This Final Indicator Says Bitcoin’s Low Is Likely In

|

| By Juan Villaverde |

For years, I’ve written about the era of “fiscal dominance.”

Broadly speaking, that refers to monetary policy not set by central banks (as it should be). But by fiscal authorities — those who govern taxing and spending.

I recently made clear why I believe we are firmly in the era of fiscal dominance.

And this changes how we can understand the markets as investors.

To forecast what central banks do in terms of issuing money, we shouldn’t listen to what they say. Instead, we should assess how much money the government needs to borrow.

From endless wars abroad to new welfare programs at home, the government’s appetite for spending is insatiable. And taxes are never enough.

So, most of that spending winds up financed through borrowing. Which is done by the Treasury issuing bonds.

At least, it is now.

In the aftermath of the 2008 Global Financial Crisis, central banks pushed money printing to extremes. Inflation wasn’t an issue, so no one batted an eye.

Then, thinking there would be no consequences, central bankers doubled down during the COVID years. They flooded the world with free cash.

But then came 2021. After more than a decade of the most aggressive monetary experiment in modern history, inflation reawakened.

To a politician, though, inflation is little more than a political liability.

Which is why, in the U.S., politicians in the White House and Congress blamed the Federal Reserve. “You completely missed obvious signs of inflation heating up,” they said.

With a straight face! As if they hadn’t been begging for free money just a year earlier.

But the hypocrisy didn’t matter. The Fed got the message loud and clear: No more money printing.

But that left a critical question unanswered: Who would finance the trillions Uncle Sam needs every year?

Enter Treasury Secretary Janet Yellen. And her solution was simple: Why not use commercial banks?

When it comes to printing money, there is no meaningful difference between a central bank and a commercial bank.

The Fed creates money by paying for government bond purchases with a check it writes out of thin air. In a fractional reserve banking system, commercial banks create money by making loans to commercial customers. And by writing checks out of thin air.

The difference is that commercial banks are profit-seeking institutions. Central banks pursue political mandates and are immune to profit and loss.

So how can commercial banks be persuaded to help finance endless deficits? Washington can’t force them. That would expose the government’s desperation, raising uncomfortable questions.

The solution is simple: Offer them something they really want.

And that’s where Treasury bills come into play.

T-bills are government securities that mature in less than one year. The market treats them as cash equivalents. To a commercial banker, a T-bill is essentially cash — but with yield attached.

That makes T-bills a nearly “risk-free” asset that earns interest. From a commercial banking perspective, that’s a no-brainer.

The architect of this approach was former Treasury Secretary Yellen. Scott Bessent, Trump’s current Treasury Secretary, has continued it.

A Whole New Class of Treasury Bill Buyers

But it’s not just commercial banks that jumped on the bandwagon.

Stablecoin issuers are also eager to get their hands on a government-backed, nearly “risk-free” yield-bearing asset. Not only because of the income. But because building their reserves out of T-bills means those stablecoins can increase their stability and legitimacy.

Related story: The Fed’s Secret Crypto Shadow

In fact, the passage of the GENIUS Act last July — which established clear regulatory guidelines for stablecoins — should be understood through this lens.

You see, Washington’s interest in crypto was only secondary. What really mattered was clearing the way for stablecoin issuers to become a major new class of T-bill buyers.

And a fresh source of financing for endless deficits.

I’ve believed this to be the case for some time. And let me be clear: This does matter. Because Bitcoin and crypto asset prices are almost entirely driven by these monetary dynamics.

If central bankers are printing money, as analysts, we care what the Fed is doing. If the Treasury is effectively doing the printing, we care about them instead.

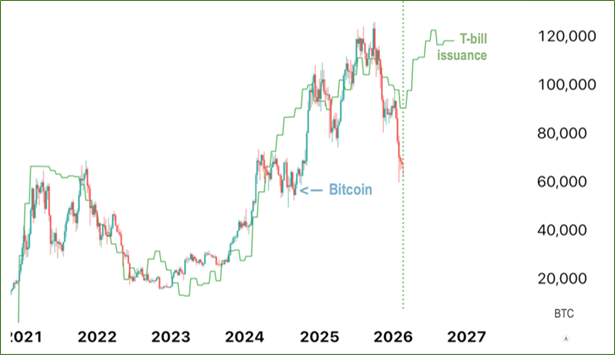

And below, you can see that when the Treasury expands T-bill supply, financial assets like Bitcoin tend to respond roughly eight months later.

The Most Important Chart in Crypto, Right Now

This makes sense.

The Treasury sold hundreds of billions in T-bills in the second half of 2022, but crypto was still in a bear market. The rally only began eight months later, in early 2023.

Overall, we can see that since March 2020, Bitcoin’s major moves have aligned more closely with Treasury issuance than with Federal Reserve policy.

This strongly supports the fiscal dominance thesis. Under this framework, the U.S. Treasury has effectively become the new money-printer-in-chief.

Now let’s zero in on 2025.

The year started with a pause in expanding T-bill issuance. And that helps explain why crypto weakened in October. Issuance slowed, liquidity tightened and markets responded.

Around July 2025, the U.S. Treasury resumed the expansion of T-bill issuance. As I said, it takes eight months for us to see the impact in crypto. Which means we should see renewed issuance factor into crypto’s price action right about now, in February 2026.

This is just another macro indicator supporting what I’ve been saying for several weeks: A key crypto low is likely already in.

That doesn’t mean prices will take off tomorrow. But it does mean eagle-eyed investors should already be watching their favorite cryptos for signs of reversal.

Because at these levels, most top cryptos are trading for a discount.

Best,

Juan Villaverde

P.S. To learn how you can get access to specific “buy” and “sell” alerts from my Crypto Timing Model for long-term investments, click here.