|

| By Beth Canova |

Think back to this morning’s coffee run. When you tapped your card to pay, did you think about what happens in the machine between the tap and printing your receipt?

I’m going to guess not.

Your payment was accepted, the transaction was processed. That’s all you need to know.

But a lot of people made money thinking about it. A processor, a card network, a bank, a clearinghouse, a fraud check. Five or six middlemen, all taking a cut, as your payment is settled behind the scenes.

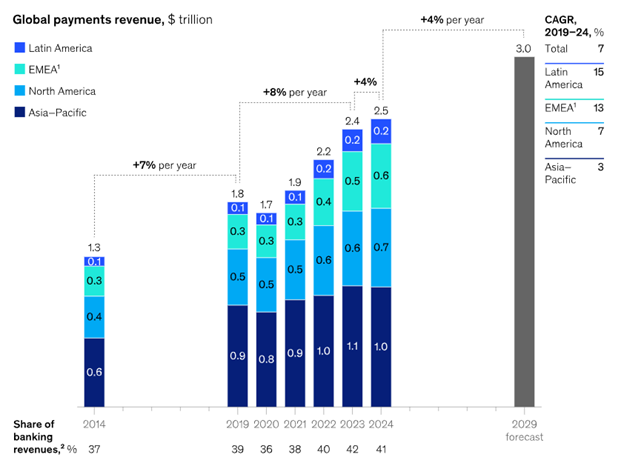

The global payment system generated roughly $2.5 trillion in revenue from fees and inefficiencies in 2024. For context, that’s about 2% of global GDP.

Just to move money from one person to another.

Crypto was supposed to fix this. The original Bitcoin (BTC, “A-”) whitepaper was titled "A Peer-to-Peer Electronic Cash System."

No middlemen. No banks. Just two people and a transaction.

That vision hasn't disappeared. But Bitcoin itself has moved on.

Its scarcity, first-mover trust and resistance to manipulation made Bitcoin something different: a savings technology. A way to store wealth outside the traditional financial system.

That's valuable … but it's not an optimal way to pay for lunch.

Which is why the payment promise is still mostly wrapped in the old system, not in crypto.

The crypto-supportive credit cards you see advertised today — the ones using Visa and Mastercard — are not crypto payments. They convert your crypto to dollars at the point of sale. Then, they route the transaction through the same legacy card networks designed before the internet existed.

The branding is new. The rails are not.

Meaning these are temporary solutions.

3 Payment Paths Forward

The real opportunity is in the projects rebuilding the rails themselves. And they're coming from three main directions at once.

The digital cash path. Some projects went back to the original premise: build a cryptocurrency that actually works as money. Fast, cheap, final.

Here are a few promising projects tackling this approach …

- Nano (XNO, “D+”) charges no fees and offers sub-second transfers with no mining at all. Pure digital cash by design.

- eCash (XEC, “E-”) was redesigned from the ground up for sub-cent transactions at scale.

- Avalanche (AVAX, “B”) achieves sub-second finality at the protocol level, meaning transactions are confirmed and irreversible almost immediately.

These are the closest thing to what Bitcoin's whitepaper originally described. They solve the speed problem by designing for it from the start.

Whether or not they’ll succeed is another story. All three networks still need a unifying mechanism to be accepted by businesses.

Investors interested in digging deeper should also look into tokenomics and security for these networks.

Weakness in either department stands as a strong headwind to adoption and long-term success.

The collateral path. Speed is one problem. Merchant trust is another.

A store owner doesn't want to learn five blockchains. They want to know they're getting paid without needing to build expertise in a new financial system.

Flexa solves this differently.

Investors stake a token called AMP (AMP, “D-”) as collateral to contribute towards the Flexa network.

Users are then able to pay in whatever crypto they want — Bitcoin, Ethereum (ETH, “B+”), stablecoins, anything. The merchant gets an instant, guaranteed payout in dollars.

If the blockchain transaction fails for any reason, the staked collateral covers it. Zero chargebacks. Zero fraud risk for the merchant. The merchant never touches crypto. The consumer never sees Flexa. It sits invisibly at the authorization layer, replacing the five middlemen with one collateral contract.

No other live system fully collateralizes every payment this way.

The stablecoin path. Stablecoins like USDT and USDC are the fastest-growing category. They move on blockchain rails, settle in minutes and don't carry the price volatility of Bitcoin or Ethereum.

The GENIUS Act, a stablecoin regulatory framework for issuers, passed last year. And the CLARITY Act, stablecoin regulatory framework for third-party platforms, is waiting for its Senate vote right now.

That's a signal. This is the rail backed by the established financial system. Which is a powerful tailwind.

For investors, the opportunity isn’t in the stablecoins themselves. Remember, as I said on Tuesday, dollar-pegged stablecoins are still bound to the dollar’s underlying weakness.

Instead, the crypto savvy should consider researching Ripple (XRP, “C+”) or Stellar (XLM, “C+”).

Both are established crypto projects. And both have received institutional interest.

That’s because they act as bridge currencies to compress international transfers from days to seconds. Banks and exchanges use them to move value across borders without holding foreign currency reserves.

These solve real problems. But most still rely on legacy backend infrastructure to complete the loop. They're upgrades to the existing system more than replacements.

Investor Takeaway

We’re still in the early days of digital, cross-border payment optimization. And no single approach has won yet.

The payment infrastructure is being rebuilt from multiple angles simultaneously, and the regulatory gates are still opening.

But the framework for evaluating what matters is already clear: Some projects are wrapping the old system in new branding.

Others are replacing the plumbing entirely.

The projects worth watching will depend on whether you believe the old system — with new trappings — will be the winner …

Or, if you agree with crypto purists and see the replacement system as the ultimate victor.

Best,

Beth Canova