer a second-order version of the same trade. These companies benefit from rising system traffic. Even when model providers cut their headline token prices.

Categories 2 & 3: Efficiency & Cost-Control Winners

The more original investment opportunity may sit one layer above the models. As companies deploy agents across multiple providers, AI spending becomes an observability, routing and governance problem.

That’s where our next two categories come into play. Both focus on exerting greater control on an AI agent’s process. The difference is where exactly that control lands.

For efficiency winners, the goal is to redirect the process through a more efficient channel.

To that end, IBM (IBM) does not need to win the frontier-model race to benefit. It can win by helping large companies decide when an expensive frontier model is unnecessary.

Its agent control plane5 promises centralized monitoring, optimization and cost control across agents, regardless of where they were built.

Cloudflare (NET) is another in this category. Its AI Gateway analytics6 track requests, tokens, errors and costs across providers. Cloudflare also offers caching, rate limits and real-time spending limits.7

If enterprises increasingly treat models as interchangeable utilities, the gateway that decides where each request goes can become more strategically important.

Two different approaches to the same goal: the ability to adjust a process for greater efficiency to help reduce overall costs.

On the other hand, cost-control winners want to control, well, the cost.

Datadog is a direct example.Its documentation explains that the platform can calculate estimated cost for individual model requests8 using token counts and provider pricing.

That capability becomes more valuable when a business needs to determine why an agent used 10x its normal budget without producing a better answer.

ServiceNow (NOW) may be able to take things to the next level and connect AI cost to business value.Its AI Control Tower9 is designed to discover and govern models and agents while measuring performance and value.

That workflow position matters because enterprises do not ultimately care about cost per token. They care about cost per resolved support case, processed invoice, completed software ticket or qualified sales lead.

5 Stocks, 5 Positions in the Token Chain

|

Company |

Role |

What must go right |

Primary risk |

|

Nvidia |

Volume winner |

Token demand outruns hardware and software efficiency |

Customers need fewer accelerators per unit of useful work |

|

Broadcom |

Network and custom-chip winner |

AI traffic and custom silicon keep expanding |

Hyperscalers internalize more technology or capex slows |

|

Datadog |

Observability winner |

AI cost monitoring becomes a standard enterprise requirement |

AI observability remains a feature rather than a large market |

|

Cloudflare |

Routing and control winner |

Enterprises use multiple models and need gateways, caching and spend controls |

Model providers bundle equivalent controls |

|

ServiceNow |

Workflow monetization winner |

It connects AI spending to measurable business outcomes |

Customers resist consumption pricing or agents fail to deliver ROI |

These are not five versions of the same AI bet. They occupy different positions in the token economy.

Nvidia and Broadcom need expanding volume.

Datadog and Cloudflare benefit from complexity and the need to control it.

ServiceNow must prove that it can turn model activity into measurable workflow value.

All are worth watching as we move forward in this new phase of AI.

The eventual winner may not have the lowest token price or the most powerful model. It may be the company that can prove that every dollar of AI consumption creates more than a dollar of economic value.

The Risk Category

The most vulnerable companies may be software vendors that bundle costly AI features into flat-rate subscriptions.

The economics look attractive during limited trials. But an assistant that answers a handful of questions is very different from an autonomous agent that runs continuously across thousands of customers.

If the software company pays for every model call while customers continue paying a fixed monthly fee, successful adoption can narrow profit margins.

That does not make Salesforce (CRM), Adobe (ADBE), Intuit (INTU), Atlassian (TEAM), HubSpot (HUBS) or other AI-enabled software companies automatic losers. It means investors should demand better disclosure.

Specifically, you should ask …

- If AI-related revenue is separated from ordinary subscription growth,

- Whether usage is metered,

- If the vendor can route routine work to cheaper models,

- And how much incremental gross profit AI produces after inference costs.

Software companies with valuable proprietary data and deep control over business workflows should have more pricing power.

On the other hand, thin application layers that merely pass requests to a third-party model may find themselves trapped between demanding customers and powerful model suppliers.

The Bottom Line

AI is getting squeezed.

Yesterday’s capabilities are becoming cheaper. But frontier models and agents are using far more tokens to perform increasingly ambitious work.

That means prices to use AI keep rising … without a guarantee that the company will see a return on investment.

For infrastructure suppliers, the boom continues as long as consumption outruns efficiency. For software providers, the same growth can become a margin problem when variable model costs sit underneath fixed subscription revenue.

And for observability, routing and workflow platforms, runaway spending creates a new market for control.

That is the next phase of the AI trade.

Investors should stop asking whether tokens to use AI are getting cheaper. Now, they need to ask who gets paid when the machines outspend their budgets.

Those will be the real winners of AI’s phase 2.

Best,

Jurica Dujmovic

1https://epoch.ai/data-insights/llm-inference-price-trends

2https://arxiv.org/abs/2604.22750

5https://www.ibm.com/products/watsonx-orchestrate/agent-control-plane

6https://developers.cloudflare.com/ai-gateway/observability/analytics/

7https://developers.cloudflare.com/ai-gateway/features/spend-limits/

8https://docs.datadoghq.com/llm_observability/monitoring/cost/